Advertisement

- United States

- /

- Software

- /

- NasdaqCM:MITK

Mitek Systems (MITK): Revisiting Valuation After Mixed Earnings, Strong 2025 Guidance and Recent Share Price Rebound

Mitek Systems (MITK) just released fresh earnings and 2025 guidance, and the headline is a mixed picture: steady revenue growth with sharply higher full-year profit, but a weaker quarterly bottom line.

See our latest analysis for Mitek Systems.

The earnings update seems to have reminded investors of Mitek’s steady progress, with the 1 month share price return of 12.15% lifting the latest share price to $10.06, even as the 5 year total shareholder return remains deeply negative and longer term momentum is still rebuilding.

If this kind of rebound story has your attention, it could be a good moment to explore fast growing stocks with high insider ownership as another way to uncover potential growth ideas with aligned insiders.

With shares still trading at a steep discount to analyst targets despite modest growth and improving profitability, the key question now is whether Mitek is genuinely undervalued or whether markets are already pricing in its future gains.

Most Popular Narrative Narrative: 22.6% Undervalued

With the most followed narrative pointing to fair value above the current $10.06 share price, the spotlight shifts to the growth and profitability assumptions behind that gap.

Ongoing shift towards SaaS and recurring revenue models (now at 41% of trailing 12 month revenue and growing) is steadily improving predictability, while the company's focus on operational discipline and automation has driven service gross margin improvements of up to 200 basis points year over year, indicating enhanced long term net margin potential.

Curious how modest top line growth, rising margins and a richer future earnings multiple can still justify a higher price tag? The full narrative unpacks the revenue mix shift, embeds detailed margin trajectories and leans on a premium valuation multiple that may surprise you. Want to see exactly which profit and share count assumptions power that outlook and how they add up to today’s fair value call?

Result: Fair Value of $13 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent declines in check usage and intensifying competition in digital identity could erode revenue streams and challenge the optimistic valuation narrative.

Find out about the key risks to this Mitek Systems narrative.

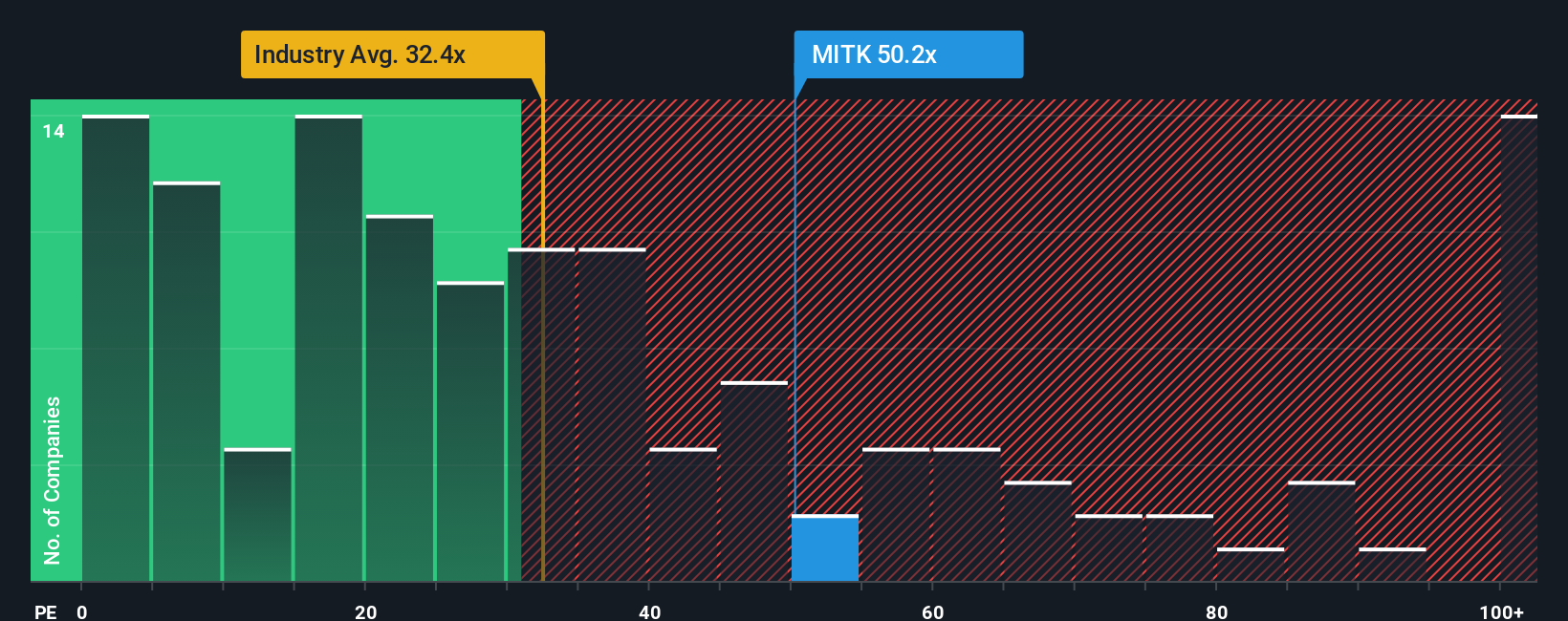

Another Lens on Valuation

While the narrative suggests Mitek is 22.6% undervalued, our ratio based view tells a different story. At a 52.3x price to earnings, the stock trades well above the US software sector on 32.9x and peers around 19.8x, and even above a 28.5x fair ratio that the market could drift toward, which would mean painful downside if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Mitek Systems Narrative

If your view differs or you prefer digging into the numbers yourself, you can build a complete narrative in just a few minutes: Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Mitek Systems.

Looking for more investment ideas?

Before you move on, lock in your next moves with targeted stock ideas from the Simply Wall Street Screener, so you are not chasing opportunities after they run.

- Capitalize on fast moving market inefficiencies by scanning these 908 undervalued stocks based on cash flows where solid fundamentals and attractive prices still align.

- Ride powerful innovation trends by zeroing in on these 26 AI penny stocks that harness automation, data, and machine learning to accelerate growth.

- Strengthen your income strategy by filtering for these 13 dividend stocks with yields > 3% that can potentially support returns even when markets turn choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:MITK

Mitek Systems

Provides digital identity verification and fraud prevention solutions worldwide.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.9% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$33.4722.6% overvalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative