- United States

- /

- Software

- /

- NasdaqGS:PEGA

Pegasystems (PEGA) Confirms US$0.03 Dividend Per Share for Fourth Quarter 2025

Reviewed by Simply Wall St

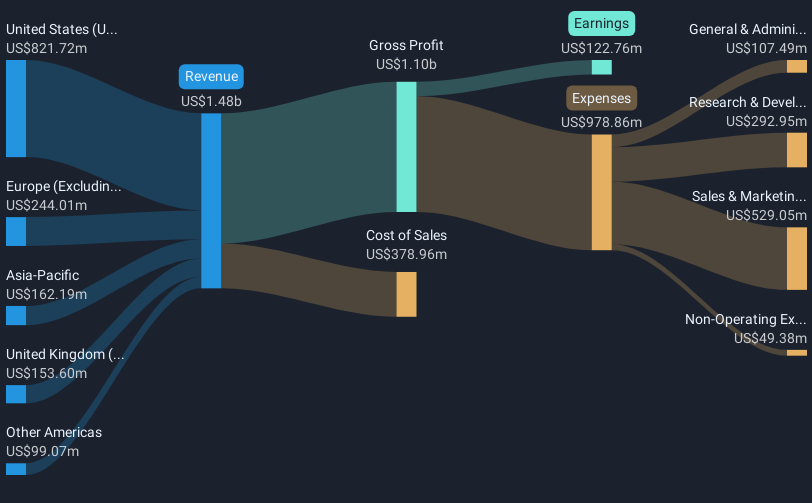

Pegasystems (PEGA) recently affirmed its quarterly dividend of $0.03 per share, maintaining its dividend policy, while announcing its third quarter earnings results with substantial year-over-year growth. The company's stock appreciated by 15% in the last quarter, potentially influenced by multiple factors. These include Pegasystems' continued dividend payout and its strategic initiatives like the introduction of Pega Self-Service Agent, which leverages advanced AI technologies. Moreover, the recent uptrend in the broader Nasdaq, driven largely by bullish tech stocks, may have complemented Pegasystems' gains, aligning it with industry growth trends despite no direct correlation.

We've spotted 1 risk for Pegasystems you should be aware of.

The recent affirmation of Pegasystems' quarterly dividend and its strong third quarter earnings growth have the potential to enhance investor confidence and support the positive narrative around its revenue and earnings trajectory. While the dividend signals financial stability and commitment to shareholders, the introduction of Pega Self-Service Agent leveraging AI technologies could contribute positively to future revenue and margin improvements. As the company focuses on AI and cloud services, investors may see continued benefits both in customer retention and financial performance.

Pegasystems shares have experienced a substantial total return of 228.72% over the past three years, illustrating significant growth beyond short-term fluctuations. Over the past year, Pegasystems outperformed the US Software industry, which returned 26.6%. This overall strong performance provides context for recent share price movement and reflects improved market positioning and competitiveness for Pegasystems.

With the current share price at $58.07, Pegasystems trades at a slight discount to the consensus price target of $62.68, reflecting an expected upside of approximately 7.9%. This could suggest confidence in achieving forecasted revenue growth and increased profit margins as outlined in analyst projections. However, macroeconomic uncertainties and potential currency fluctuations remain, which could influence Pegasystems' revenue and earnings forecasts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PEGA

Pegasystems

Develops, markets, licenses, hosts, and supports enterprise software in the United States, rest of the Americas, the United Kingdom, rest of Europe, the Middle East, Africa, and the Asia-Pacific.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion