Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:NVDA

Nvidia’s (NASDAQ:NVDA) Road Ahead May be Bumpy as the Company Plays the Long Game with Metaverse Strategy

NVIDIA Corporation ( NASDAQ:NVDA ) is in the enviable position of supplying components to some of the fastest growing industries in the world - including gaming, cloud computing, artificial intelligence, visualization, and cryptocurrency mining. With a market value of $538 billion, it is the 11th most valuable company listed on US markets, and on the verge of overtaking TSMC ( NYSE:TSM ) as the most valuable semiconductor manufacturer in the world.

However, when a company is the size of Nvidia, it becomes more difficult to maintain the growth rates that got it to that size in the first place. Amongst the world’s mega-cap companies, Nvidia has one of the richest valuations, apart perhaps from Tesla ( Nasdaq:TSLA ).

Nvidia's price-to-earnings (or "P/E") ratio of 74x is second only to Tesla amongst the 20 largest companies. And Nvidia’s price-to-sales (or "P/S") ratio of 24x is the highest amongst this group of companies. These metrics suggest that Nvidia and Tesla have the most future growth priced into their valuations amongst mega cap stocks.

See our latest analysis for NVIDIA

What is Nvidia worth?

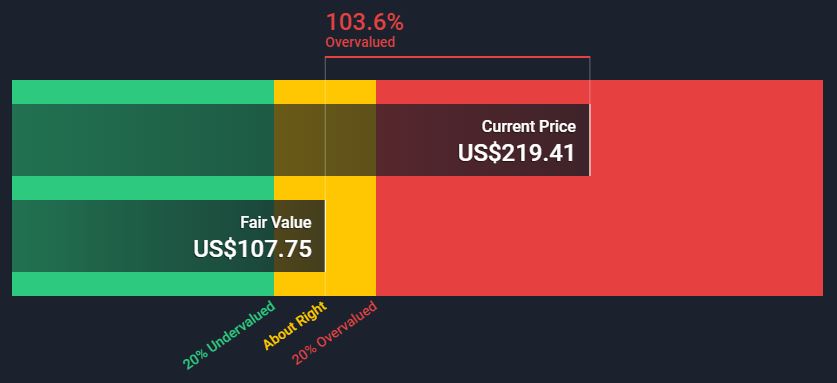

When we estimate Nvidia’s intrinsic value using analyst forecasts we arrive at a value of $107.75, implying the stock is overvalued by about 103%. This estimate is calculated using the 2 Stage Free Cash Flow to Equity and you can see the full calculation here .

Now the most important inputs to a discounted cash flow are the discount rate, and of course, the actual cash flows. Both of these can, and probably will change, over time - so the $107 value is just an estimate based on current forecasts.

Enter the Metaverse

Clearly the market believes Nvidia can grow faster than current forecasts suggest. One of the reasons for this is the metaverse, and Nvidia’s efforts to accelerate growth in the industries it supplies.

The metaverse is a virtual, 3D, digital world, or worlds. Currently, the metaverse is mostly confined to games like Fortnite and Minecraft. But in the future, the metaverse promises to be a place to work and play. It will see the full realization of the potential of virtual and augmented reality, and merge the real world with the internet.

Creating the metaverse requires cloud computing, artificial intelligence, and virtual and augmented reality - the same industries and technologies that make up some of Nvidia’s key markets. Nvidia’s CEO Jensen Huang believes t he economy in the metaverse will be larger than the economy in the physical world , though he tends to use the term omniverse rather than metaverse.

A core part of Nvidia’s growth strategy is providing the tools to make this a reality. These efforts fall within the Nvidia Omniverse, a platform for real time collaboration and simulation.

There are countless applications where companies can use any combination of AR, VR, and AI to increase efficiency, reduce costs and collaborate. Applications for industries like animation, gaming, architecture and automotive design are obvious. But there are applications in countless other industries too.

To create the platform, Nvidia has partnered with a large number of other companies including Adobe, Autodesk, Blender, and Pixar. This means Nvidia’s Omniverse is helping the users of all these products to make the metaverse a reality, and thereby increasing the size of Nvidia’s market.

Conclusion

If Jensen Huang’s prediction that the metaverse will be a bigger economy than the current physical economy comes anywhere close to being true, Nvidia will be one of its major suppliers, if not its largest supplier. This makes for a compelling investment case - but the metaverse is a long way from being a reality at scale, and stocks don’t move in a straight line.

The semiconductor industry is also cyclical, and earnings tend to be lumpy. Add to that the fact that Nvidia is trading at a substantial premium, and there’s potential for lots of volatility in the future.

We recently pointed out that trading by insiders suggested Nvidia may be nearing a peak. We may see lots of corrections of varying magnitudes in the future - this is the nature of companies that persistently trade at high valuations. Watching insider activity may be a good way to manage your own expectations. Insider activity and the ownership breakdown are included in our free analysis of Nvidia.

Valuation is complex, but we're here to simplify it.

Discover if NVIDIA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NasdaqGS:NVDA

NVIDIA

A computing infrastructure company, provides graphics and compute and networking solutions in the United States, Singapore, Taiwan, China, Hong Kong, and internationally.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor