Advertisement

- United States

- /

- Software

- /

- NasdaqGS:FTNT

Should Fortinet’s Index Exit and Partner Expansion Shift How Investors View FTNT’s Risk‑Return Profile?

Reviewed by Sasha Jovanovic

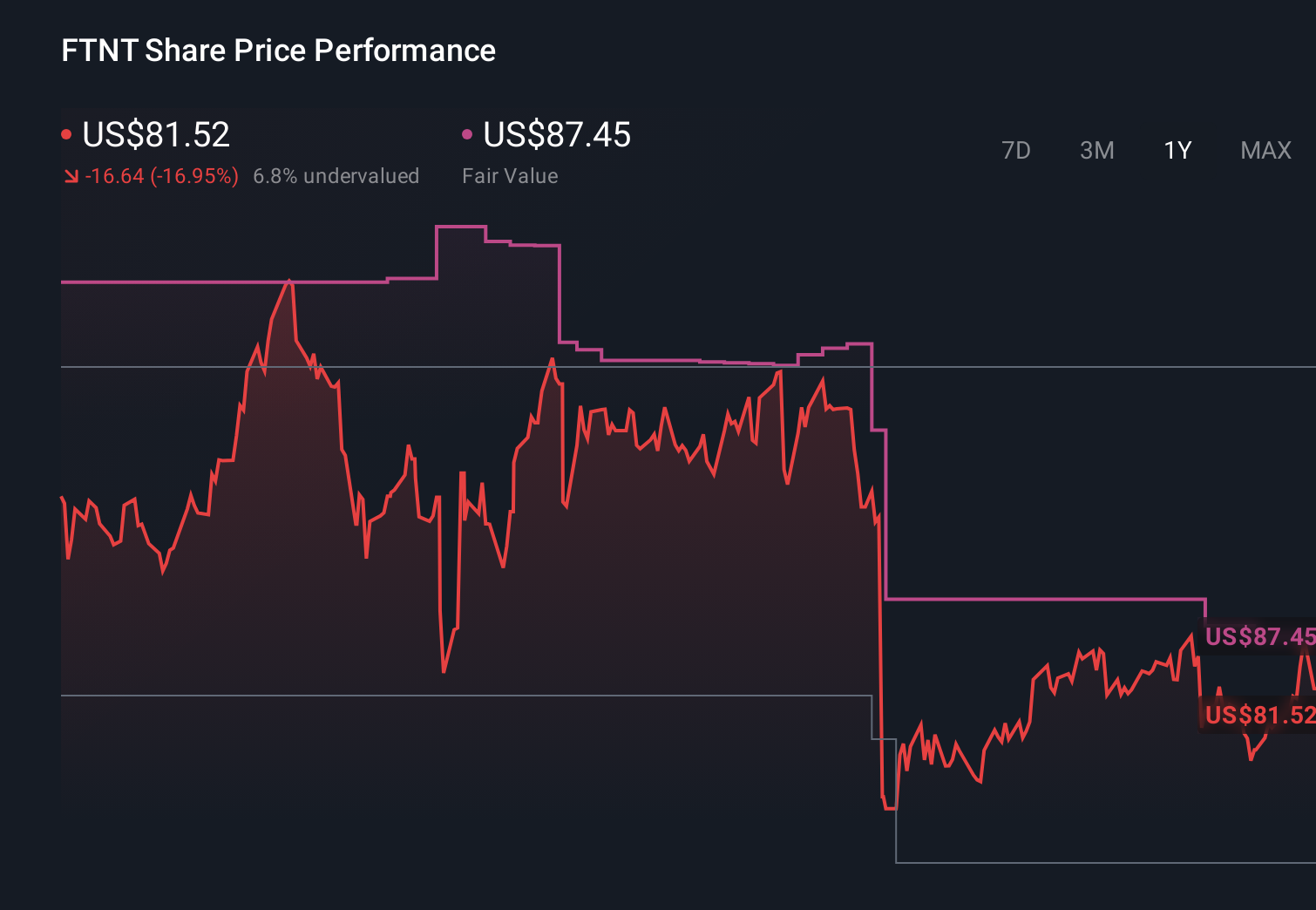

- In late June 2026, Fortinet, Inc. was removed from both the Russell 1000 Defensive Index and the Russell 1000 Growth-Defensive Index, reflecting a shift in how the stock is categorized by index providers.

- At the same time, Fortinet’s ecosystem momentum remained evident, with partner Liquid Networx expanding access to Fortinet licensing and professional services through major cloud marketplaces while the company continued to highlight strong demand for its cybersecurity platform.

- We’ll now examine how Fortinet’s index removal and ongoing demand signals influence its existing investment narrative and risk-return profile.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Fortinet Investment Narrative Recap

To own Fortinet, you need to believe its integrated security platform, growing software and services mix, and large enterprise relationships can offset pressures on hardware-driven cycles and margins. The recent removal from Russell defensive indexes may cause some technical selling but does not appear to alter the key near term catalyst around execution on SASE, AI security, and large enterprise deals, nor the main risk of post refresh product growth deceleration and ongoing investment driven margin pressure.

The most relevant recent development is Liquid Networx bringing Fortinet licensing and services to AWS and Azure Marketplaces, which reinforces the SASE and cloud platform adoption story that many see as Fortinet’s main growth lever. This aligns with analyst expectations that higher margin, recurring cloud and security services can gradually lessen reliance on appliance refresh cycles and help buffer the business against slower hardware demand or elongated sales cycles.

Yet, despite these positives, investors should be aware that Fortinet’s heavy infrastructure and sales investments could weigh on margins if...

Read the full narrative on Fortinet (it's free!)

Fortinet's narrative projects $9.2 billion revenue and $2.5 billion earnings by 2029. This requires 10.6% yearly revenue growth and an earnings increase of about $0.6 billion from $1.9 billion today.

Uncover how Fortinet's forecasts yield a $89.00 fair value, a 43% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were penciling in about US$10.6 billion in 2029 revenue and US$3.2 billion in earnings, yet the latest index removal and hardware dependence risk show how differently you and those analysts might weigh Fortinet’s upside and potential pressure on growth and margins over time.

Explore 16 other fair value estimates on Fortinet - why the stock might be worth as much as $120.34!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Fortinet research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Fortinet research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fortinet's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 42 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FTNT

Fortinet

Provides cybersecurity and convergence of networking and security solutions worldwide.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.6% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9956.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative