Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

Lacklustre Performance Is Driving InterDigital, Inc.'s (NASDAQ:IDCC) Low P/E

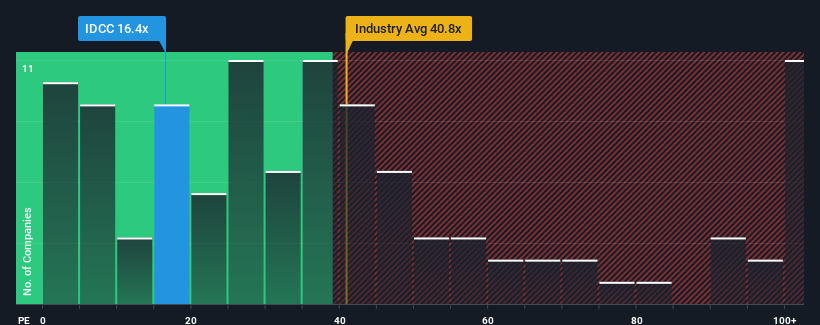

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may consider InterDigital, Inc. (NASDAQ:IDCC) as an attractive investment with its 16.4x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

InterDigital certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for InterDigital

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as InterDigital's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 40% gain to the company's bottom line. Pleasingly, EPS has also lifted 903% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 13% per year as estimated by the five analysts watching the company. Meanwhile, the broader market is forecast to expand by 11% per year, which paints a poor picture.

With this information, we are not surprised that InterDigital is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that InterDigital maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for InterDigital that you should be aware of.

You might be able to find a better investment than InterDigital. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8228.9% undervalued

39 followersusers have followed this narrative

4 commentsusers have commented on this narrative

28 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6435.3% undervalued

30 followersusers have followed this narrative

4 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Hitit Bilgisayar Hizmetleri ·

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

Fair Value:₺61.1531.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22090.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

WealthAP on Alibaba Group Holding ·

BABA Analysis: Buying the Fear, Holding the Cloud

Fair Value:US$187.0417.4% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

70 followersusers have followed this narrative

13 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.9% undervalued

1027 followersusers have followed this narrative

6 commentsusers have commented on this narrative

29 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25411.3% overvalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative