Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CRWD

Does CrowdStrike’s Impressive 81.5% Gain Reflect Its True Value After Recent Cybersecurity News?

Reviewed by Bailey Pemberton

- Curious whether CrowdStrike Holdings is still a good deal after such impressive gains? You're not alone. Let's dive into what really matters for valuation-focused investors.

- The stock has climbed 3.2% in the last week, 9.8% over the past month, and boasts an 81.5% gain in the past year, with returns of 280.6% over three years and 287.8% in five.

- Recent headlines highlight CrowdStrike's continued leadership in cybersecurity innovation and strategic partnerships, fueling optimism around future growth and competitive strength. Industry buzz has intensified as enterprises seek robust cloud security solutions, adding momentum to the company's share price.

- When it comes to traditional valuation checks, CrowdStrike scores 0 out of 6 for being undervalued. Yet, as we'll see, there's more to valuation than these simple signals, and a better approach might make all the difference by the end of this article.

CrowdStrike Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: CrowdStrike Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today's value. Essentially, this approach looks at how much cash the business will generate each year, determines what that is worth in today's dollars, and adds up the total to arrive at a fair estimate of value.

CrowdStrike Holdings currently delivers Free Cash Flow of $1.04 Billion, with analysts projecting significant growth over the next decade. By 2030, estimates call for Free Cash Flow to reach approximately $4.58 Billion, based on both analyst forecasts for the next five years and longer-term extrapolations. This strong growth trend highlights the company's scalability and market momentum in cybersecurity.

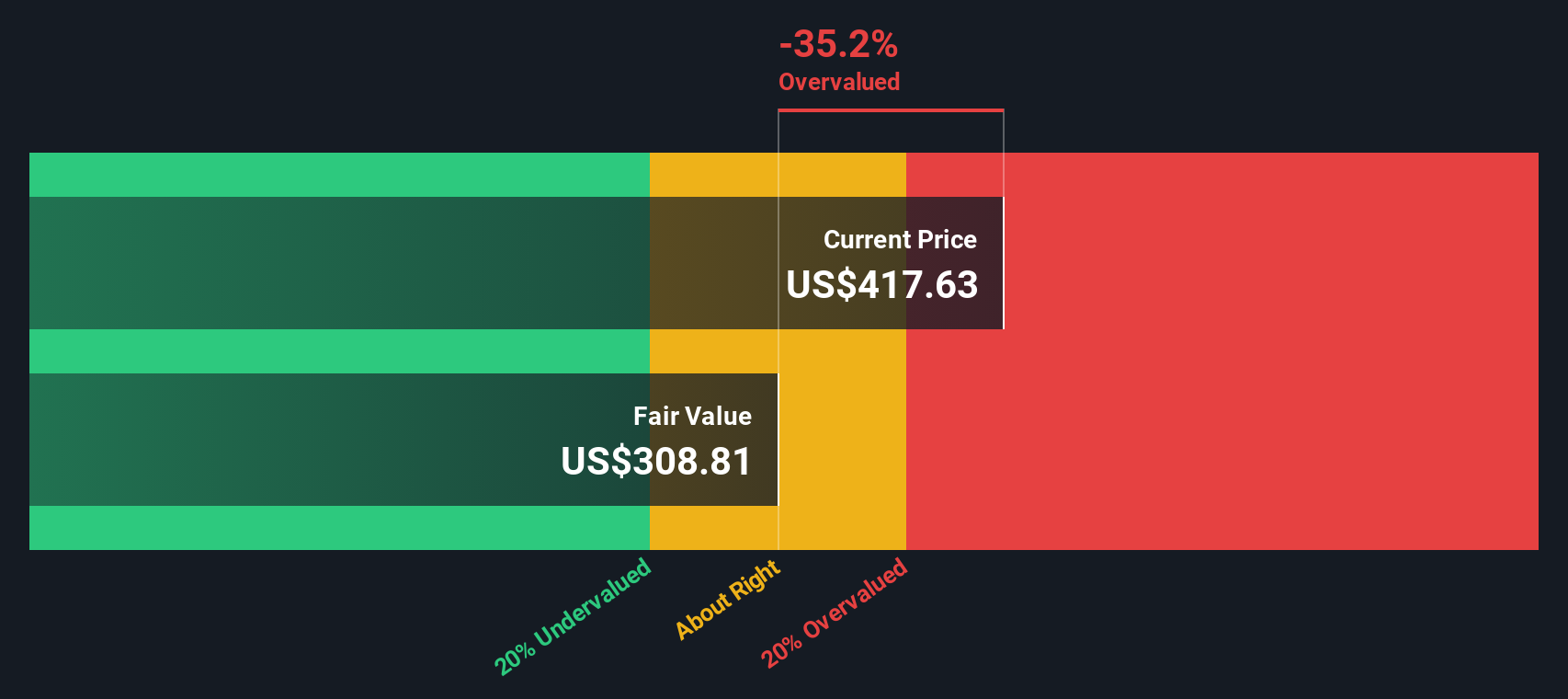

Based on these projections, the DCF model calculates an intrinsic value of $411.57 per share for CrowdStrike. When compared to the current share price, this implies the stock is about 30.9% overvalued at present. In other words, the market has already priced in much of the anticipated growth, and the shares are trading well above what the company’s present and projected cash flows might justify.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CrowdStrike Holdings may be overvalued by 30.9%. Discover 848 undervalued stocks or create your own screener to find better value opportunities.

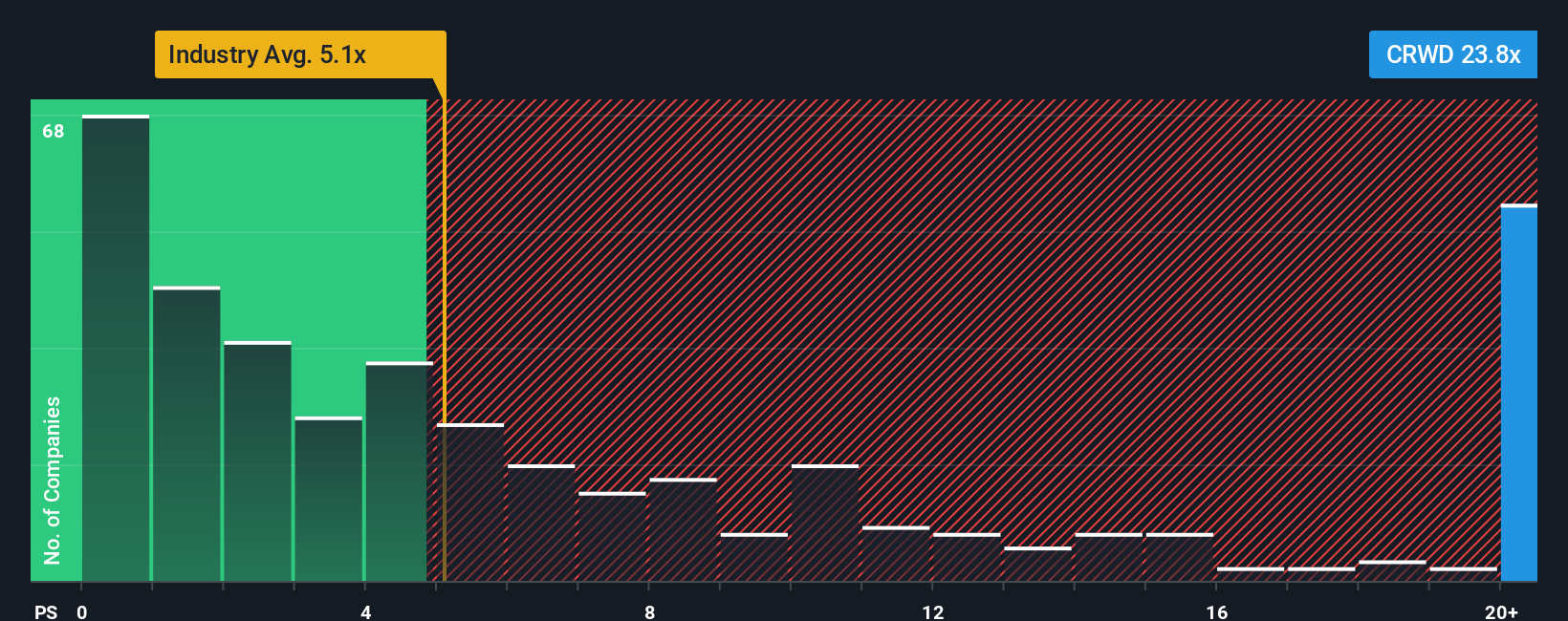

Approach 2: CrowdStrike Holdings Price vs Sales (P/S) Multiple

The Price-to-Sales (P/S) multiple is often a strong valuation tool for rapidly growing, profitable software firms like CrowdStrike. P/S is especially meaningful in cases where earnings can be volatile due to ongoing investments in growth, but strong recurring revenues signal fundamental business strength.

A company's fair P/S multiple is shaped by its expected revenue growth, profit margins, and overall market risks. Higher-growth and market-leading software companies usually trade at higher multiples, as investors are willing to pay more for future expansion opportunities. However, if the multiple rises too far, it may indicate market enthusiasm has outpaced fundamentals.

CrowdStrike currently trades at a P/S multiple of 31.1x. This is considerably higher than the Software industry average of 5.24x and also above the peer average of 15.15x. At first glance, this premium valuation appears significant.

Simply Wall St's proprietary Fair Ratio for CrowdStrike is 17.98x. Unlike traditional comparison methods, the Fair Ratio adjusts for the company’s unique growth outlook, profit margins, risks, and market size. This provides a more nuanced benchmark compared to a simple industry average or peer group.

Because CrowdStrike's current P/S multiple is substantially higher than its Fair Ratio, this suggests the stock is currently overvalued on this basis. In summary, high expectations for future performance appear to be fully reflected in the share price.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CrowdStrike Holdings Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is simply your personal story about a company, bringing together your expectations about its future, such as how much it will grow, what profits it will earn, and what its business will look like, to create a financial forecast and a fair value based on your own viewpoints.

With Narratives on Simply Wall St’s Community page, you do not need to just accept a generic fair value. You can easily adjust assumptions to see how your perspective changes the investment outlook, just like millions of other investors who use the platform. Narratives make it clear when a stock looks like a buy or sell by directly comparing your calculated Fair Value to the current share price.

Best of all, Narratives update automatically as new information, such as major news or earnings results, comes in. Your story and valuation can always reflect the latest situation.

For CrowdStrike Holdings, some investors believe its innovative platform and cloud-focused strategy could justify a fair value as high as $498.91, while others adopt a more cautious view with fair values closer to $330. This shows how Narratives help you make sense of differing opinions and decide what fits your own investment beliefs.

Do you think there's more to the story for CrowdStrike Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRWD

CrowdStrike Holdings

Provides cybersecurity solutions in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

138 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4844.4% undervalued

228 followersusers have followed this narrative

15 commentsusers have commented on this narrative

34 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43044.4% undervalued

31 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9954.7% undervalued

40 followersusers have followed this narrative

1 commentusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$5860.7% overvalued

40 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on UUE Holdings Berhad ·

UUE Holdings Berhad Reports Record Q1 FY2027 Financial Performance as Revenue Soars 88.9%

Fair Value:RM 0.831.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Infomina Berhad ·

Infomina: Ongoing Share Buybacks Strengthen an Already Compelling Growth Story

Fair Value:RM 3.151.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.2% undervalued

241 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9116.1% overvalued

113 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6284.3% overvalued

127 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

4

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0