Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:LSCC

Lattice Semiconductor (LSCC): Exploring Current Valuation After Recent Share Price Dip

Lattice Semiconductor (LSCC) has attracted renewed attention as investors assess the company’s performance over the past month, especially after a period of moderate volatility in the semiconductor sector. Shares have shifted slightly, which has prompted some fresh discussion around its valuation and growth profile.

See our latest analysis for Lattice Semiconductor.

After a sharp selloff in the last week, Lattice Semiconductor’s recent share price return stands at -11.98% for the past seven days and -13.04% over the month, despite an impressive 23.54% total shareholder return for the past year. Momentum has cooled lately, but long-term investors have still seen robust gains as the company’s fundamentals continue to evolve.

If this shift in momentum has you thinking about spotting the next opportunity, it may be the perfect moment to discover See the full list for free.

But with the stock trading below analyst price targets and strong long-term returns, investors may wonder if this recent dip is an attractive entry point for new investors or if the market has already factored in all of Lattice Semiconductor’s growth potential.

Most Popular Narrative: 9.5% Undervalued

The most popular narrative currently values Lattice Semiconductor at $69.85, higher than its last close of $63.23. With this fair value in mind, the latest narrative highlights how game-changing trends in AI and edge computing could shape the company’s long-term trajectory.

The ongoing AI and edge computing boom is driving hyperscale data center spend and increasing Lattice's attach rate as a companion chip for AI accelerators, servers, and networking equipment. This leads to higher ASPs and robust design wins, which could accelerate revenue growth and support gross margin expansion.

Curious about the bold quantitative leaps backing up this narrative’s fair value? The growth assumptions make this story stand out. Find out what future profit margins and revenue targets analysts are betting on, and what it could take for Lattice to surprise the market.

Result: Fair Value of $69.85 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent competition and regulatory risks remain potential headwinds that could challenge Lattice's current growth projections and alter the bullish outlook.

Find out about the key risks to this Lattice Semiconductor narrative.

Another View: Multiples Raise a Red Flag

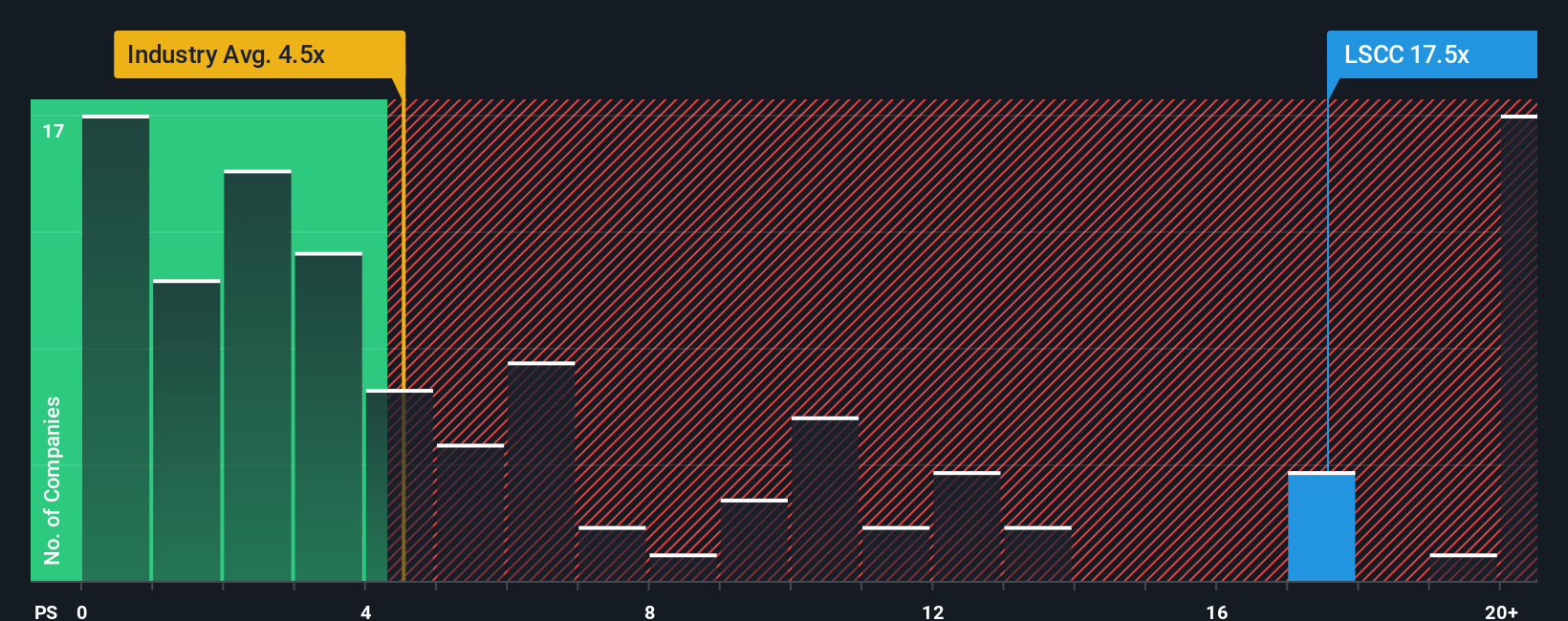

While narratives and analyst targets paint Lattice Semiconductor as undervalued, a closer look at its price-to-sales ratio tells a different story. At 17.5x, it is considerably higher than both the US semiconductor industry average of 5.3x and the calculated fair ratio of 10.1x. This kind of gap signals meaningful valuation risk. Could momentum alone keep the story alive, or will the market eventually catch up with fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Lattice Semiconductor Narrative

If you think there is more to the story or want to test your own analysis, it only takes a few minutes to build a personal view and share insights. Do it your way

A great starting point for your Lattice Semiconductor research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for More Standout Investment Opportunities?

Don’t miss out on innovative ideas beyond Lattice Semiconductor. Smart investors are logging in every day to spot their next move using the powerful Simply Wall Street Screener.

- Capitalize on market mispricing with these 842 undervalued stocks based on cash flows to reveal companies trading below their true potential and set up your portfolio for growth.

- Unlock long-term income by checking out these 18 dividend stocks with yields > 3% for stocks paying reliable yields above 3% and strengthening your passive cashflow strategy.

- Catch the next tech wave early by jumping into these 27 AI penny stocks to find those shaping the future of artificial intelligence and automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LSCC

Lattice Semiconductor

Develops and sells semiconductor, silicon-based and silicon-enabling, evaluation boards, and development hardware products in Asia, Europe, and the Americas.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative