Advertisement

- United States

- /

- Software

- /

- NasdaqGS:OPRA

Is Opera (OPRA) Offering Value After Its Strong Multi Year Share Price Performance

Reviewed by Bailey Pemberton

- Wondering if Opera's recent share price puts it in the bargain bin or the overhyped aisle? This article breaks down what the numbers say about value.

- At a last close of US$17.23, Opera's share price comes with recent returns of 0.6% over 7 days, 25.6% over 30 days, 21.1% year to date, 16.3% over 1 year, 67.0% over 3 years, and 105.9% over 5 years.

- These moves sit against a backdrop of ongoing interest in Opera as a software name, with headlines frequently focusing on its role as a browser platform and the broader attention on tech related stocks. This context is important because sentiment around product positioning and sector themes can influence how the market prices the shares.

- On Simply Wall St's 6 point valuation check, Opera scores a full 6 out of 6. The rest of this piece will unpack what that means across different valuation methods and then point to a more complete way to think about value beyond any single model.

Approach 1: Opera Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash Opera is expected to generate in the future, then discounts those projections back to what they might be worth in today’s dollars. It is essentially asking what a stream of future cash flows is worth right now.

For Opera, the latest twelve month free cash flow is about US$96.2 million. Using a 2 Stage Free Cash Flow to Equity model, analyst estimates and extrapolations point to projected free cash flow of US$276.9 million in 2030, with interim projections between 2026 and 2035 also feeding into the calculation. Simply Wall St uses analyst inputs for the earlier years and then extends the series using its own growth assumptions for the later years.

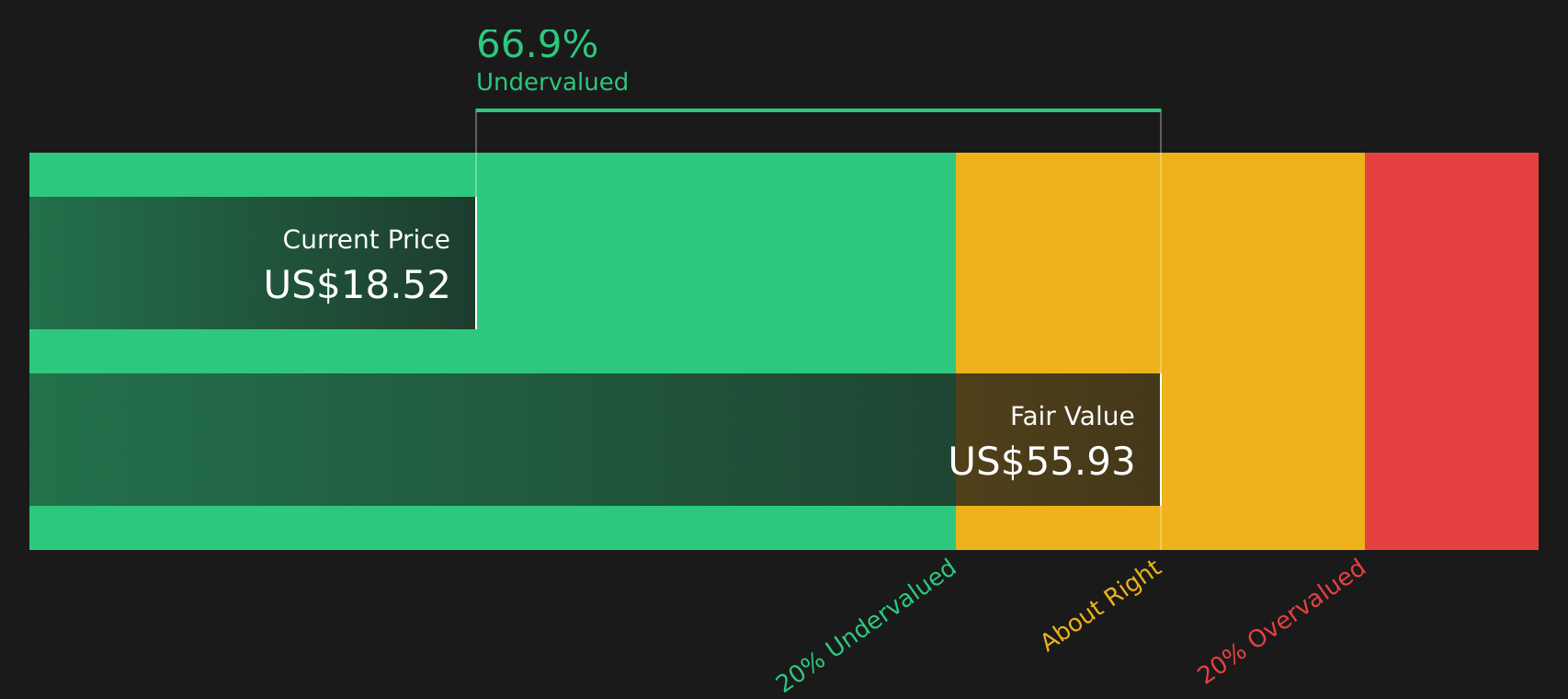

When these projected cash flows are discounted back using the DCF model, the resulting estimated intrinsic value is US$62.09 per share. Compared with the recent share price of US$17.23, this implies an intrinsic discount of about 72.2%, which indicates that the shares screen as materially undervalued on this model alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Opera is undervalued by 72.2%. Track this in your watchlist or portfolio, or discover 56 more high quality undervalued stocks.

Approach 2: Opera Price vs Earnings

For a profitable business like Opera, the P/E ratio is a straightforward way to relate what you pay for each share to the earnings that share currently generates. Investors often look for a P/E that reflects both what the company is earning today and what the market expects those earnings to look like over time, while also factoring in the risk of those earnings being volatile or disappointing.

Opera trades on a P/E of 14.26x. This sits below the Software industry average P/E of 30.50x and also below the peer group average of 31.51x. Simply Wall St’s Fair Ratio for Opera is 26.02x. This Fair Ratio is a proprietary estimate of what a reasonable P/E might be, given Opera’s earnings growth profile, profit margins, industry, market cap and risk characteristics.

Because the Fair Ratio folds in these company specific factors, it is a more tailored benchmark than a simple comparison with broad industry or peer averages. Lining up Opera’s current P/E of 14.26x against the Fair Ratio of 26.02x suggests the shares are trading below the level implied by those fundamentals on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Opera Narrative

Earlier the focus was on models and ratios, but Narratives give you a way to add your own story about Opera on top of the numbers. You can link a view on its products, risks and opportunities to specific forecasts for revenue, earnings and margins. These then roll up into a Fair Value that you can compare with the current share price to judge whether the stock looks attractive or stretched. All of this happens within Simply Wall St's Community page, where Narratives update automatically as new earnings or news arrive. One investor might build a cautious Opera Narrative that lines up with a Fair Value around the lower analyst end at US$23.00, while another might lean toward a more optimistic view closer to the upper analyst end at about US$33.00. Both can clearly see how their assumptions translate into different Fair Values and how that might influence their decisions on when to buy, sell or hold.

Do you think there's more to the story for Opera? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:OPRA

Opera

Provides mobile and PC web browsers and related products and services in Ireland, Singapore, the United States, and internationally.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1156.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.5% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9219.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19010.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Mastercard ·

Capital-light, high-return payment network that is successfully expanding into high-margin security and data services faster than its peers.

Fair Value:US$395.534.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JM

JM7 on Soluna Holdings ·

Soluna: Powering Renewable AI, Funding the Risk

Fair Value:US$985.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on RENOVA ·

Empowering the future with “new energy”

Fair Value:JP¥690.0941.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.8% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23038.1% overvalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative