Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Is Dropbox (DBX) Now Attractively Priced After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- Wondering whether Dropbox is a bargain or just fairly priced at its current level? This article walks through what the numbers are saying about the stock's value.

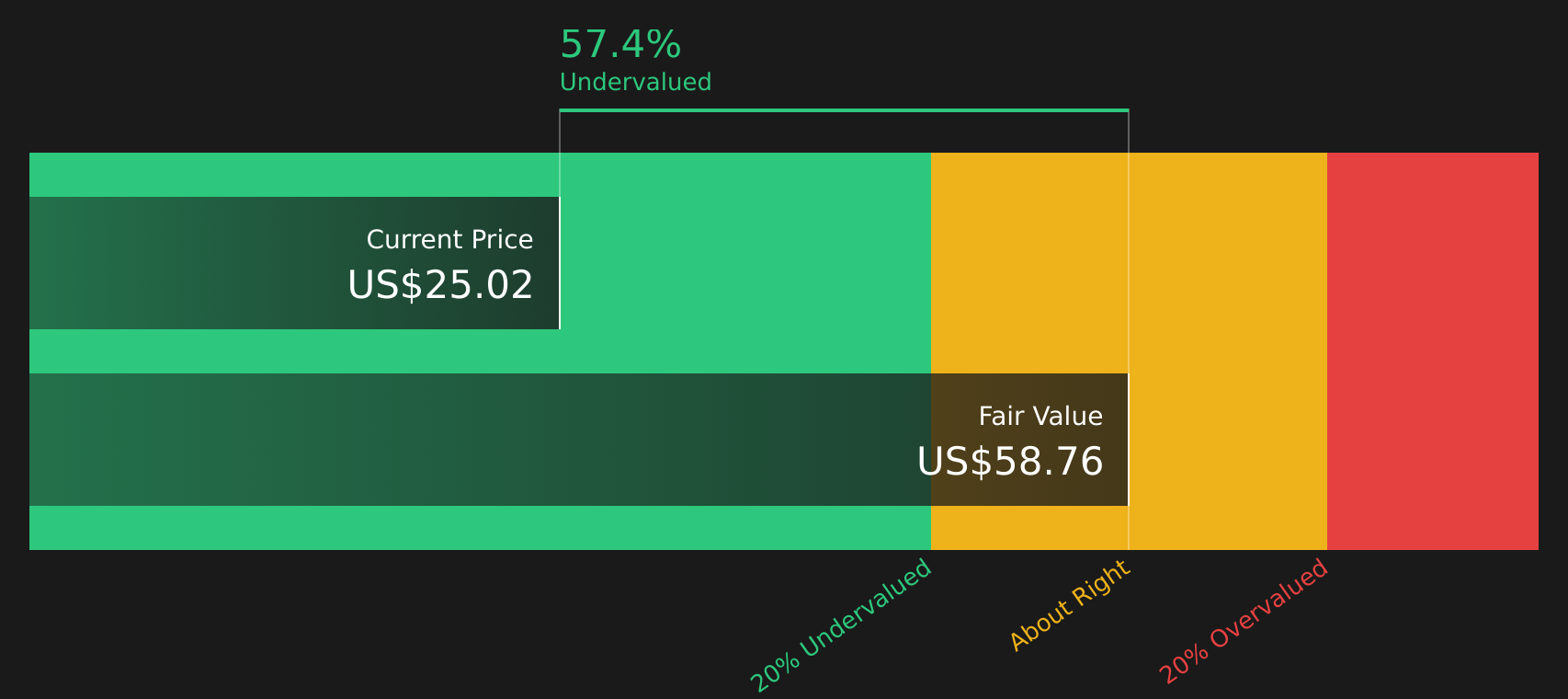

- Dropbox shares last closed at US$24.43, with returns of a 1.2% decline over 7 days, 7.9% decline over 30 days, 9.3% decline year to date, 5.9% decline over 1 year, 18.2% over 3 years and 6.0% over 5 years, which may have some investors reassessing the balance between opportunity and risk.

- Recent coverage around Dropbox has focused on its position as a mature cloud storage and collaboration platform and how investors weigh that against other software names. This helps frame the recent share price performance. Alongside that, ongoing discussion about competition in cloud services and productivity tools has kept attention on how much value the market is currently willing to assign to Dropbox.

- On our framework, Dropbox scores a 5 out of 6 valuation score. This indicates it screens as undervalued on most of our checks. Next we will walk through the main valuation approaches we use, before finishing with a different way to look at value that can put all of these methods in context.

Approach 1: Dropbox Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF model, looks at the cash Dropbox is expected to generate in the future and discounts those projections back to today, to estimate what the entire business could be worth right now.

For Dropbox, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about US$928.9 million. Analyst estimates and Simply Wall St extrapolations project free cash flow of roughly US$931.0 million in 2026 and US$1,296.6 million in 2035, with values between those years laid out in the ten year projection set.

When all those future cash flows are discounted back to today, the model arrives at an estimated intrinsic value of US$59.33 per share. Compared with the recent share price of US$24.43, the DCF output suggests the stock trades at a 58.8% discount, which points to Dropbox looking undervalued on this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 58.8%. Track this in your watchlist or portfolio, or discover 53 more high quality undervalued stocks.

Approach 2: Dropbox Price vs Earnings (P/E)

For a profitable business like Dropbox, the P/E ratio is a useful shortcut because it links what you pay today directly to the earnings the company is already generating. In general, higher growth expectations and lower perceived risk tend to justify a higher P/E, while slower growth or higher risk usually point to a lower, more cautious multiple.

Dropbox currently trades on a P/E of 11.59x. That sits well below the Software industry average of 25.78x and also below the peer group average of 22.86x. To sharpen this comparison, Simply Wall St uses a proprietary “Fair Ratio” of 20.38x, which is the P/E level the model suggests for Dropbox given factors such as its earnings profile, industry, profit margins, market cap and company specific risks.

This Fair Ratio is more tailored than a simple industry or peer comparison because it adjusts for Dropbox’s own characteristics instead of assuming it should trade exactly like the average software name. Setting the Fair Ratio of 20.38x against the actual 11.59x P/E implies the shares are pricing in a lower multiple than the model suggests might be appropriate.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 21 top founder-led companies.

Upgrade Your Decision Making: Choose your Dropbox Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St you can use Narratives on the Community page to attach your own story about Dropbox to a set of revenue, earnings and margin assumptions, link that story to a fair value, then compare it with the current price to help decide whether you see Dropbox as closer to the higher US$30 or lower US$20 fair value cases. The Narrative automatically updates as new news or earnings arrive so your view stays connected to the latest information rather than a static spreadsheet.

For Dropbox, here are previews of two leading Dropbox narratives:

Fair value in this bullish narrative: US$30.00 per share

Implied discount to this fair value: 18.6% below the narrative fair value at the recent US$24.43 share price

Revenue trend used in this narrative: 29.8% annual decline

- Assumes Dropbox successfully leans into AI led products like Dash and workflow tools for enterprises, supporting higher margins and long term cash generation.

- Builds in an expectation that share buybacks reduce the share count meaningfully, which supports earnings per share even with a soft revenue trend.

- Identifies long term potential if management can keep investing in AI tools while holding on to profitability, with churn, competition and a shrinking paid user base as key risks.

Fair value in this bearish narrative: US$20.00 per share

Implied premium to this fair value: 22.2% above the narrative fair value at the recent US$24.43 share price

Revenue trend used in this narrative: 157.2% annual decline

- Assumes elevated churn in Teams customers, reduced investment in non core lines and headwinds in outbound sales that keep pressure on revenue and earnings.

- Treats the shift from mature file storage into AI tools like Dash as a source of execution uncertainty, with slower contribution from new products and sensitivity to currency moves.

- Views the current price as demanding, based on a fair value anchor of US$20.00 that already factors in profitability, buybacks and some benefit from AI, while still highlighting competition and growth risk.

These two narratives bracket the recent share price by using different assumptions about revenue trends, margins and how much credit Dropbox earns for its AI initiatives and capital returns. The useful next step is to decide which set of assumptions feels closer to how you see the business, or to shape your own view somewhere between the two.

Curious how numbers become stories that shape markets? Explore Community Narratives

Do you think there's more to the story for Dropbox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on Evolution ·

A Monopoly-Quality Business Trading at Distress Multiples — CEO Buying, €346M Buyback Active, 73% Upside to Fair Value

Fair Value:SEK 1.04k33.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IM

Imthetxarbi on SThree ·

Every Staffing Stock Is Being Sold. SThree Is the Only One That Benefits From the Thing Killing the Others

Fair Value:UK£4.966.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

basicFit26 on Vusion ·

Vusion's Profit Margin to Grow by 9.74% Promises Bright Future

Fair Value:€229.1937.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

3 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative