Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ROP

Does Roper Technologies’ 2025 Slide Create a Long Term Opportunity for Investors?

Reviewed by Bailey Pemberton

- Wondering if Roper Technologies is quietly turning into a value opportunity while everyone is distracted by flashier tech names? You are not alone, and that is exactly what we are going to unpack here.

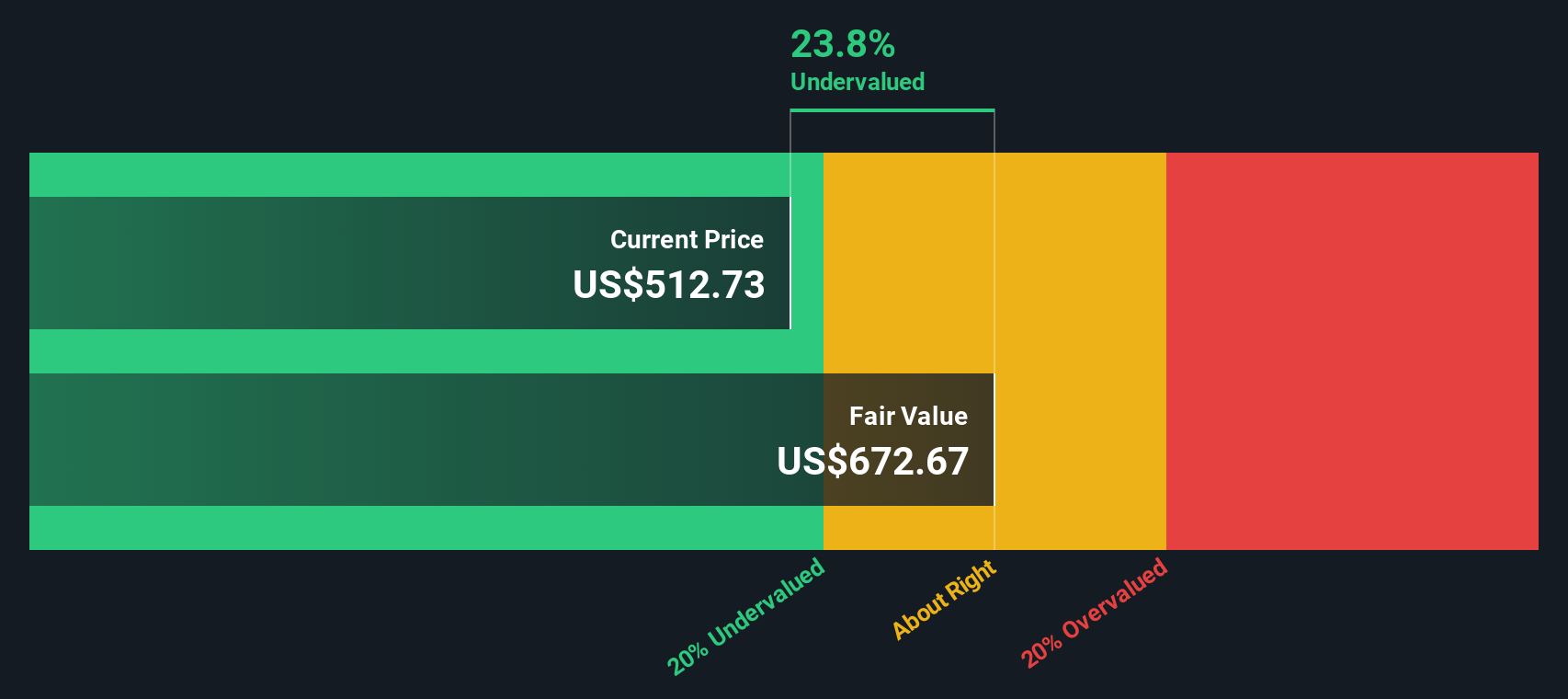

- Despite being a high quality software and technology conglomerate, the stock has slipped, down about 0.8% over the last week, 1.7% over the last month, and 13.9% year to date, leaving it roughly 19.1% lower than a year ago even though 5 year returns are still positive at 8.1%.

- Recent moves have less to do with company specific factors and more with a market that is re rating long duration, high quality compounders as investors rotate between growth, quality, and income. At the same time, Roper has kept leaning into its asset light software and information businesses, which the market has historically rewarded with premium multiples when sentiment turns more constructive again.

- On our checks, Roper currently scores a 6/6 valuation score, suggesting it screens as undervalued on every one of our metrics. Next we will walk through those valuation approaches, and then wrap up with an even more intuitive framework for understanding what the numbers are really saying about its long term value.

Find out why Roper Technologies's -19.1% return over the last year is lagging behind its peers.

Approach 1: Roper Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by taking its expected future cash flows and discounting them back to today, so we can compare that value directly to the current share price.

Roper Technologies is currently generating about $2.4 Billion in free cash flow, and analysts expect this to keep growing steadily as the company leans further into asset light software and information businesses. Based on analyst forecasts and Simply Wall St extrapolations, free cash flow is projected to reach roughly $6.4 Billion by 2035.

When these projected cash flows are discounted back to today using a 2 stage Free Cash Flow to Equity model, the estimated intrinsic value comes out at about $714.78 per share. Compared to the current market price, this implies the stock is trading at roughly a 38.1% discount.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Roper Technologies is undervalued by 38.1%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

Approach 2: Roper Technologies Price vs Earnings

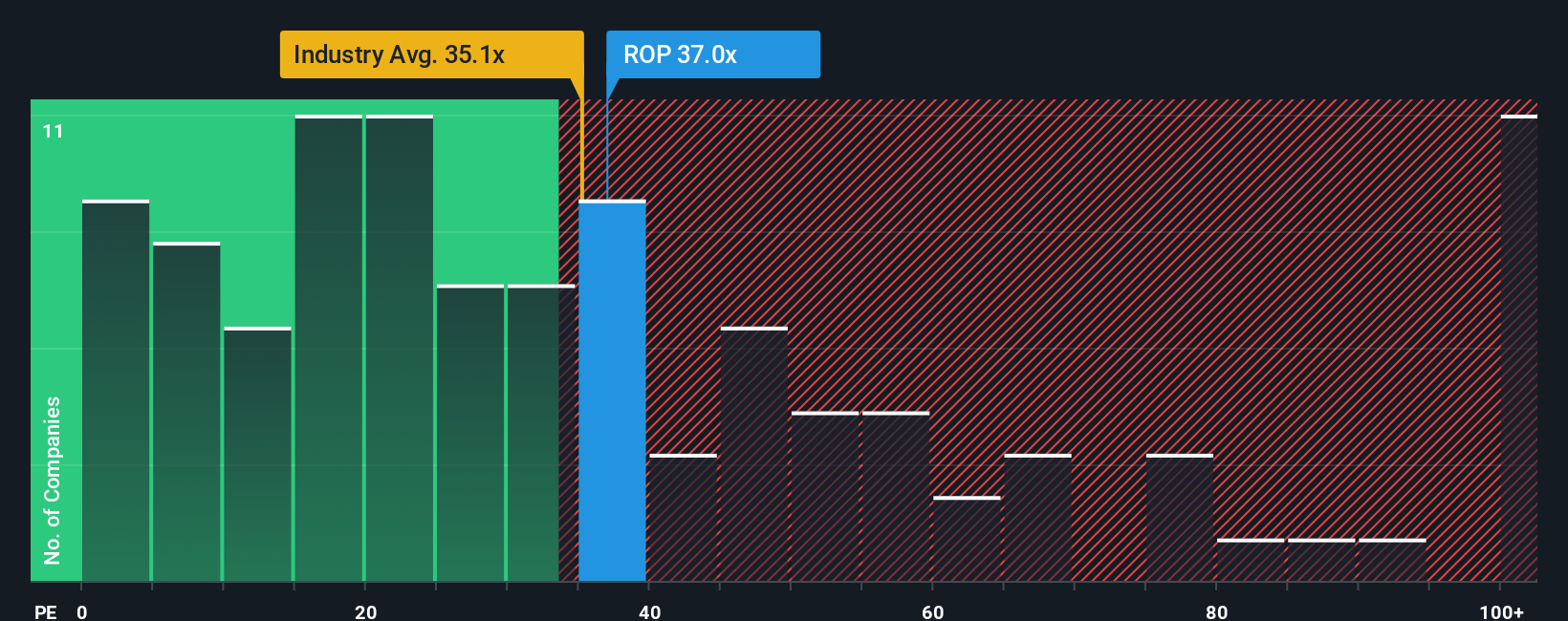

For profitable, steadily growing companies like Roper Technologies, the price to earnings multiple is a useful shorthand for how much investors are willing to pay for each dollar of current profits. In general, faster growth and lower perceived risk justify a higher PE, while slower growth or more uncertainty should translate into a lower, more cautious multiple.

Roper currently trades on a PE of about 30.3x, which is slightly below the broader Software industry average of roughly 31.9x and well below the peer group average of around 54.7x. Simply Wall St also calculates a proprietary Fair Ratio of 33.1x for Roper, which reflects what investors might reasonably pay given its earnings growth profile, margins, industry, size, and risk factors.

This Fair Ratio is more tailored than a simple comparison with peers or the sector, because it adjusts for the specific characteristics of Roper rather than assuming all software companies deserve the same multiple. With the actual PE of 30.3x sitting below the Fair Ratio of 33.1x, the multiple based view points to Roper Technologies being modestly undervalued at current prices.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Roper Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives, a simple framework that lets you attach a clear story about Roper Technologies future to the numbers behind your own fair value, revenue, earnings, and margin assumptions. A Narrative links three things together: your view of the business, a forward looking financial forecast, and the fair value that drops out of those assumptions, so you can see whether the current price makes sense for your story. On Simply Wall St, millions of investors build these Narratives on the Community page, then compare their fair value to today’s share price to decide whether Roper looks like a buy, a hold, or a sell. Because Narratives are updated dynamically as new news, guidance, or earnings arrive, your valuation stays in sync with reality instead of going stale. For example, one Roper Narrative might lean bullish and land near the upper analyst target of around $714 per share, while a more cautious view could sit closer to $460, showing how different perspectives can coexist and helping you choose which story, and which price, you actually believe.

Do you think there's more to the story for Roper Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROP

Roper Technologies

Designs and develops vertical software and technology enabled products in the United States, Canada, Europe, Asia, and internationally.

Very undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7833.2% undervalued

31 followersusers have followed this narrative

5 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Quanta Services ·

Quanta Services (PWR): Strengthening the Backbone of the AI Power Grid.

Fair Value:US$5464.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on KLA ·

KLA Corporation (KLAC): Engineering Yield in the Age of Chiplets and Sub-2nm Nodes.

Fair Value:US$1.5k4.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Monolithic Power Systems ·

Monolithic Power Systems (MPWR): The AI "Power Play" Facing a Transition from Scarcity to Scale.

Fair Value:US$1.27k16.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1302 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative