- United States

- /

- Semiconductors

- /

- NasdaqGS:KLIC

Is Kulicke and Soffa Industries (NASDAQ:KLIC) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Kulicke and Soffa Industries, Inc. (NASDAQ:KLIC) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Kulicke and Soffa Industries

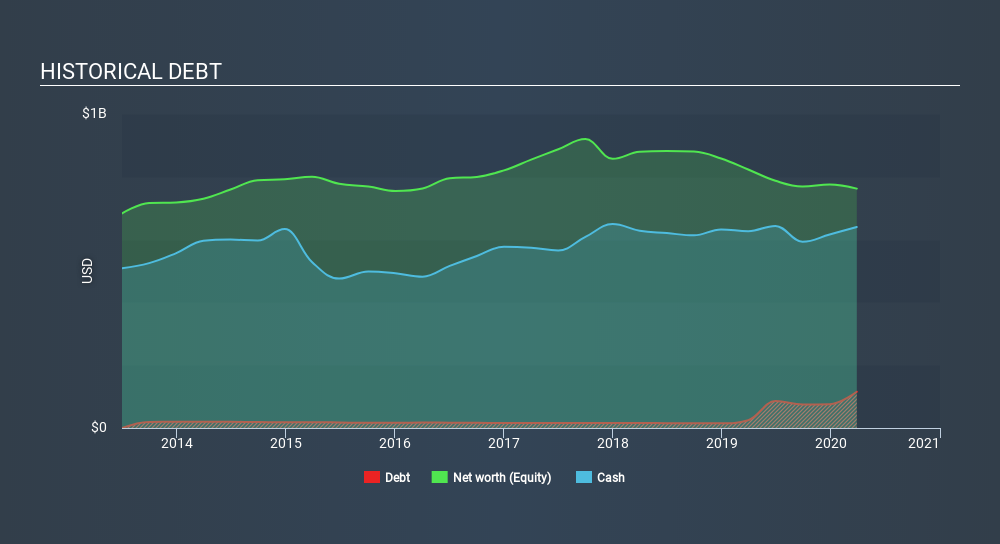

What Is Kulicke and Soffa Industries's Debt?

The image below, which you can click on for greater detail, shows that at March 2020 Kulicke and Soffa Industries had debt of US$115.6m, up from US$24.9m in one year. However, its balance sheet shows it holds US$640.3m in cash, so it actually has US$524.7m net cash.

A Look At Kulicke and Soffa Industries's Liabilities

According to the last reported balance sheet, Kulicke and Soffa Industries had liabilities of US$262.0m due within 12 months, and liabilities of US$136.5m due beyond 12 months. Offsetting this, it had US$640.3m in cash and US$199.8m in receivables that were due within 12 months. So it actually has US$441.6m more liquid assets than total liabilities.

This surplus suggests that Kulicke and Soffa Industries is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Simply put, the fact that Kulicke and Soffa Industries has more cash than debt is arguably a good indication that it can manage its debt safely.

In fact Kulicke and Soffa Industries's saving grace is its low debt levels, because its EBIT has tanked 67% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Kulicke and Soffa Industries can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Kulicke and Soffa Industries has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Kulicke and Soffa Industries generated free cash flow amounting to a very robust 89% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Kulicke and Soffa Industries has net cash of US$524.7m, as well as more liquid assets than liabilities. The cherry on top was that in converted 89% of that EBIT to free cash flow, bringing in US$12m. So is Kulicke and Soffa Industries's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Kulicke and Soffa Industries you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NasdaqGS:KLIC

Kulicke and Soffa Industries

Designs, manufactures, and sells capital equipment and consumables in China, the United States, Taiwan, Malaysia, Japan, the Philippines, Korea, Hong Kong, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

CS Disco Stock: Legal AI Is Moving From Efficiency Tool to Competitive Necessity

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)