Advertisement

- United States

- /

- Software

- /

- NasdaqCM:SNCR

Synchronoss Technologies (NASDAQ:SNCR) Seems To Be Using A Lot Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Synchronoss Technologies, Inc. (NASDAQ:SNCR) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Synchronoss Technologies

What Is Synchronoss Technologies's Debt?

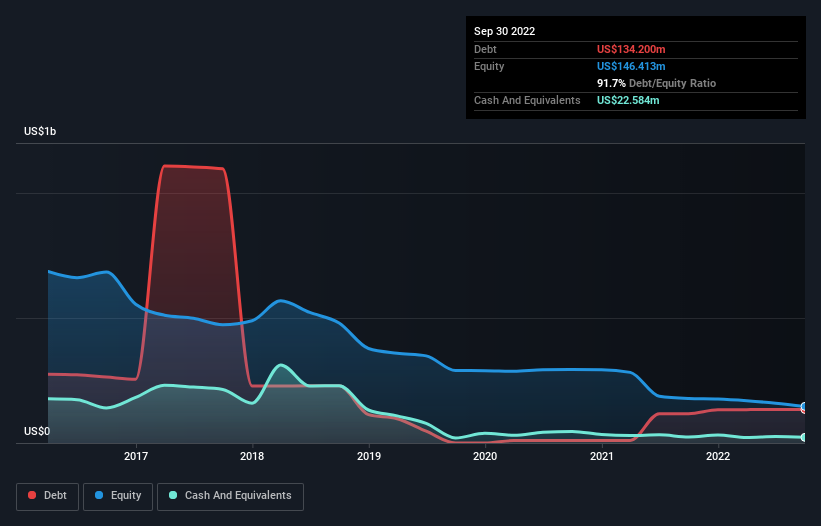

The image below, which you can click on for greater detail, shows that at September 2022 Synchronoss Technologies had debt of US$134.2m, up from US$117.5m in one year. However, it also had US$22.6m in cash, and so its net debt is US$111.6m.

How Strong Is Synchronoss Technologies' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Synchronoss Technologies had liabilities of US$81.7m due within 12 months and liabilities of US$170.8m due beyond that. On the other hand, it had cash of US$22.6m and US$45.9m worth of receivables due within a year. So it has liabilities totalling US$184.0m more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$56.9m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Synchronoss Technologies would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn't worry about Synchronoss Technologies's net debt to EBITDA ratio of 3.5, we think its super-low interest cover of 1.1 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. One redeeming factor for Synchronoss Technologies is that it turned last year's EBIT loss into a gain of US$15m, over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Synchronoss Technologies's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. During the last year, Synchronoss Technologies burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Synchronoss Technologies's conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to grow its EBIT isn't such a worry. Taking into account all the aforementioned factors, it looks like Synchronoss Technologies has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Synchronoss Technologies (1 is a bit concerning!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SNCR

Synchronoss Technologies

Provides white label cloud software and services in North America, Europe, the Middle East, Africa, and the Asia Pacific.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

47 followersusers have followed this narrative

4 commentsusers have commented on this narrative

28 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$961.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6434.2% undervalued

32 followersusers have followed this narrative

5 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

YI

yiannisz on Alphabet ·

The Real Power Behind Alphabet’s Growth

Fair Value:US$192.5470.7% overvalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on RELX ·

RELX: The Quiet Compounder Powering Law, Science, and Risk Intelligence

Fair Value:US$41.224.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on CVS Health ·

Why CVS’s Valuation Signals Opportunity

Fair Value:US$104.0122.8% undervalued

102 followersusers have followed this narrative

9 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

70 followersusers have followed this narrative

13 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.0% undervalued

1029 followersusers have followed this narrative

6 commentsusers have commented on this narrative

29 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25422.1% overvalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative