Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:FSLR

Is First Solar’s Recent 15% Stock Rally Justified After Latest Earnings Outlook?

Simply Wall St

Reviewed by Bailey Pemberton

Thinking about what to do with First Solar stock right now? You are not alone. With all the excitement in the renewable energy sector and the market in general, First Solar has been a hot topic among both new investors and seasoned pros. Just check out the numbers: the stock climbed 15.4% in the last 30 days and 25.7% since the start of the year. Even looking back further, it is up an impressive 184.8% over the past five years. Such strong momentum naturally raises questions about whether First Solar remains a smart investment at its current price or if it is already overvalued.

Much of this recent surge can be traced to growing optimism around clean energy policy shifts and new market incentives for solar technology. These changes have put companies like First Solar in the spotlight. As investors re-examine risk and growth in the sector, sentiment has clearly tilted toward opportunity, and the price action reflects it.

But price moves only tell part of the story. To get a clear sense of whether First Solar is a bargain or fair valued, we need to look at several established valuation checks. By those measures, the company clocks a value score of 4 out of 6, suggesting it is undervalued in two-thirds of the key areas analysts watch most closely.

So how do these valuation methods stack up, and how confident should you feel about the number? Let us break down each approach. At the end, I will also share a perspective that goes beyond the usual checks and might just shift how you look at First Solar’s true value altogether.

Why First Solar is lagging behind its peers

Approach 1: First Solar Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model takes First Solar’s expected future cash flows and discounts them back to today’s value, giving investors a way to estimate what the company is truly worth right now. This approach focuses on how much cash the company is likely to generate over time and then applies a discount to account for the time value of money and risk.

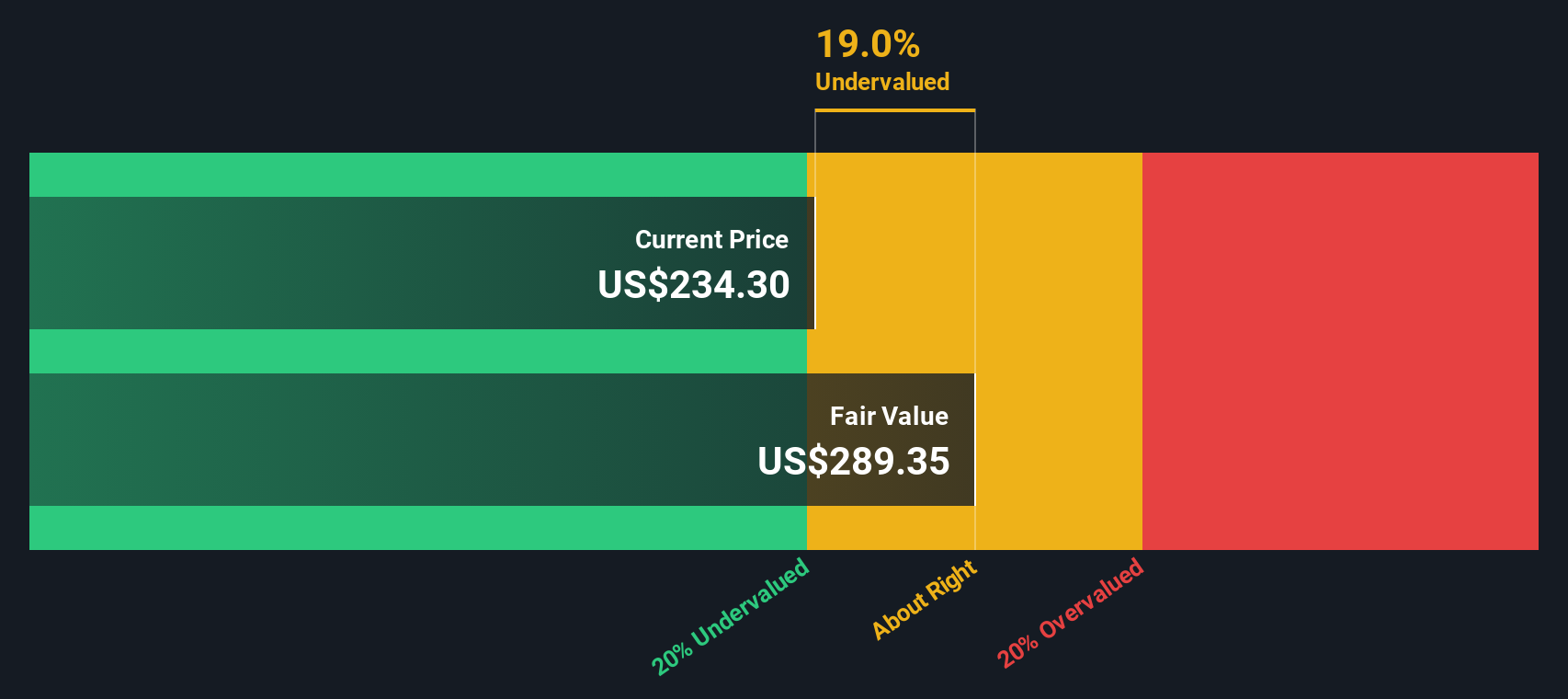

Currently, First Solar’s latest twelve months (LTM) Free Cash Flow stands at a deficit of $1.25 billion. However, analyst forecasts suggest rapid improvements. In five years, projections point to Free Cash Flow reaching $2.84 billion. Further gains are estimated beyond that based on extrapolation by Simply Wall St. This indicates not only a sharp turnaround but also robust growth expectations in the coming decade.

The outcome of the DCF model pegs First Solar’s intrinsic fair value at $289.35 per share. This implies the stock is trading at a 19.0% discount to its true worth, suggesting there is meaningful upside still on the table for investors at current market prices.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests First Solar is undervalued by 19.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: First Solar Price vs Earnings

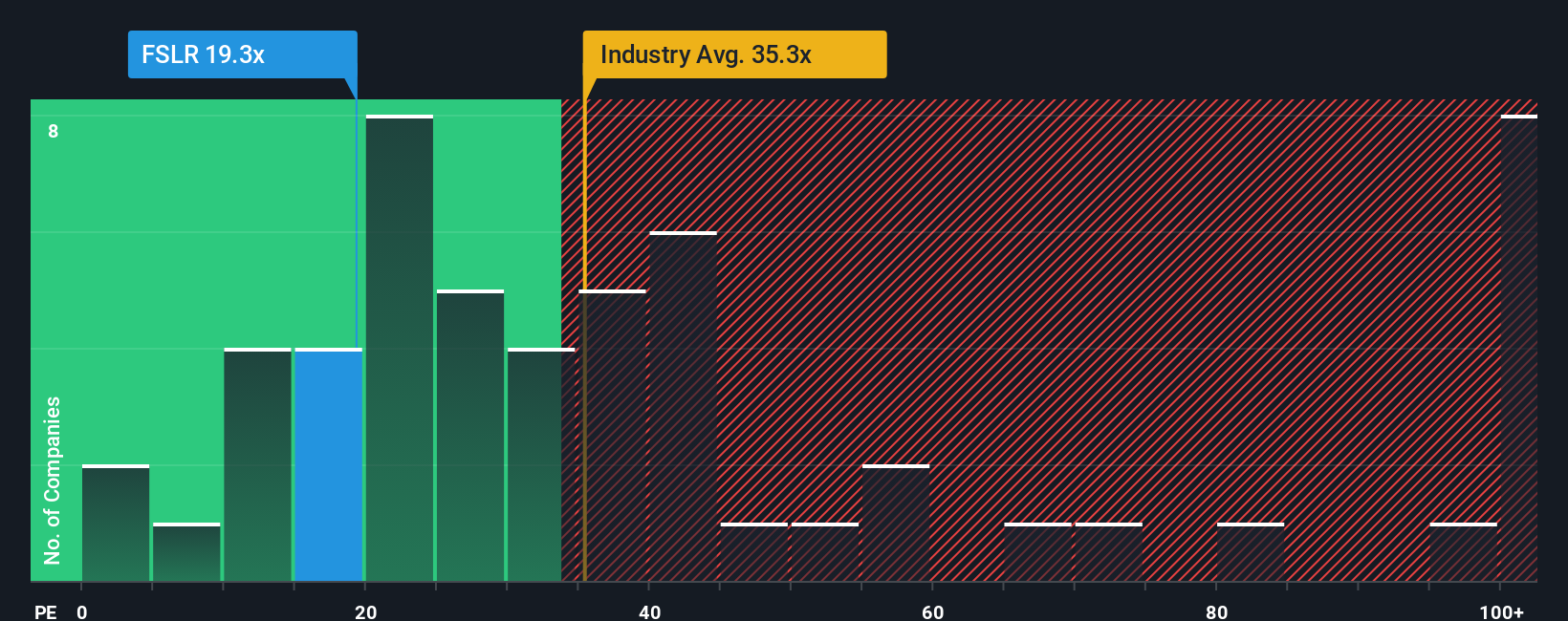

For a profitable and growing company like First Solar, the Price-to-Earnings (PE) ratio is a common and useful valuation tool. It tells investors how much they are paying for each dollar of earnings, making it easier to compare across similar businesses. Especially for companies actively generating profits, the PE ratio reflects both current performance and the market’s expectations of future growth and risk.

Higher growth expectations or lower perceived risk typically justify a higher “fair” PE ratio, since investors are willing to pay up for future potential. Conversely, slower growth or higher risk usually warrants a lower PE. Understanding where First Solar sits on this scale helps determine whether the stock’s current price makes sense.

Right now, First Solar trades at a PE ratio of 20x. That is well below the semiconductor industry average of 38.3x and even further below the peer group average of 81.1x. This initially suggests the shares might be undervalued compared to other players in the space. However, simply comparing with the industry can miss important context, such as differences in growth or profitability across companies.

This is where the Simply Wall St “Fair Ratio” comes in. Unlike a basic industry comparison, this proprietary measure estimates what a reasonable PE ratio should be for First Solar specifically, by factoring in its unique earnings growth outlook, profit margins, market cap, and risk profile. In First Solar’s case, the Fair Ratio sits at 37.5x, reflecting the premium it deserves based on its fundamentals and future prospects.

Comparing the Fair Ratio to the company’s current PE ratio, there is a sizeable gap. First Solar’s shares trade at just over half of what their tailored multiple would justify. This points to the stock being meaningfully undervalued on an earnings basis, even after accounting for growth, risks, and the bigger industry picture.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your First Solar Narrative

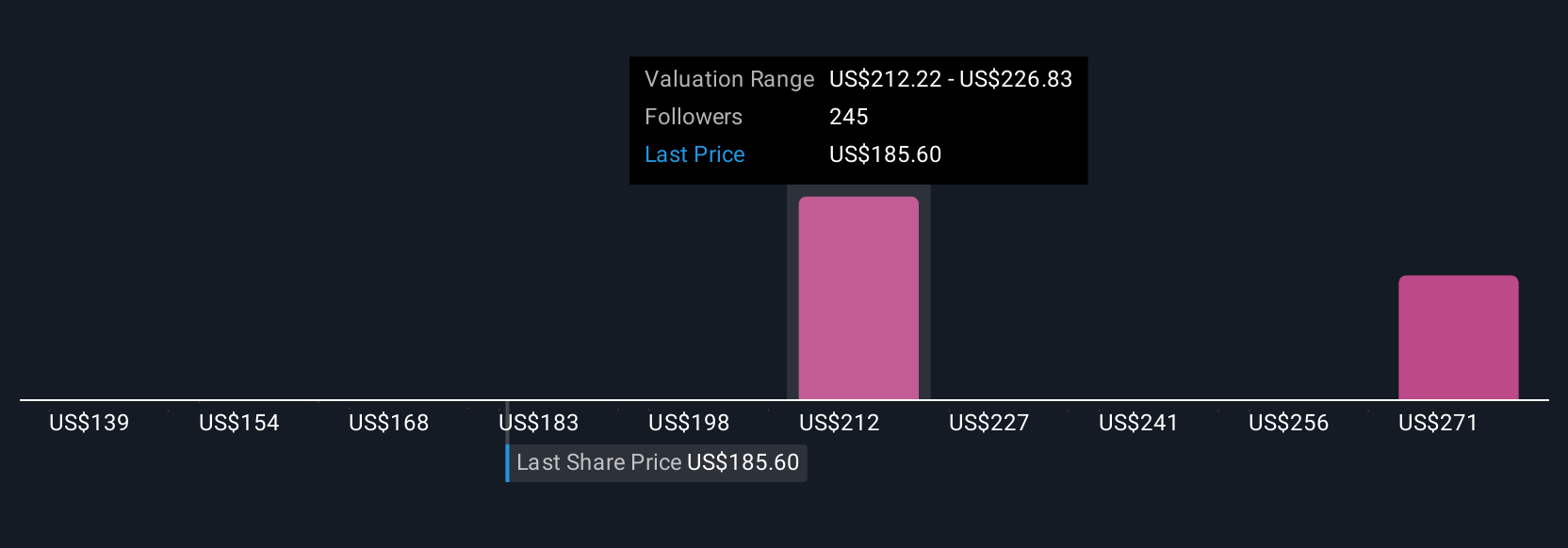

Earlier, we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. In investing, a Narrative is a simple, powerful tool that lets you connect the story you believe about a company, such as where you think First Solar is headed and what could drive its profits, to a forecast for revenue and earnings, and ultimately to your personal estimate of fair value.

Narratives make your assumptions and expectations explicit, turning your perspective on things like market trends, new policies, or innovation into a set of clear, testable numbers. On Simply Wall St’s platform, available in the Community page, millions of investors can easily craft or discover Narratives for companies, helping you base your decisions on more than just industry averages or analyst targets.

By comparing your Narrative’s fair value number to the current share price, you can quickly see if First Solar looks attractive or overpriced for your unique view. Thanks to real-time updates, your Narrative evolves as news, results, or fresh forecasts roll in.

For example, one Narrative might assume rapid U.S. expansion and stable policy support, resulting in a projected fair value as high as $287 per share. A more cautious view, emphasizing risks from global competition and policy changes, could yield a lower fair value near $100 per share.

Do you think there's more to the story for First Solar? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FSLR

First Solar

A solar technology company, provides photovoltaic (PV) solar energy solutions in the United States, France, India, Chile, and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor