Advertisement

- United States

- /

- Software

- /

- NasdaqGS:PONY

Has Pony AI’s Autonomous Driving Progress Already Driven the Share Price Too Far in 2025?

Reviewed by Bailey Pemberton

- Whether you see Pony AI as a hidden bargain or already priced for perfection, this piece will walk through what the current share price really implies.

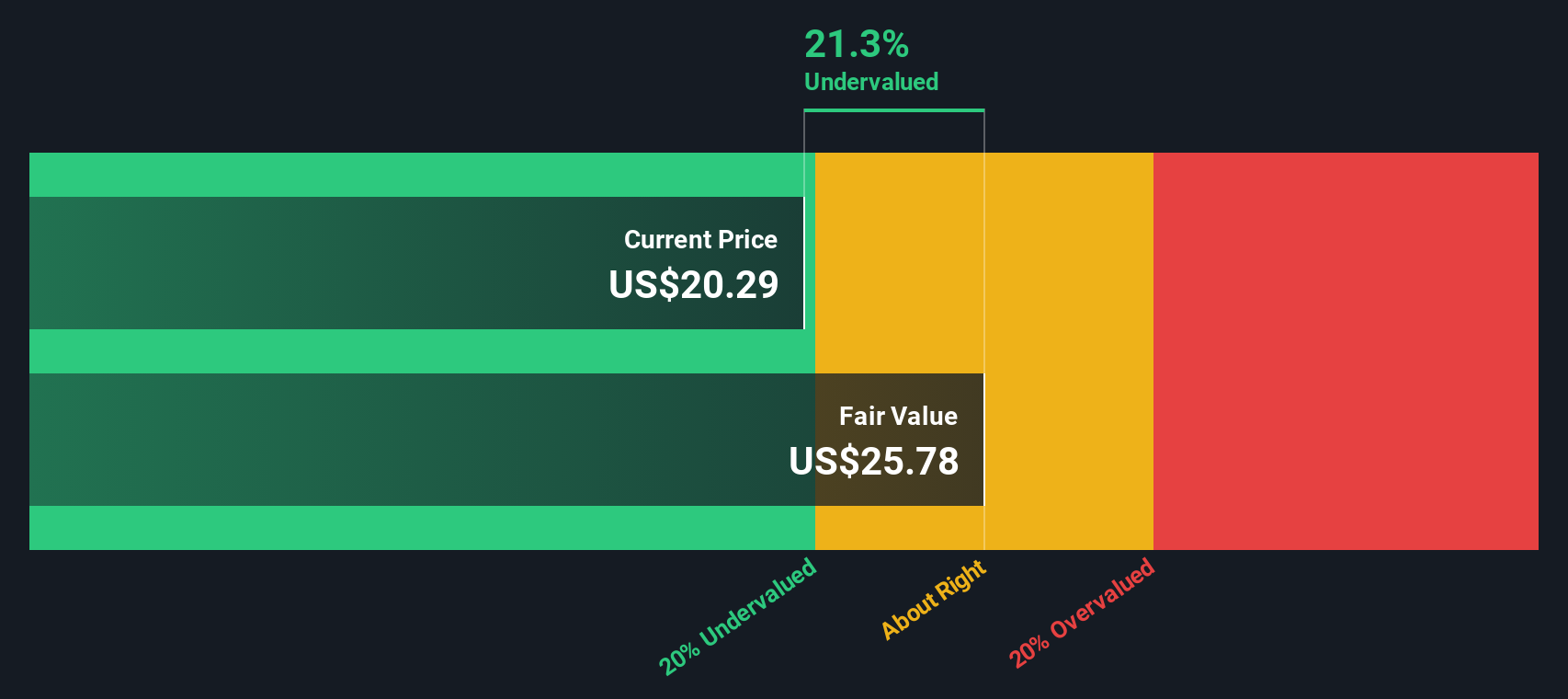

- The stock has been lively lately, climbing 10.7% over the last week, 24.5% over the past month, and 20.4% over the last year, even though it is only up 3.2% year to date from its last close at $15.68.

- Investors have been reacting to a steady drumbeat of headlines around autonomous driving partnerships and regulatory milestones in key U.S. and Chinese cities. Together, these developments are shaping expectations for Pony AI's commercialization timeline. At the same time, updates on new pilot programs and expanded testing zones have fueled a narrative that the company could be closer to scaled deployment than many once assumed.

- Despite the excitement, Pony AI currently scores just 2/6 on our valuation checks. This suggests the market might be paying up for growth that still needs to be earned. Next, we will unpack the usual valuation methods and then finish with a more powerful way to think about what this stock is really worth.

Pony AI scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Pony AI Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth today by projecting its future cash flows and discounting them back to the present. For Pony AI, this uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections in $.

The company currently has last twelve month free cash flow of about $175 million in the red, highlighting that it is still in an investment heavy phase. Analyst forecasts and extrapolations in the model see this swinging into positive territory, with free cash flow projected to reach around $2.61 billion by 2035, moving from negative outflows over the next couple of years to inflows later in the decade.

When all these projected cash flows are discounted back, Simply Wall St estimates an intrinsic value of about $55.66 per share. Compared with the recent share price of $15.68, the DCF output implies the stock is roughly 71.8% below that intrinsic value estimate, indicating the market price is lower than this particular valuation model suggests for Pony AI's long term cash generation potential.

Result: UNDERVALUED (model-based)

Our Discounted Cash Flow (DCF) analysis suggests Pony AI is undervalued by 71.8%. Track this in your watchlist or portfolio, or discover 905 more undervalued stocks based on cash flows.

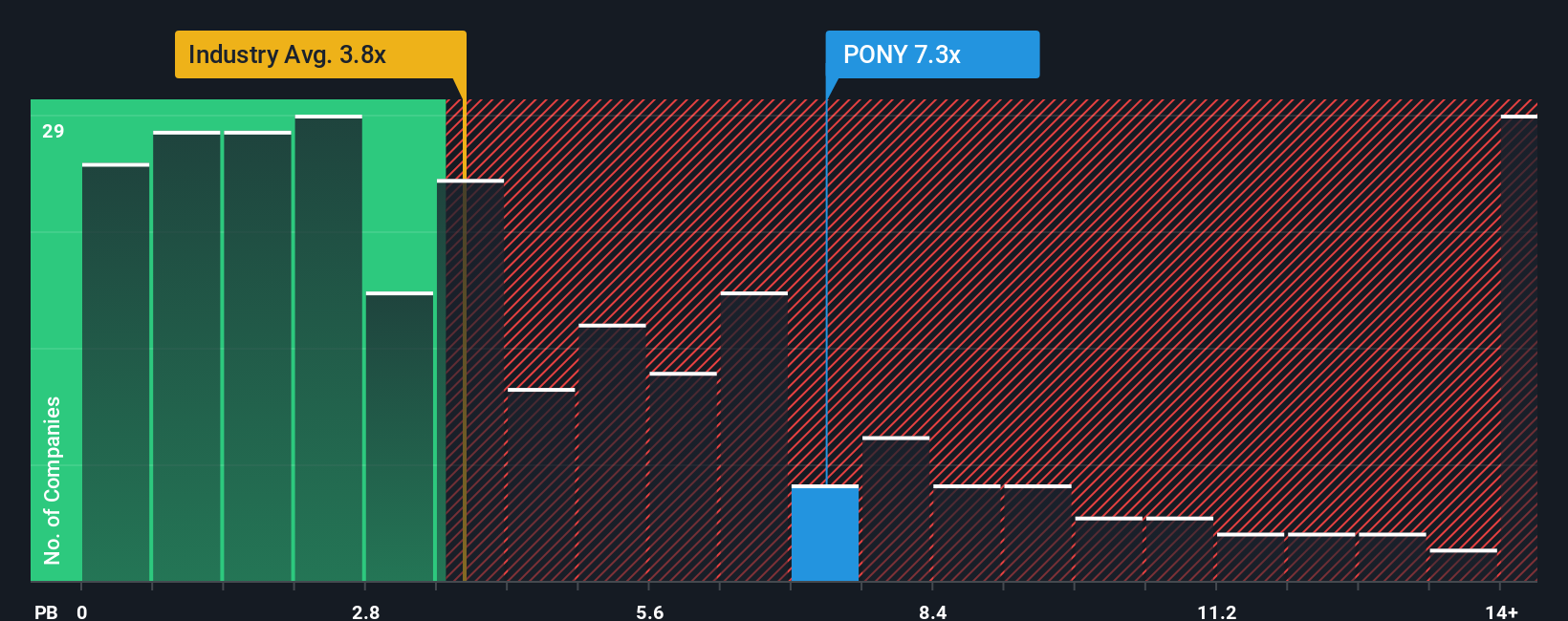

Approach 2: Pony AI Price vs Book

For companies that are still loss making and investing heavily in future growth, the price to book ratio is often a more useful yardstick than earnings based metrics, because it compares the share price with the accounting value of the net assets backing the business.

In general, investors are willing to pay a higher price to book multiple when they expect stronger growth and see lower risk, while slower or more uncertain stories tend to trade closer to, or even below, their book value. Pony AI currently trades at about 8.48x book value, which is well above both the Software industry average of roughly 3.41x and the peer group average of around 3.84x, suggesting the market is already pricing in a premium for its autonomous driving potential.

Simply Wall St also uses a proprietary Fair Ratio, which estimates what a reasonable price to book multiple should be for Pony AI given its specific growth outlook, risk profile, profitability, industry and market cap. This tailored measure is more informative than a simple peer or industry comparison, because it adjusts for company level nuances rather than assuming all software names deserve the same pricing. On this basis, Pony AI’s current 8.48x price to book looks high relative to where the Fair Ratio would likely sit, pointing to a stretched valuation.

Result: OVERVALUED

PB ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1459 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pony AI Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework that lets you attach a clear story, your assumptions about Pony AI’s future revenue, earnings and margins, to the numbers behind a fair value estimate. A Narrative links three things together: what you believe about the company, how that belief translates into a financial forecast, and the fair value that drops out of those forecasts, so you can quickly see whether the current share price looks attractive or expensive. On Simply Wall St, millions of investors use Narratives on the Community page as an easy, accessible tool to compare their fair value with today’s market price and decide whether to buy, hold or sell. Because Narratives update dynamically when new information like news, earnings or regulatory developments arrives, your view of Pony AI can evolve in real time rather than staying stuck in an outdated model. For example, one investor’s Pony AI Narrative might support a fair value far above the current price while another’s, using more conservative growth and margin assumptions, might land well below it.

Do you think there's more to the story for Pony AI? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PONY

Pony AI

Through its subsidiaries, engages in the autonomous mobility business in the People’s Republic of China and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5297.0% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3076.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative