Advertisement

- United States

- /

- Software

- /

- NasdaqGS:TRMB

Trimble (TRMB) Valuation Check As Analyst Optimism Grows Around Recurring Revenue And Growth Targets

Recent analyst actions around Trimble (TRMB), including an upgrade from KeyBanc and an outperform reiteration from Oppenheimer, have drawn fresh attention to the stock and its growth focus.

See our latest analysis for Trimble.

At a latest share price of $80.61, Trimble’s recent 1-day and 7-day share price returns of 1.38% and 2.91% sit alongside a 90-day share price return of 6.58% and a 1-year total shareholder return of 14.78%. Investors are weighing its Lucid Gravity partnership and recurring revenue plans as they evaluate this recent performance.

If Trimble’s recent interest in advanced positioning for EVs has caught your eye, this could be a good moment to look across auto manufacturers as you think about where technology and mobility intersect next.

With Trimble trading at $80.61, showing a 1-year total return of 14.78% and sitting around 24% below the average analyst price target, you have to ask: is there real upside here, or is future growth already priced in?

Most Popular Narrative: 18.2% Undervalued

With Trimble last closing at $80.61 and the most followed narrative pointing to fair value of $98.50, the gap hinges on confidence in its long term earnings power.

The targeted "3-4-30" framework, calling for $3B in annualized recurring revenue, $4B in sales and a 30 percent EBITDA margin by 2027, is described as a credible roadmap that could drive sustained double digit earnings growth and multiple expansion if achieved or exceeded.

Curious what ties that 3-4-30 roadmap to a near $100 fair value tag? Revenue mix, margin lift and a future earnings multiple all quietly do the heavy lifting.

Result: Fair Value of $98.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that near $100 fair value view still leans on Trimble hitting its 3-4-30 goals while avoiding setbacks related to softer government spending or tougher competition in AI software.

Find out about the key risks to this Trimble narrative.

Another View: Multiples Paint a Tougher Picture

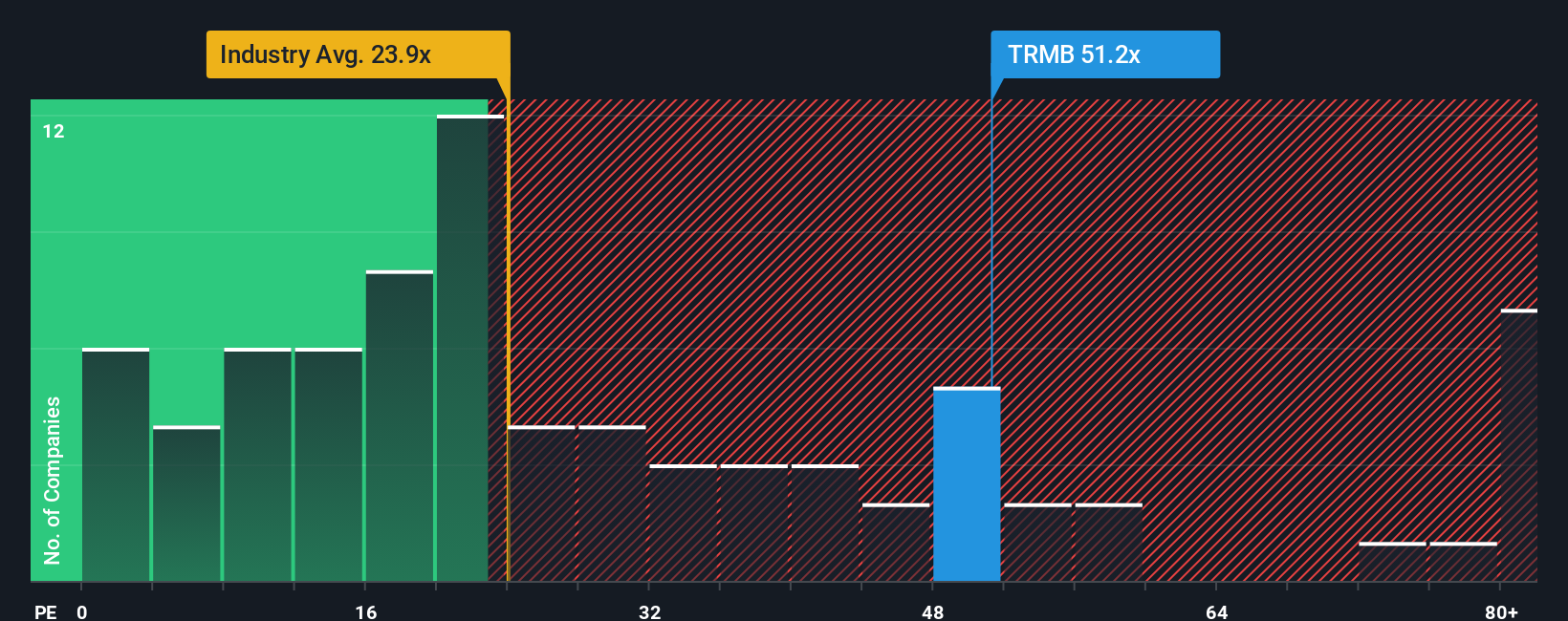

That 18.2% undervalued narrative leans on future earnings power, but today’s market multiples tell a different story. Trimble trades on a P/E of 53.6x, compared with 32.2x for the US Software industry, 38.8x for peers, and a fair ratio of 36.8x. That premium suggests less margin for error if growth or margins fall short. Which story do you think holds up best?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Trimble Narrative

If you see the numbers differently or simply prefer to test your own view, you can build a Trimble story from the ground up in a few minutes: Do it your way.

A great starting point for your Trimble research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Trimble has sparked your interest, do not stop here. The next step is lining up a few more ideas so you are not relying on a single story.

- Spot potential value with strong cash flow support by checking out these 879 undervalued stocks based on cash flows that could fit a more disciplined price tag.

- Target growth at the edge of new technology by scanning these 28 AI penny stocks that are working on real world AI applications.

- Lock in income focused opportunities by reviewing these 12 dividend stocks with yields > 3% that may offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Trimble might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TRMB

Trimble

Offers technology solutions and platform that enable office professionals and field workers to connect workflows and industry lifecycles in North America, Europe, the Asia Pacific, and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

212 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

53 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on INTLOOP ·

Renewed focus on business investment

Fair Value:JP¥4.17k56.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36036.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Fibromat (M) Berhad ·

Fibromat: More than just a niche player, with clearer earnings visibility from order book and project wins

Fair Value:RM 1.0519.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1350 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0