Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DDOG

Datadog (DDOG) Valuation Reassessed After Analyst Downgrades And Rotation Out Of Technology Stocks

Recent analyst downgrades and a rotation out of technology stocks have put Datadog (DDOG) back under the microscope as investors weigh valuation concerns against its strong earnings beat and ongoing positive business outlook.

See our latest analysis for Datadog.

That pullback has been sharp, with a 1 day share price return of a 4.0% decline, a 30 day share price return of a 14.1% decline and a year to date share price return of a 6.2% decline. Even so, the 3 year total shareholder return of 78.1% still points to strong longer term gains. Recent momentum appears to be fading as investors reassess growth expectations and risk around competition and AI budgets.

If Datadog’s swings have you thinking about where else AI spending might flow, this could be a good moment to check out high growth tech and AI stocks as potential next ideas.

So with Datadog now at US$125.49, strong recent results and a roughly 49.6% intrinsic discount signal one story, while fresh Sell ratings and AI competition suggest another. Is this a reset worth considering, or is future growth already priced in?

Most Popular Narrative: 39.8% Undervalued

With Datadog last closing at US$125.49 versus a most followed fair value estimate of about US$208.49, the valuation story hinges on how much earnings power and AI driven demand you think can be sustained over time.

Ongoing product innovation (e.g., autonomous AI agents, enhanced security modules, expanded log and data observability) is increasing platform breadth and relevance, providing cross-selling opportunities and driving higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins. Datadog's focus on internal cloud cost optimization, platform efficiency, and leveraging its own solutions for cost savings is already contributing to higher gross margins, and further improvements are expected to flow through to operating income and net earnings as volume scales.

Curious what kind of revenue trajectory and margin profile need to materialise to back that fair value, plus what future P/E is being baked in? The full narrative lays out a detailed path involving rapid earnings expansion, shifting profitability and a rich earnings multiple that goes well beyond typical software names.

Result: Fair Value of $208.49 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including potential pricing compression from rivals and heavier spending that could squeeze margins if revenue growth does not keep pace.

Find out about the key risks to this Datadog narrative.

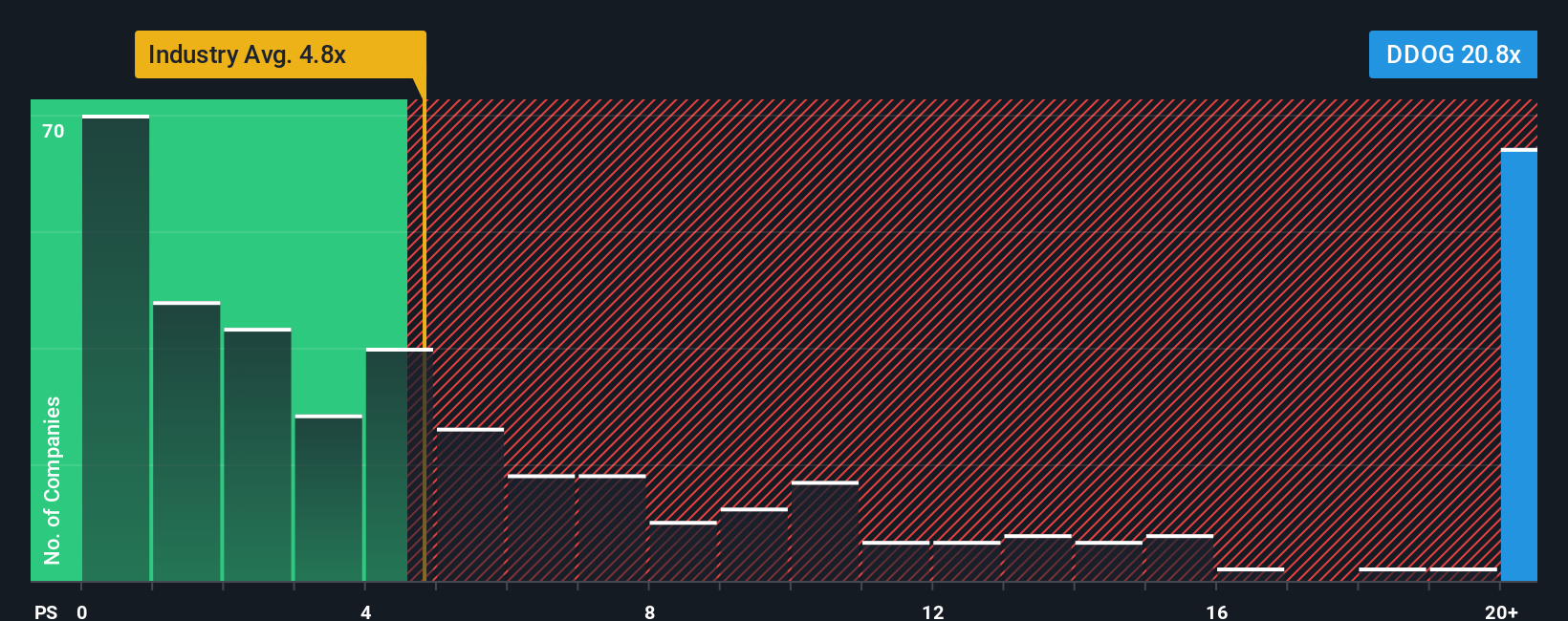

Another View: Rich Sales Multiple Keeps Expectations High

While our fair value estimate suggests Datadog trades at a roughly 49.6% discount, its P/S ratio of 13.7x tells a different story. That is well above the US Software industry at 4.9x, the peer average at 9.7x, and even the 12.5x fair ratio our model suggests the market could move toward. For you, that gap can either look like a valuation cushion or a sign that expectations still sit high, especially if growth or margins come in softer than hoped.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Datadog Narrative

If you see the numbers differently, or simply want to stress test your own assumptions against the data, you can quickly build a custom thesis that reflects your view, then Do it your way.

A great starting point for your Datadog research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

Do not stop your research with a single stock, broaden your watchlist using focused screeners that surface opportunities you might otherwise miss.

- Target reliable cash generators by scanning for companies in these 12 dividend stocks with yields > 3% that may add income strength to your portfolio.

- Chase future facing themes by reviewing these 79 cryptocurrency and blockchain stocks that are building real businesses around blockchain and digital assets.

- Hunt for potential mispricings by checking these 885 undervalued stocks based on cash flows that currently trade at a discount to their cash flow profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DDOG

Datadog

Operates an observability and security platform for cloud applications in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

98 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9820.4% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

22 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1558.0% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3648.3% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.162.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FI

Finder109 on BARK ·

Buy-out proposal for BARK Inc., at $1.10 has be confirmed by the acquisition group

Fair Value:US$1.443.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DH

Dhruva on Paladin Energy ·

Paladin Energy: Betting on the Nuclear Renaissance

Fair Value:AU$1.87563.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.9% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.9% undervalued

1306 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.0% undervalued

1103 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative