- United States

- /

- Semiconductors

- /

- NYSE:WOLF

Wolfspeed (NYSE:WOLF) Showcases 200mm Tech Shift at UBS Conference, Tackles Key Challenges

Reviewed by Simply Wall St

Click to explore a detailed breakdown of our findings on Wolfspeed.

Innovative Factors Supporting Wolfspeed

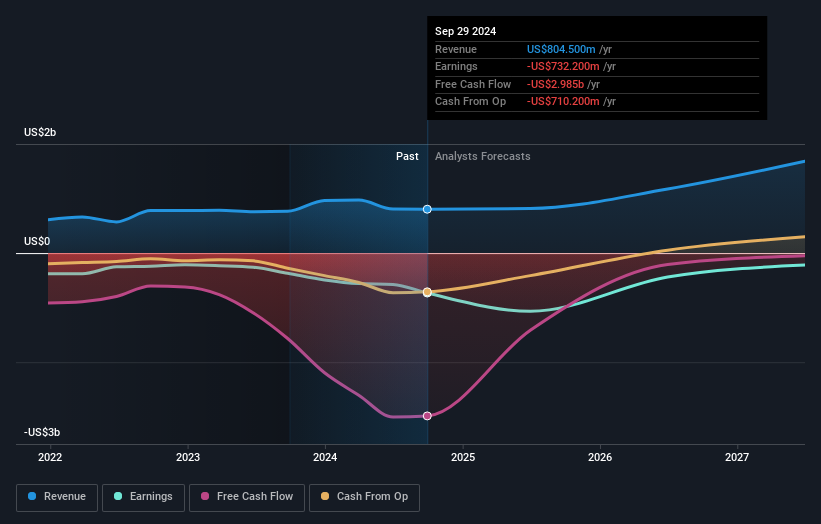

Wolfspeed's transition to 200-millimeter technology marks a pivotal moment in its evolution, as highlighted by CEO Gregg Lowe. This move enhances manufacturing efficiency and financial performance by reducing costs and increasing capacity utilization. The company's backlog of $11 billion in design wins, particularly in the electric vehicle sector, underscores strong demand and future revenue potential. Additionally, the CHIPS Act funding and additional debt financing bolster Wolfspeed's financial position, providing a solid foundation for its ambitious expansion plans. With a revenue growth forecast of 22.9% per year, significantly outpacing the US market average, Wolfspeed is poised for substantial growth. Moreover, its Price-To-Sales Ratio of 1.7x compared to the industry average of 4.2x suggests a competitive edge in the semiconductor space.

Strategic Gaps That Could Affect Wolfspeed

Operational challenges remain a concern, with CFO Neill Reynolds acknowledging the need for restructuring charges of $400 million to $450 million. These charges highlight inefficiencies and a high cost structure that Wolfspeed is addressing through facility closures and workforce reductions. The sequential 3% decline in revenue reflects pressures in the industrial and energy sectors, exacerbated by macroeconomic factors like rising interest rates. Moreover, underutilization costs, particularly at the Mohawk Valley facility, have impacted profitability, with a gross margin decrease to 3.4%. The company's high net debt to equity ratio of 712.7% and a return on equity of -116.43% further underscore financial challenges that need to be addressed.

Potential Strategies for Leveraging Growth and Competitive Advantage

The growing demand for silicon carbide in electric vehicles presents a significant opportunity for Wolfspeed, as emphasized by Lowe. With EV revenue growing 2.5 times year-over-year, the company is well-positioned to capitalize on this trend. The CHIPS Act funding of $750 million will enable Wolfspeed to expand its U.S. manufacturing capacity, strengthening its market leadership. Furthermore, a potential recovery in the industrial and energy markets by the first half of 2025 could open new revenue streams. Analysts' target price, set over 20% higher than the current share price, indicates potential upside and investor confidence in Wolfspeed's growth trajectory.

External Factors Threatening Wolfspeed

Economic headwinds, including high interest rates and delayed investment cycles, pose risks to Wolfspeed's growth, as noted by Lowe. The volatility of the share price over the past three months adds another layer of uncertainty. Additionally, changes in customer demand and competitive pressures in the semiconductor industry could impact market share and profitability. The reliance on meeting specific operational milestones to secure CHIPS funding presents a risk if delays occur. With less than a year of cash runway, financial stability remains a pressing concern, necessitating careful navigation of these external challenges.

See what the latest analyst reports say about Wolfspeed's future prospects and potential market movements.

Conclusion

Wolfspeed's strategic shift to 200-millimeter technology is a critical step in enhancing its manufacturing efficiency and financial performance, setting the stage for substantial growth driven by strong demand in the electric vehicle sector. However, the company faces significant operational challenges, including a high cost structure and underutilization issues, which are reflected in its restructuring charges and declining gross margins. While the CHIPS Act funding and potential recovery in key markets offer promising growth avenues, Wolfspeed must navigate economic headwinds and financial constraints, such as its high net debt to equity ratio and limited cash runway. Despite these challenges, Wolfspeed's Price-To-Sales Ratio of 1.7x, compared to the industry average of 4.2x, suggests it is competitively positioned in the semiconductor space, though it remains costly relative to its peers, indicating a need for strategic management to leverage its growth potential effectively.

Taking Advantage

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Wolfspeed, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wolfspeed might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WOLF

Wolfspeed

Operates as a bandgap semiconductor company focuses on silicon carbide and gallium nitride (GaN) technologies in Europe, Hong Kong, China, rest of Asia-Pacific, the United States, and internationally.

Undervalued slight.

Similar Companies

Market Insights

Community Narratives