- United States

- /

- Software

- /

- NasdaqGS:APP

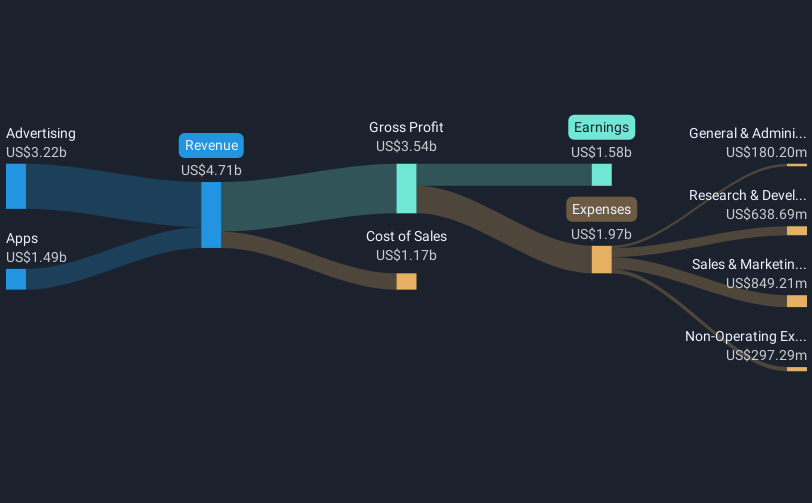

AppLovin (NasdaqGS:APP) Posts Strong Q1 Earnings with Substantial Year-Over-Year Growth

Reviewed by Simply Wall St

AppLovin (NasdaqGS:APP) recently experienced a significant share price increase of 58% over the past month, moving distinctly beyond the broader market's 5% increase over the last week. This notable performance came after the company reported strong Q1 earnings, with sales and net income showing substantial year-over-year growth and an increased EPS. The completion of a significant share buyback program also likely added momentum to the stock’s rise. However, the company faces challenges with a new securities class action lawsuit and a notable goodwill impairment, both of which might have tempered the overall enthusiasm surrounding its otherwise strong financial performance.

We've spotted 3 risks for AppLovin you should be aware of.

AppLovin’s recent share price surge by 58% over the past month, fueled by robust Q1 earnings and a significant share buyback, signals optimism around its strategic initiatives. However, the accompanying securities class action lawsuit and a notable goodwill impairment may introduce elements of risk that could affect its revenue growth and earnings forecasts. Despite these challenges, analysts foresee substantial revenue growth as the company pivots towards the global advertising market, leveraging AI-driven models for better operational efficiency and increased net margins. The potential short-term impacts may temper enthusiasm around long-term forecasts, considering the company's growth trajectory and market expansion goals.

Over the past three years, AppLovin has delivered a total shareholder return exceeding 800%, reflecting a strong upward trajectory. This performance contrasts with its recent outperforming of the US Software industry, which returned 17.3% over the past year. This long-term growth indicates a resilient market position, notwithstanding short-term fluctuations. As the current share price stands at US$304.62, the consensus analyst price target of US$432.90 suggests potential upward movement of approximately 29.6%. This aligns with analysts' expectations of continued robust earnings growth, contingent on the company's successful navigation of associated operational and market risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:APP

AppLovin

Engages in building a software-based platform for advertisers to enhance the marketing and monetization of their content in the United States and internationally.

High growth potential with solid track record.

Similar Companies

Market Insights

Community Narratives