Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

Amdocs (NASDAQ:DOX) Has More To Do To Multiply In Value Going Forward

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. That's why when we briefly looked at Amdocs' (NASDAQ:DOX) ROCE trend, we were pretty happy with what we saw.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Amdocs:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

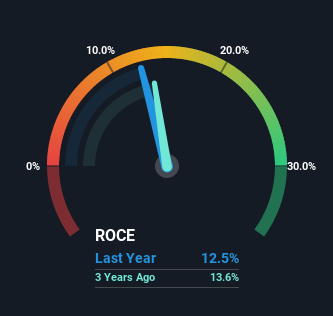

0.13 = US$647m ÷ (US$6.5b - US$1.3b) (Based on the trailing twelve months to June 2022).

Therefore, Amdocs has an ROCE of 13%. In absolute terms, that's a pretty normal return, and it's somewhat close to the IT industry average of 12%.

Our analysis indicates that DOX is potentially undervalued!

In the above chart we have measured Amdocs' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Amdocs here for free.

What Does the ROCE Trend For Amdocs Tell Us?

While the returns on capital are good, they haven't moved much. Over the past five years, ROCE has remained relatively flat at around 13% and the business has deployed 26% more capital into its operations. Since 13% is a moderate ROCE though, it's good to see a business can continue to reinvest at these decent rates of return. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

In Conclusion...

The main thing to remember is that Amdocs has proven its ability to continually reinvest at respectable rates of return. In light of this, the stock has only gained 33% over the last five years for shareholders who have owned the stock in this period. That's why it could be worth your time looking into this stock further to discover if it has more traits of a multi-bagger.

Amdocs could be trading at an attractive price in other respects, so you might find our free intrinsic value estimation on our platform quite valuable.

While Amdocs may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on Myseum ·

The Future of Social Sharing Is Private and People Are Ready

Fair Value:US$7.9577.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on ASML Holding ·

EU#3 - From Philips Management Buyout to Europe’s Biggest Company

Fair Value:€1.31k6.4% undervalued

30 followersusers have followed this narrative

4 commentsusers have commented on this narrative

11 likesusers have liked this narrative

YI

yiannisz on Booking Holdings ·

Booking Holdings: Why Ground-Level Travel Trends Still Favor the Platform Giants

Fair Value:US$5.47k8.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CO

composite32 on Shell ·

A fully integrated LNG business seems to be ignored by the market.

Fair Value:UK£36.123.0% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

TI

TibiT on On the Beach Group ·

Sunny Returns with On the Beach

Fair Value:UK£3.0326.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EM

emndy on Presco ·

High Quality Business and a true compounding machine

Fair Value:₦2.2k25.7% undervalued

10 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CL

Clive_Thompson on Roche Holding ·

Roche Holding AG To Benefit From Strong Drug Pipeline In 2027 And Beyond

Fair Value:CHF 430.0117.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.4% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0224.5% undervalued

1048 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Amazon.com ·

AMZN: Acceleration In Cloud And AI Will Drive Margin Expansion Ahead

Fair Value:US$295.6119.1% undervalued

1344 followersusers have followed this narrative

5 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

RO

RockeTeller on Argenta Silver ·

AGAG still in exploration, in bull market, such company will be the last to participate. It's high risk but can results in 20-30 baggers potential. The best play with current bull are with producers or near-producer miners, you can get 5-10 baggers with much lower risk. See my analysis on santacruz silver, andean silver.

0

|0

US

User on Life Insurance Corporation of India ·

Stock falling daily since promoter (Govt of India) holds maximum... selling

0

|0