Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Is Dropbox (DBX) Undervalued On Russell Index Rebalancing?

Why Dropbox Is Shifting Between Growth and Defensive Indexes

Recent Russell index rebalancing moved Dropbox (DBX) out of several growth benchmarks and into the Russell 1000 Defensive and Value Defensive indexes, a shift that can influence fund-driven trading flows.

For you as an investor, these changes are less about company headlines and more about how rules based funds that track Russell indexes may adjust their Dropbox exposure. Those reallocations can affect liquidity and short term price behavior without changing the underlying business.

This index reshuffle comes as Dropbox continues to run a subscription based cloud storage and collaboration platform with around 18 million paying users and a sizeable presence across both United States and international markets.

See our latest analysis for Dropbox.

Against this index reshuffle backdrop, Dropbox’s share price has moved to US$28.56, with a 7.21% 7 day share price return and a 22.05% 90 day share price return pointing to building short term momentum. The 2.00% 1 year total shareholder return and 5.90% 3 year total shareholder return sit alongside a 5 year total shareholder return that is down 8.02%.

If the recent shift toward defensive indexes has you thinking about where else growth or resilience might show up next, it could be worth scanning 62 profitable AI stocks that aren't just burning cash

With Dropbox now sitting in defensive indexes, trading above its average analyst target and carrying an estimated 34% intrinsic discount, the key question is whether the current price still offers upside or already reflects future growth.

Most Popular Narrative: 9% Overvalued

The most followed Dropbox narrative points to a fair value of $26.17, slightly below the last close at $28.56, which frames the current valuation debate.

The planned expansion and deeper integration of AI-driven productivity tools (Dash), including upcoming self-serve offerings and seamless bundling with Dropbox's existing file sync-and-share product, position the company to capture higher ARPU and accelerate recurring revenue growth as digital transformation and hybrid work drive demand for intelligent, collaborative cloud platforms.

Ongoing investments in onboarding improvements, streamlined product experiences, and personalized retention (e.g., cancellation flow redesign, Simple plan targeting mobile-first consumers) are already reducing churn and increasing user engagement, setting the stage for greater user retention and potential user base growth, positively impacting revenue stability and reducing customer acquisition costs.

Curious how a flat revenue path, steady margins, and shrinking share count still add up to that fair value? The core of this narrative rests on consistent profitability, disciplined discount rate assumptions, and a future earnings multiple that sits below many peers but above today. Want to see which precise earnings and valuation inputs are doing the heavy lifting in that model? The full narrative lays those numbers out line by line.

Result: Fair Value of $26.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, investors still need to weigh Dropbox’s recent revenue decline and ARPU pressure, as well as tougher competition from larger suites that could challenge user retention.

Find out about the key risks to this Dropbox narrative.

Another View: How Dropbox Looks On Earnings Multiples

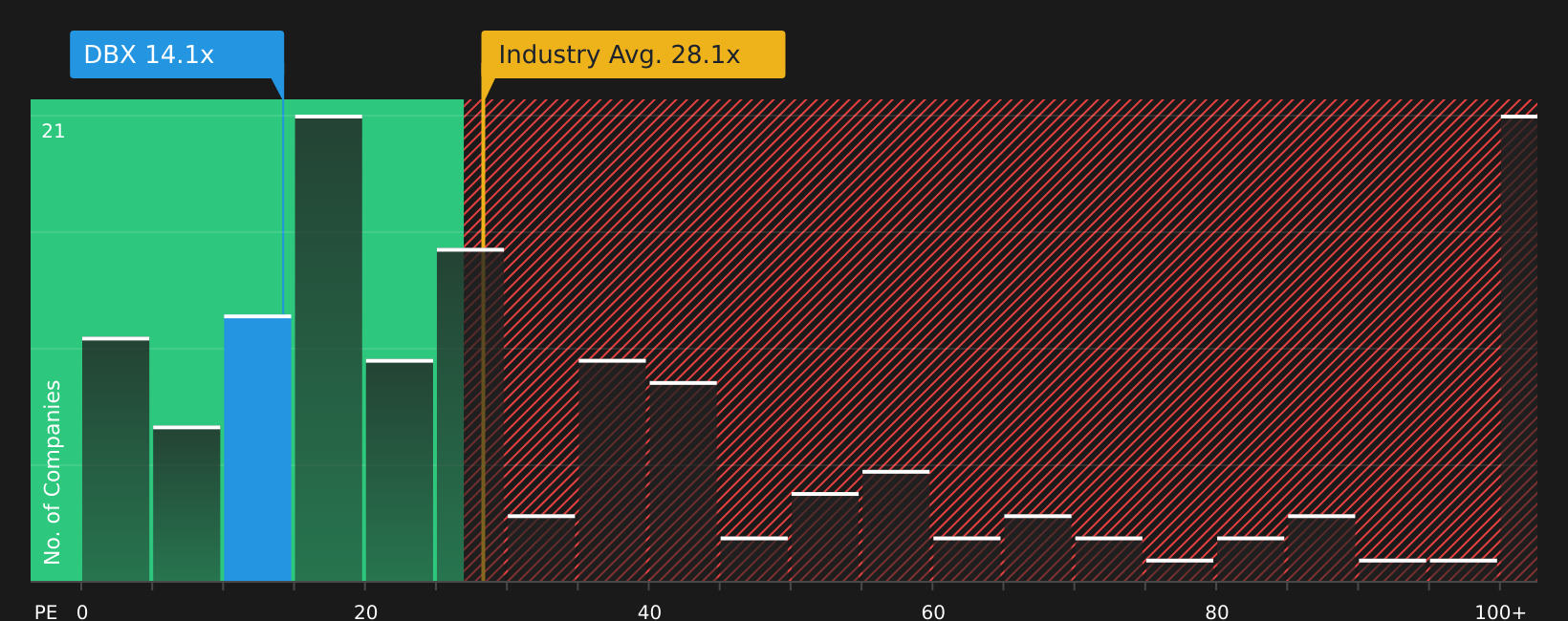

While the most followed Dropbox narrative sees the stock as about 9% overvalued versus a fair value of $26.17, the earnings multiple tells a different story. At a P/E of 14.1x, Dropbox trades below both peers at 18.5x and the wider US Software industry at 28x, and also below a fair ratio of 20.1x that the market could move towards. This points to a valuation gap you need to decide is risk or opportunity.

To see how this earnings based view stacks up against the detailed assumptions in the valuation work, take a closer look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals around Dropbox’s valuation and business momentum, do you want to rely on others’ sentiment or test it yourself against the numbers? Take a closer look at both sides of the story by weighing the 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Dropbox?

If you only stop at Dropbox, you risk overlooking other stocks that might fit your goals even better, so consider putting a few curated shortlists to work.

- Target dependable cash generators by reviewing the 43 high quality undervalued stocks, which combine earnings strength with potentially appealing prices.

- Strengthen your income stream by scanning the 7 dividend fortresses, offering higher yields with a focus on resilience.

- Dial down portfolio risk by focusing on the 75 resilient stocks with low risk scores, which score well on stability and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.1% undervalued

70 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

IN

inimosini on Lucky Cement ·

Discounted Cash Flow Valuation of Lucky Cement Limited (LUCK)

Fair Value:PK₨511.86.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative