- United States

- /

- Software

- /

- NasdaqGS:ADBE

Adobe (ADBE) Margin Expansion to 30% Reinforces Bullish Profitability Narratives

Reviewed by Simply Wall St

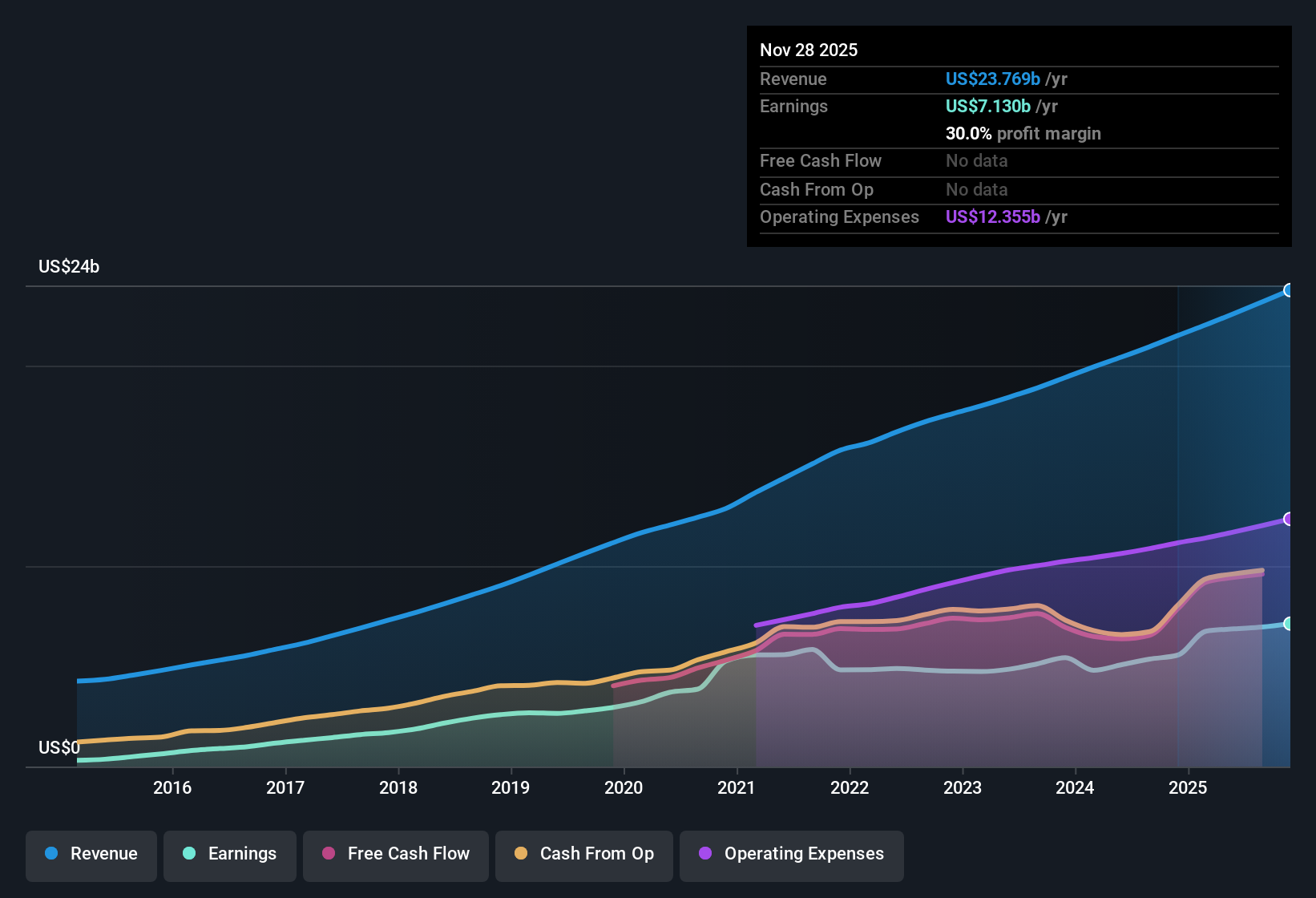

Adobe (ADBE) just closed out FY 2025 with Q4 revenue of $6.2 billion and basic EPS of $4.45, capping a year in which trailing twelve month revenue reached $23.8 billion and EPS came in at $16.74 alongside 28.3% earnings growth and a 30% net margin. Over the past few quarters, the company has seen revenue move from $5.6 billion in Q4 2024 to $6.2 billion in Q4 2025, while quarterly EPS stepped up from $3.82 to $4.45, setting the stage for investors to weigh solid profitability against more measured forward growth expectations.

See our full analysis for Adobe.With the latest numbers on the table, the next step is to see how this earnings profile lines up with the prevailing narratives around Adobe's growth, risk, and long term trajectory.

See what the community is saying about Adobe

Margins Step Up To 30%

- Over the last twelve months, Adobe generated about $7.1 billion of net income on $23.8 billion of revenue, which works out to a 30% net margin versus 25.9% a year earlier.

- Bulls point to this margin lift as evidence that AI and subscription scale are paying off, yet

- the bullish view assumes margins can climb further from roughly 30% toward 36.5% by 2028, while current data only confirms the move from 25.9% to 30% so far.

- at the same time, five year earnings growth of 5.5% per year is much lower than the latest 28.3% jump, so investors need to decide whether the recent margin and earnings spike is a new normal or a one year acceleration.

Growth Slows Toward Mid Single Digits

- Trailing twelve month earnings grew 28.3%, but forward expectations call for earnings growth of about 6.8% per year and revenue growth of 7.7% per year, both below the US market forecasts of 16.3% for earnings and 10.7% for revenue in the same dataset.

- Bears focus on these slower forecasts as a sign that AI driven products may not turn into runaway growth, and

- they note that even with Q4 revenue rising from $5.6 billion in 2024 to $6.2 billion in 2025, the longer term outlook still sits in the high single digit range rather than matching higher growth software peers.

- they also highlight that forecasts baking in around 7% annual revenue growth leave less room for upside if new offerings like Firefly and Acrobat AI Assistant fail to produce the step change some bulls are counting on.

Valuation Signals Versus Peers

- At a trailing P E of 20.6 times, Adobe trades below both the US software industry average of 32.7 times and a peer average of 58.5 times, while a DCF fair value of about $519.21 sits well above the current share price of $350.43.

- Supporters of the bullish narrative see this mix of lower multiple and higher DCF fair value as a valuation cushion, yet

- the same dataset shows forecast revenue growth of 7.7% per year and earnings growth of 6.8% per year, which helps explain why the market is not awarding the same multiple as faster growing software peers.

- the gap between the $350.43 share price and the $519.21 DCF fair value hinges on those growth and margin assumptions playing out, so any drift toward the more cautious growth paths that some analysts model would narrow that implied upside.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Adobe on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Use that perspective to shape your own view in just a few minutes and share it with the community, Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Adobe.

See What Else Is Out There

Adobe’s slower forecast growth and reliance on optimistic margin expansion assumptions leave investors exposed if the company settles into a more mature, mid single digit trajectory.

If that trade off feels too narrow, use our high growth potential stocks screener (44 results) to immediately focus on established names where consensus expects far stronger earnings momentum over the next few years.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026