Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

InterDigital (IDCC) Stock Could Be 36% Undervalued After Amazon License Agreement

Why InterDigital’s New Amazon Agreement Matters for Shareholders

InterDigital (IDCC) has drawn fresh investor attention after announcing a patent license agreement with Amazon that covers key services and devices, alongside plans to resolve all pending litigation through binding arbitration.

This development sits alongside a recently declared regular quarterly dividend and shareholder approval of bylaw changes related to officer exculpation. Together, these provide investors with several governance, income, and licensing factors to weigh when assessing the stock.

See our latest analysis for InterDigital.

InterDigital’s recent Amazon agreement and bylaw update come against a mixed backdrop, with a 13.43% 1 month share price return and the share price still down 9.26% year to date. At the same time, the 5 year total shareholder return of 330.09% highlights substantial longer term gains.

If this kind of licensing news has you thinking about where else growth stories could emerge, it may be worth scanning the market using the 49 AI infrastructure stocks

With InterDigital’s share price up 13.43% over the past month but still down 9.26% year to date, and trading well below the average analyst price target, investors have to ask: is there real value left here or is the market already pricing in future growth?

Most Popular Narrative: 36% Undervalued

InterDigital’s most followed narrative pegs fair value at $462.67 per share versus a last close of $296.04. This frames the current price as a sizable discount built on detailed cash flow and earnings assumptions.

The recent 67% uplift in the Samsung license and an all-time high annualized recurring revenue, driven by multi-year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals, potentially inflating valuation multiples and overstating sustainable revenue trajectory.

Curious what justifies that valuation gap for InterDigital? The narrative leans heavily on recurring licensing income, margin resilience and a richer future earnings multiple than many software peers.

Result: Fair Value of $462.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still have to weigh the risk that InterDigital’s heavy reliance on smartphone royalties and ongoing regulatory scrutiny of patent licensing could weaken those long term cash flow assumptions.

Find out about the key risks to this InterDigital narrative.

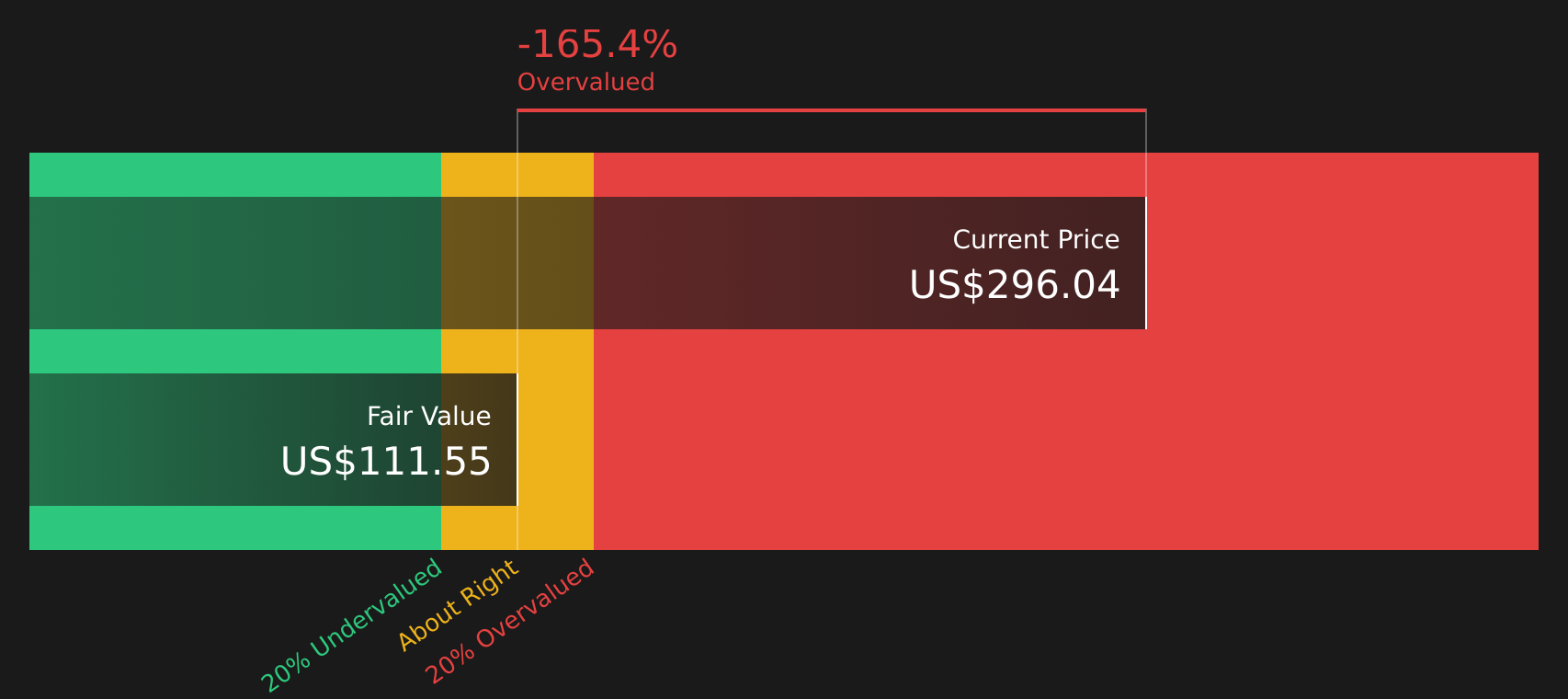

Another View: InterDigital Through a Cash Flow Lens

While the analyst narrative suggests InterDigital is 36% undervalued with a fair value of $462.67 per share, the Simply Wall St DCF model points the other way, with an estimate of $111.55 per share versus today’s $296.04 price. This implies the stock screens as overvalued on that basis. Which lens do you trust more for your own thesis?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of optimism and caution around InterDigital leaves you undecided, act while the data is fresh and form your own view by reviewing the 3 key rewards

Looking For More Investment Ideas Beyond InterDigital?

If InterDigital has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to surface other opportunities that fit your style.

- Target resilient cash generators by scanning companies in the 45 high quality undervalued stocks and see where market expectations look out of line with fundamentals.

- Prioritize stability by reviewing the 65 resilient stocks with low risk scores to find stocks that pair lower risk scores with more predictable business profiles.

- Hunt for tomorrow’s potential standouts with the screener containing 19 high quality undiscovered gems and spot quality ideas before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.524.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.719.3% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

PE

peter_4mgsy on Rhythm Pharmaceuticals ·

High-Growth Emerging Commercial Stage Biotech

Fair Value:US$13413.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on FreightCar America ·

ALL ABOARD THE VALUE TRAIN: WHY $RAIL MIGHT BE HEADED NORTH - FREIGHTCAR AMERICA - Long term price target of $25

Fair Value:US$2568.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Rigaku Holdings ·

Capitalizing on rising semiconductor complexity

Fair Value:JP¥2.52k22.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

288 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

153 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

173 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

R2

R2R on Fonterra Shareholders Fund ·

SIMPLY WALL STREET please delete this Ai slop nonsense article.

0

|0