- United States

- /

- Software

- /

- NasdaqGS:TEAM

Atlassian (NasdaqGS:TEAM) Falls 13% Amid Q2 Revenue Rise To US$1,286 Million

Reviewed by Simply Wall St

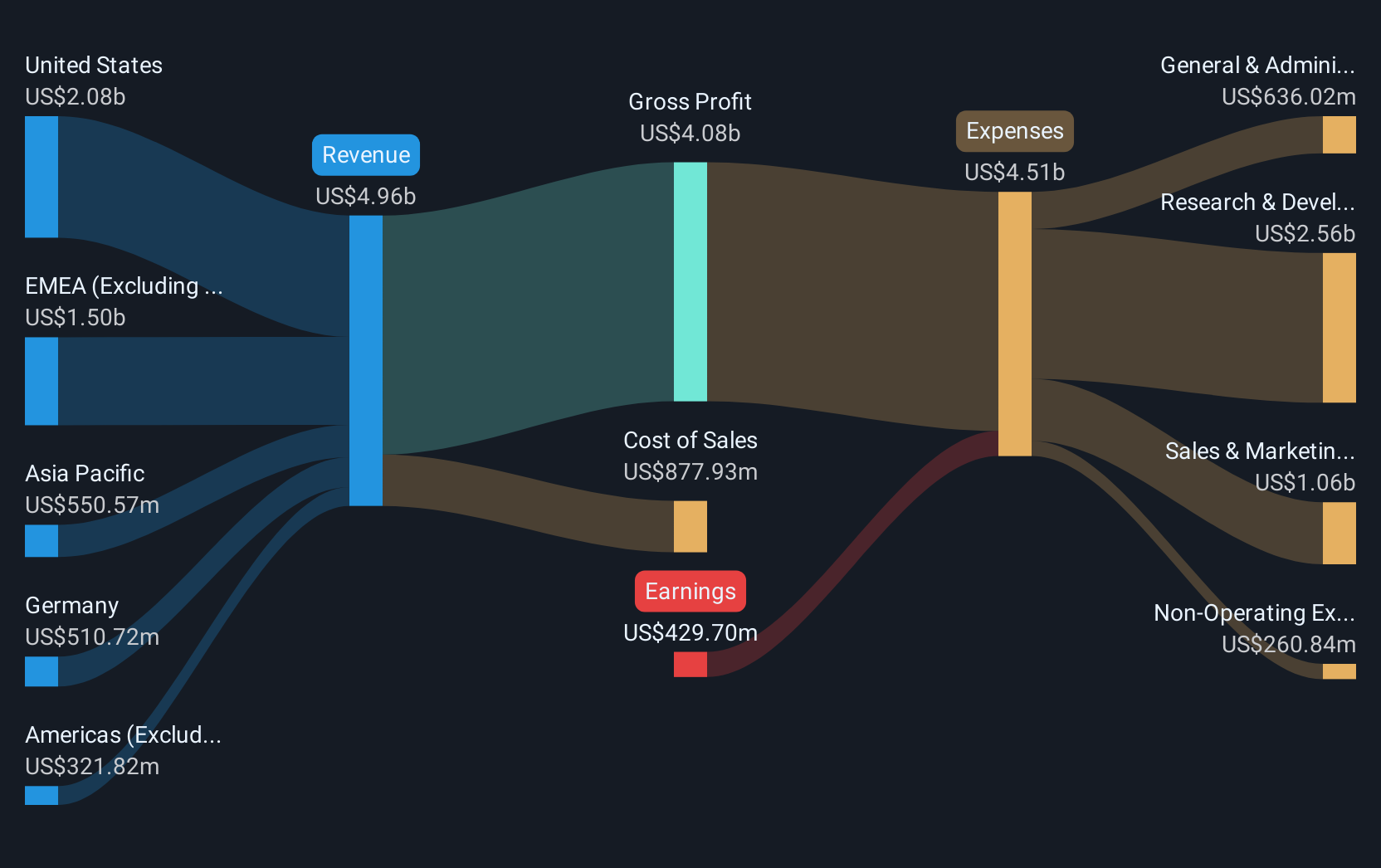

Atlassian (NasdaqGS:TEAM) has recently been in the spotlight after announcing its Q2 2025 earnings, showcasing a revenue increase to USD 1,286 million but still reporting a net loss of USD 38 million, albeit improved from the previous year. The tech company's stock recorded a 12.55% decline over the last quarter amid these mixed financial results and broader market turbulence. The company's ongoing share buyback program, with 368,000 shares repurchased, did not significantly buoy its stock performance. Meanwhile, tech-heavy Nasdaq experienced three consecutive weeks of declines, pressured by macroeconomic concerns and lackluster job reports, contributing to the pressure on Atlassian's share price. Despite these challenges, the appointment of Christian Smith to the board could signal strategic realignments. Although CEO Jay Parikh’s exit might have stirred some investor uncertainty, Atlassian's operational endurance continues to catch analytical interest against a backdrop of volatile market conditions.

Take a closer look at Atlassian's potential here.

The last five years have seen Atlassian achieve a commendable total return of 86.70%, combining share price appreciation and dividends. Despite its unprofitability, Atlassian has shown resilience with a consistent revenue increase, such as the Q4 FY 2024 report announcing full year revenue at US$4.36 billion, up from US$3.53 billion. This growth trajectory aligns with its revenue forecast to outpace the broader US market. However, the company appears expensive based on its Price-To-Sales Ratio compared to industry averages, which might concern potential investors.

Noteworthy events that could have contributed to the performance include Atlassian's multi-year collaboration with Amazon Web Services announced in December 2024, aiming to advance cloud migration for enterprise customers. The extensive share buyback program, with 4.64 million shares repurchased, underscores efforts to enhance shareholder value, even as executive changes such as the appointment of Brian Duffy as Chief Revenue Officer indicate a focus on refining revenue strategies. These elements combined may explain the substantial long-term shareholder returns.

- Learn how Atlassian's intrinsic value compares to its market price with our detailed valuation report.

- Gain insight into the risks facing Atlassian and how they might influence its performance—click here to read more.

- Got skin in the game with Atlassian? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TEAM

Atlassian

Through its subsidiaries, designs, develops, licenses, and maintains various software products worldwide.

Flawless balance sheet with high growth potential.