Advertisement

- United States

- /

- Software

- /

- NasdaqGS:INTU

Intuit (INTU): Exploring Valuation After Recent Modest Share Price Gain

Intuit (INTU) shares moved slightly following a quiet news cycle, with the stock posting a 1% gain in the latest trading session. Investors continue to watch the company’s performance as broader trends in the tech sector remain in focus.

See our latest analysis for Intuit.

Intuit’s latest share price uptick comes after a modest pullback earlier this quarter. The stock continues to show solid momentum with an 8.57% year-to-date share price return and a nearly 10% total shareholder return over the past year, reinforcing longer-term confidence from investors.

Wondering what other innovative companies are gaining traction? Now could be the right moment to explore See the full list for free.

With Intuit’s shares outperforming much of the sector and the company delivering impressive growth in both revenue and net income, the question remains: is the stock still trading below its intrinsic value, or is the market already factoring in future gains?

Most Popular Narrative: 17.5% Undervalued

Intuit’s fair value, according to the most popular narrative, stands notably above the recent closing price. This suggests there may be untapped upside potential. How is this premium justified by growth and margin expectations? Consider the following:

The accelerating adoption of Intuit's AI-driven all-in-one platform, which includes virtual teams of AI agents and human experts, positions the company to consolidate customers' tech stacks, drive automation of workflows, and unlock substantial ROI for customers. This supports higher average revenue per customer (ARPC) and net margin expansion over time.

Want to know the growth blueprint driving this lofty valuation? The hidden ingredient: soaring long-term earnings, ambitious profit margins, and a projected future multiple typically reserved for industry giants. Curious which bold forecasts unlock that fair value? Dive in to see the numbers the analysts are betting on.

Result: Fair Value of $819.73 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent Mailchimp revenue softness and weaker international growth could undermine these optimistic projections. This may challenge Intuit’s continued momentum if trends do not improve.

Find out about the key risks to this Intuit narrative.

Another Perspective: Pricing Signals Mixed Caution

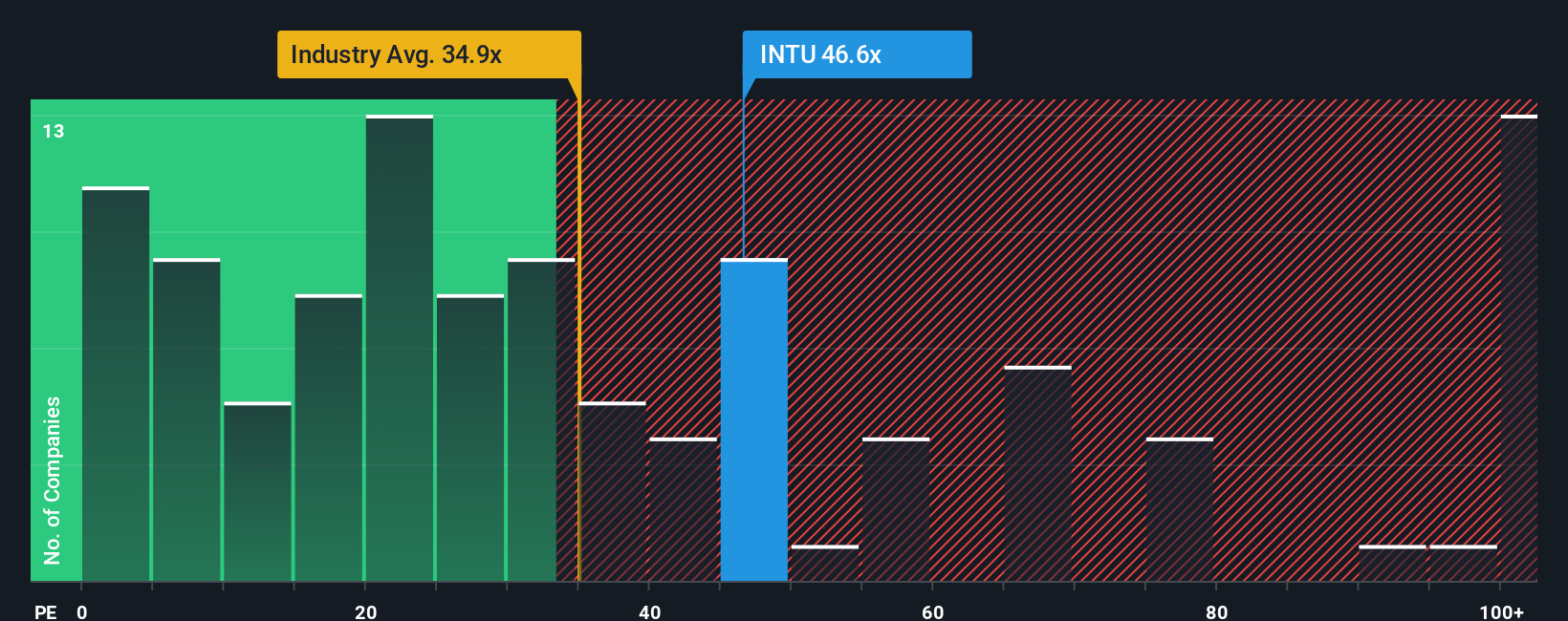

While the analyst consensus points to Intuit being undervalued, a closer look at its price-to-earnings ratio adds complexity. The ratio stands at 48.7 times, notably higher than both the software industry average (35.9x) and its own fair ratio benchmark (43.4x), even though it remains below the peer average (57.2x). This means investors are paying a premium for Intuit’s current growth. If expectations disappoint, the stock could face sharper pullbacks. Is the premium justified by future results, or does it leave little margin for error?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Intuit Narrative

If you see the story differently or want to reach your own conclusions, you can put together a personal view in just a few minutes with Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Intuit.

Looking for More Investment Ideas?

Don’t let great opportunities pass you by when there’s a world of exciting stocks just waiting to be uncovered. Try these targeted screens to find your next winner:

- Spot undervalued gems primed for long-term growth with these 842 undervalued stocks based on cash flows, helping you zero in on companies trading below their true worth.

- Capture strong income potential and reliable payouts by browsing these 18 dividend stocks with yields > 3%, which is ideal for those seeking dividend yields above 3%.

- Position yourself for the next technological leap by tapping into these 28 quantum computing stocks, featuring breakthrough firms shaping the future of computing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:INTU

Intuit

Provides financial management, payments and capital, compliance, and marketing products and services in the United States.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥1.91k9.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on International Business Machines ·

IBM has transitioned from a traditional IT services provider into a hybrid cloud and AI platform leader

Fair Value:US$256.0812.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RetiredbutWorking on USA Rare Earth ·

USAR Secures $19.3M Boost to Develop an Independent Rare Earth Supply Chain

Fair Value:US$0.336.7k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative