Intuit (INTU) shares dipped slightly this week, continuing a generally muted stretch for the software company. With performance over the past month barely budging, investors might be weighing long-term fundamentals against recent, smaller market moves.

Looking beyond the recent pause, Intuit’s stock has quietly delivered a steady 12% one-year total shareholder return, even as quarterly market momentum has briefly slowed. That blend of resilience and long-term growth potential helps explain why the company continues to hold investor interest, despite a muted few weeks.

With shares trading about 20% below analyst targets and solid double-digit growth still in the picture, the question remains: is Intuit a hidden bargain for patient investors, or is all that promise already priced in?

Advertisement

Most Popular Narrative: 17.1% Undervalued

With Intuit’s last close at $679.94 and the prevailing narrative pointing to a fair value near $820, anticipation is building around its future earnings power and profit margins. The valuation hinges on whether this anticipated growth can be realized within the next few years.

The accelerating adoption of Intuit's AI-driven all-in-one platform, including virtual teams of AI agents and human experts, positions the company to consolidate customers' tech stacks, drive automation of workflows, and unlock substantial ROI for customers. This supports higher average revenue per customer (ARPC) and net margin expansion over time. Intuit's rapid penetration into the fast-growing mid-market segment (serving customers with $2.5M to $100M in revenue and tapping into an $89B to $90B TAM), bolstered by quarterly product innovations and expanding partnerships with top accounting firms, sets up a durable multi-year revenue growth vector through new customer acquisition and cross-sell opportunities.

Curious what’s really fueling this ambitious price target? The most widely followed narrative is anchored on bold assumptions about Intuit’s future revenue, margin expansion, and dominance in emerging markets. Find out which critical forecasts, projections, and sector breakthroughs are moving the valuation needle to discover the surprising levers that could set Intuit apart from the software pack.

However, sluggish Mailchimp growth and international market hurdles could challenge Intuit’s impressive momentum. These factors serve as key risks to this bullish outlook.

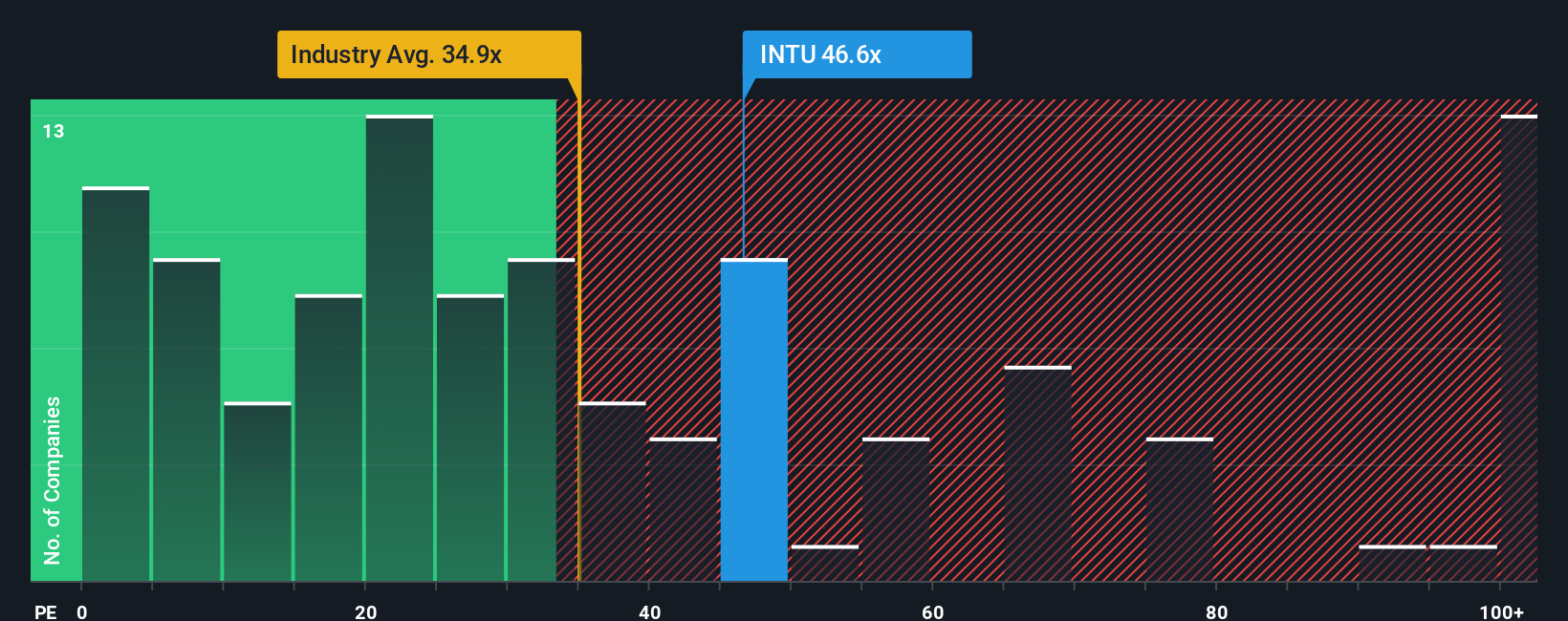

Looking at how Intuit’s price-to-earnings ratio compares, the company trades at 49x earnings, above the US Software industry average of 35.7x and its own fair ratio of 43.7x. This signals a premium price. Does this suggest risk of a valuation pullback, or is the market still optimistic?

If you see things differently or want to analyze Intuit's story your own way, you can dive into the numbers and craft a personal view in under three minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Intuit.

Looking for more investment ideas?

Serious about beating the market? You owe it to yourself to check out these exciting stock opportunities, each handpicked to help you grow and diversify your portfolio.

Target robust income streams by reviewing these 19 dividend stocks with yields > 3%. These consistently deliver yields above 3% for investors seeking steady returns.

Uncover tomorrow’s disruptors by evaluating these 24 AI penny stocks. These have explosive potential in artificial intelligence and automation-driven growth sectors.

Capitalize on value investment strategies when you assess these 893 undervalued stocks based on cash flows, pinpointing companies trading at attractive prices based on their future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies