Advertisement

- United States

- /

- Software

- /

- NasdaqGS:RDWR

Radware (RDWR) Valuation Check After ZombieAgent AI Security Discovery

Why Radware’s AI Security Discovery Matters for Investors

Radware (RDWR) recently reported the discovery of ZombieAgent, a zero-click indirect prompt injection vulnerability in OpenAI’s Deep Research agent, exposing risks such as invisible data theft and persistent agent hijacking for enterprise users.

The company plans to publish full technical details and defense guidance through its Security Research Center. This keeps the focus on how its cybersecurity capabilities align with demand for protection around fast growing AI agent deployments.

See our latest analysis for Radware.

The ZombieAgent disclosure lands at a time when Radware’s 1 month share price return of 5.16% and 1 week return of 2.41% point to improving short term momentum, even though the 3 month share price return of 2.14% decline contrasts with a 1 year total shareholder return of 13.29% and a 3 year total shareholder return of 22.28%, with the stock last closing at US$24.64.

If this kind of AI security story has your attention, it is a good moment to scan other high growth tech and AI stocks that could benefit as demand for protection around advanced software grows.

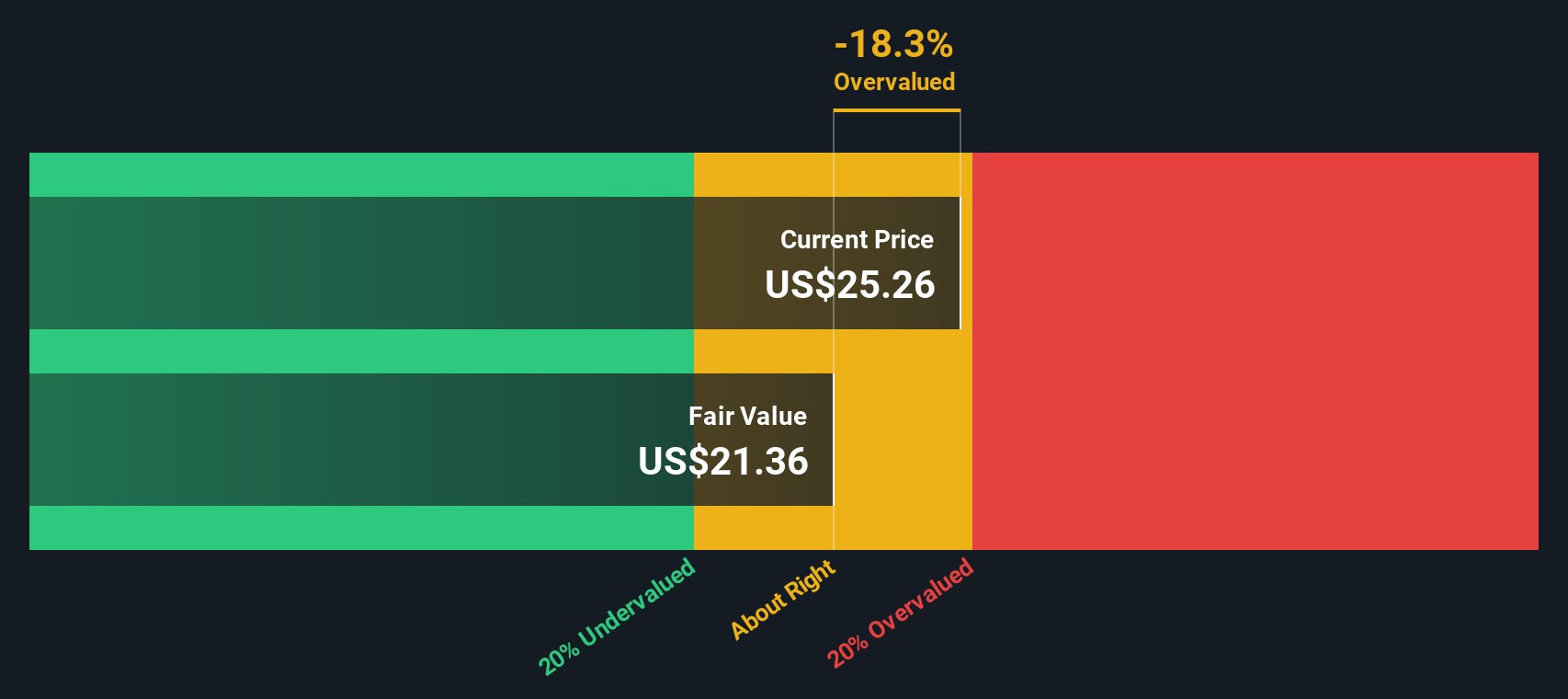

With Radware trading at US$24.64 versus an average analyst target of about US$30.67 and an intrinsic premium flagged by its model, you have to ask: is there still upside here, or is future growth already priced in?

Price-to-Earnings of 64.2x: Is it justified?

Radware's current P/E of 64.2x alongside a last close of US$24.64 points to a richer pricing than many peers in the software space.

The P/E ratio compares the share price to earnings per share, so for a company like Radware it reflects what investors are willing to pay for each dollar of earnings. For a cybersecurity and application delivery business, a higher P/E can reflect expectations about future profitability or the perceived value of its solutions rather than just current earnings.

According to the Statements Data, Radware is described as expensive on a P/E basis both versus a peer group average of 25.1x and the broader US Software industry average of 31.8x. With earnings having declined by 20.6% per year over the past 5 years and only recently turning profitable, that higher multiple suggests the market is currently placing a premium on Radware's earnings profile compared to many software names.

Compared to peers, a P/E of 64.2x is more than double the cited industry average of 31.8x, and also well above the 25.1x peer average, which underscores how much extra investors are currently paying per dollar of earnings relative to similar companies.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 64.2x (OVERVALUED)

However, you still have to weigh the risk that a 64.2x P/E, alongside an intrinsic premium, could limit upside if growth or AI security momentum stalls.

Find out about the key risks to this Radware narrative.

Another View: SWS DCF Model Flags a Premium

While the 64.2x P/E already looks rich, our DCF model also points to Radware trading above its estimated fair value, with the shares at US$24.64 versus a DCF value of US$17.25. If both earnings and cash flow lenses point to a premium, what exactly is the market paying up for?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Radware for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Radware Narrative

If you look at the numbers and come to a different conclusion, or simply prefer to test your own view against the data, you can build a complete, personalised thesis in just a few minutes with Do it your way.

A great starting point for your Radware research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Radware’s story has you thinking bigger, do not stop here. Broaden your watchlist with ideas that tap into different themes and potential return profiles.

- Spot early stage opportunities with stronger balance sheets and business quality by scanning these 3539 penny stocks with strong financials before they hit everyone’s radar.

- Explore a wider range of AI-related companies by checking out these 24 AI penny stocks that focus on artificial intelligence themes.

- Identify potential mispricings by filtering for these 868 undervalued stocks based on cash flows to find companies trading at levels that may not fully reflect their cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:RDWR

Radware

Develops, manufactures, and markets cyber security and application delivery solutions for cloud, on-premises, and software defined data centers.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative