Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ROP

Is There Now An Opportunity In Roper Technologies (ROP) After Recent Software Pivot?

Reviewed by Bailey Pemberton

- If you are wondering whether Roper Technologies at around US$414 per share still lines up with its underlying worth, this breakdown is designed to help you connect the current price with the fundamentals behind it.

- The stock has seen a 4.7% decline over the past week, a 6.7% decline over the past month, and it is down 4.7% year to date and 19.7% over the last year, which may have changed how some investors view its potential and risk.

- Recent news coverage around Roper Technologies has focused on its positioning as a software focused business and how that aligns with broader market sentiment on higher quality, recurring revenue models. This context helps frame whether recent share price weakness is simply sentiment driven or connected to how investors currently judge its long term prospects.

- Even with these returns, Roper Technologies holds a valuation score of 6 out of 6. Next we will walk through how different valuation methods line up with that score before closing with a practical way to interpret all of this for your own process.

Find out why Roper Technologies's -19.7% return over the last year is lagging behind its peers.

Approach 1: Roper Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth today by projecting its future cash flows and discounting them back to the present using a required rate of return.

For Roper Technologies, the model starts with last twelve month free cash flow of about $2.4b, then uses analyst forecasts and longer term extrapolations to build a 2 stage Free Cash Flow to Equity view. For example, projected free cash flow for 2028 is $3.9b, and the ten year path from 2026 through 2035 is based on a mix of analyst inputs and estimated growth rates provided by Simply Wall St.

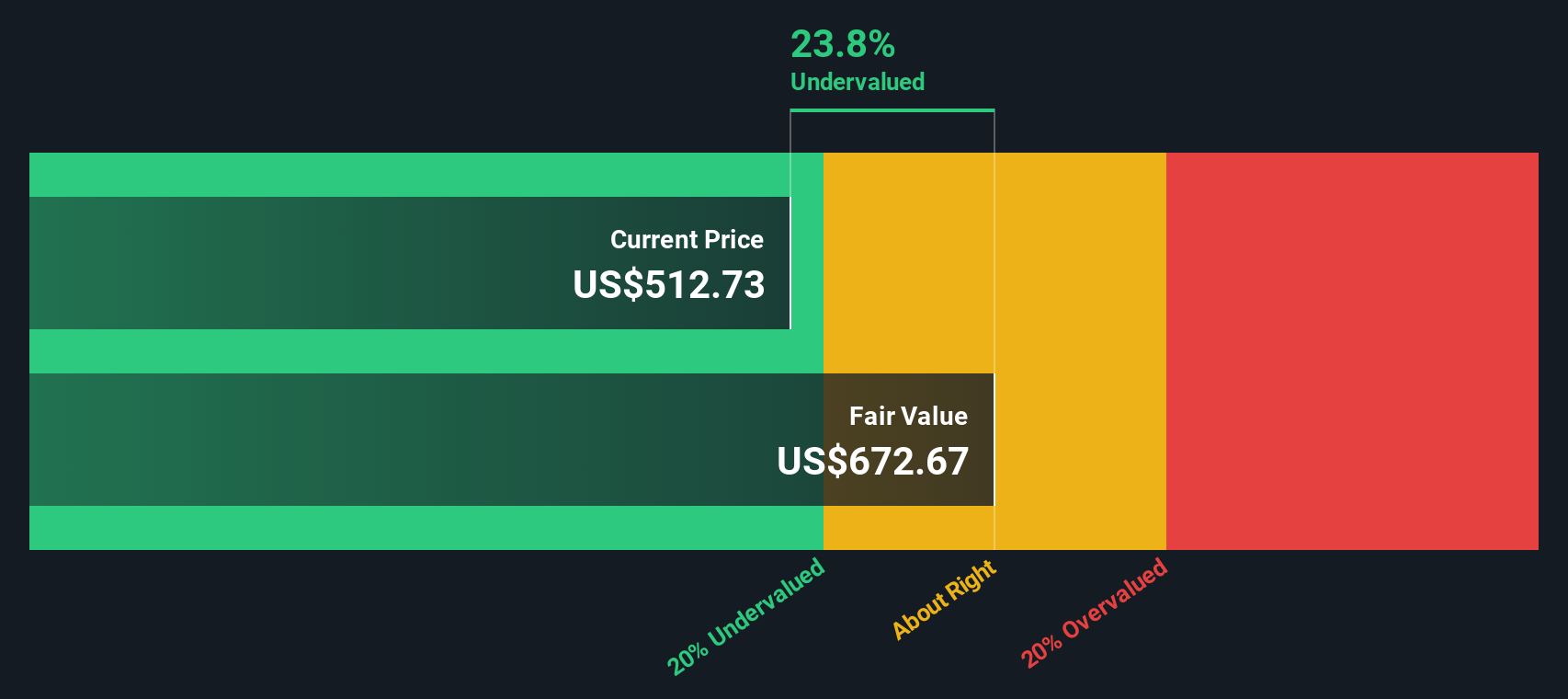

When all those future cash flows are discounted back and summed, the model arrives at an intrinsic value of about $715.92 per share. Compared with a current share price around $414, this suggests the stock is trading at roughly a 42.1% discount. This indicates a meaningful gap between the DCF estimate and where the market is pricing the shares today.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Roper Technologies is undervalued by 42.1%. Track this in your watchlist or portfolio, or discover 867 more undervalued stocks based on cash flows.

Approach 2: Roper Technologies Price vs Earnings

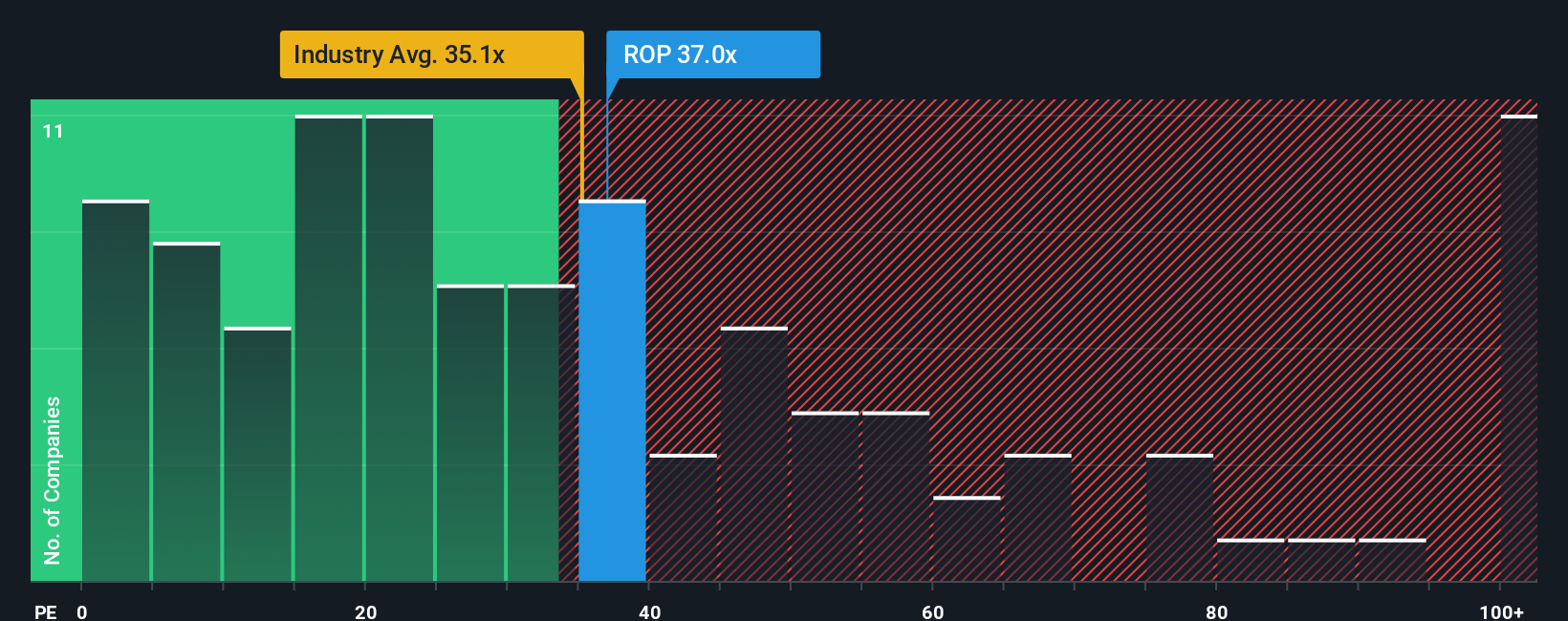

For a profitable business like Roper Technologies, the P/E ratio is a useful way to connect the share price to the earnings that support it. In general, higher expected earnings growth and lower perceived risk can justify a higher P/E, while slower growth or higher risk usually points to a lower, more conservative range.

Roper Technologies currently trades on a P/E of 28.40x. That sits below both the broader Software industry average of 31.77x and the peer group average of 48.36x. Simply Wall St also calculates a proprietary “Fair Ratio” for the company of 32.21x, which is an estimate of what the P/E might be given its earnings growth profile, profit margins, risks, industry and market cap.

This Fair Ratio aims to be more tailored than a simple peer or industry comparison because it adjusts for company specific factors rather than assuming that all software names deserve the same multiple. With the current 28.40x P/E sitting below the 32.21x Fair Ratio, the P/E based view points to Roper Technologies looking undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Roper Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, which are simply your story about Roper Technologies linked directly to a forecast and a fair value. They are built on your own assumptions for future revenue, earnings and margins, and are available on Simply Wall St's Community page. There, millions of investors compare their Fair Value with the current price, see how that view shifts when news or earnings arrive, and observe how some investors might lean toward the higher US$714 analyst target while others sit closer to the lower US$460 view, all within a single, easy to use framework that turns your perspective into numbers you can track over time.

Do you think there's more to the story for Roper Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROP

Roper Technologies

Designs and develops vertical software and technology enabled products in the United States, Canada, Europe, Asia, and internationally.

Very undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.0% undervalued

49 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23056.0% overvalued

53 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$123.1512.9% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Rox Resources ·

Developer to Producer: Debt-Free Path, A$965M Post-Tax NPV, and Massive Gold Leverage

Fair Value:AU$6.1693.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

JO

John_Eric on MercadoLibre ·

MercadoLibre and the Spreadsheet Trick That Decides Everything

Fair Value:US$4.72k61.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.2% undervalued

86 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5452.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

AN

AnalystConsensusTarget on Broadcom ·

AVGO: Upcoming AI Chip Production With Key Partner Will Shape Competitive Position

Fair Value:US$523.7323.4% undervalued

689 followersusers have followed this narrative

3 commentsusers have commented on this narrative

5 likesusers have liked this narrative