Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SNPS

Assessing Synopsys (SNPS) Valuation After Recent Share Price Weakness And Ansys Integration Outlook

Synopsys stock performance and recent context

Synopsys (SNPS) has been under pressure in recent months, with the share price showing a 9% decline over the past month and a similar 9% decline over the past 3 months.

Over the past year, Synopsys has recorded a 4.7% negative total return, while revenue of US$8,007.7m and net income of US$1,105.4m sit alongside annual revenue and net income growth figures of 11.9% and 20.3% respectively.

See our latest analysis for Synopsys.

The recent 7 day share price return of a 3.7% decline and year to date share price return of an 11.7% decline point to fading short term momentum, even as the 5 year total shareholder return of 85.8% reflects a much stronger long term picture.

If Synopsys has you thinking more broadly about opportunities around AI infrastructure and chip design, this is a good moment to scan our list of 34 AI infrastructure stocks as potential next ideas to research.

With the shares pulling back and the stock trading at a small discount to one intrinsic estimate and to some analyst targets, the key question now is whether Synopsys is genuinely undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 23.3% Undervalued

At a last close of $424.32 versus a narrative fair value of $553.40, the most followed view sees Synopsys trading at a meaningful discount, with that gap tied to long term earnings and cash flow assumptions rather than short term sentiment.

The acquisition and integration of Ansys positions Synopsys as the global leader in engineering solutions from silicon to systems, dramatically expanding its addressable market into sectors like automotive, industrial, and aerospace. This should drive long-term top-line growth as more sophisticated and complex products (especially AI-powered and smart devices) require robust simulation, analysis, and EDA tools.

Curious what kind of revenue mix, margin path, and future earnings multiple are baked into that fair value figure, and how they tie back to this Ansys story plus AI heavy design demand, without just relying on headline growth rates, guidance snippets or simple P/E charts.

Result: Fair Value of $553.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can shift quickly if China related export restrictions deepen, or if the Ansys integration adds more cost and complexity than expected.

Find out about the key risks to this Synopsys narrative.

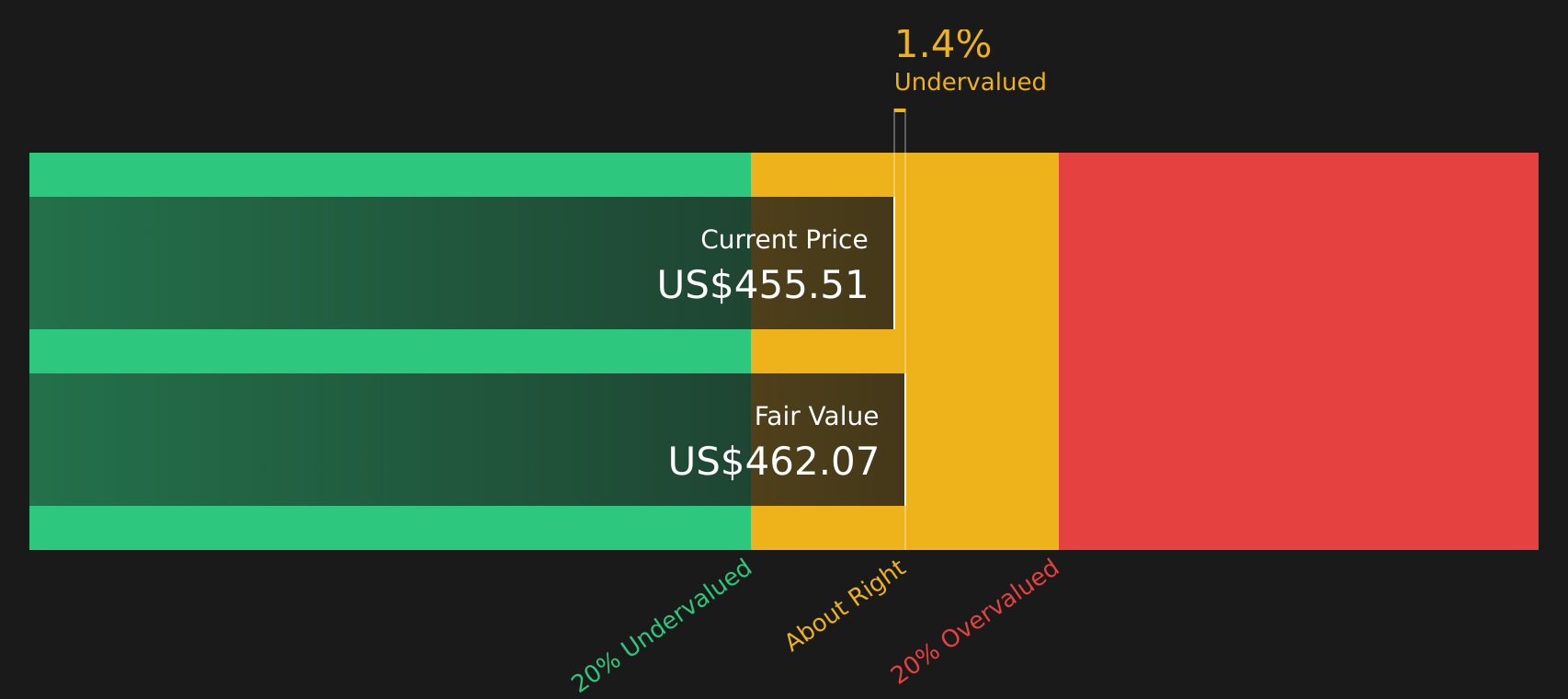

Another Angle On Valuation

Our SWS DCF model points to a fair value of $450.14 for Synopsys, which is only a 5.7% premium to the current $424.32 share price. That is far less than the 23.3% upside suggested by the narrative fair value of $553.40. Which yardstick do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mix of opportunity and concern around Synopsys leaves you on the fence, now is a good time to look through the underlying data yourself, compare both sides, and weigh up the 3 key rewards and 3 important warning signs before deciding what it all means for you.

Looking for more investment ideas?

If Synopsys is on your radar, do not stop there. Use this moment to broaden your watchlist with a few focused stock ideas built from hard numbers.

- Target stability first by reviewing companies in our 75 resilient stocks with low risk scores that score well on resilience and measured risk profiles.

- Hunt for quality at a discount through the 49 high quality undervalued stocks, highlighting stocks where fundamentals and price are not fully aligned.

- Channel your search into firms with robust finances using the solid balance sheet and fundamentals stocks screener (40 results) that filters for stronger balance sheets and healthier fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SNPS

Synopsys

Provides design IP solutions in the semiconductor and electronics industries.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.9% undervalued

148 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0327.9% undervalued

33 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.8% undervalued

16 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.8% undervalued

264 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.0% overvalued

130 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.7% undervalued

160 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0