Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:CSIQ

Will Analyst Concerns Over Margins Reshape Canadian Solar’s (CSIQ) Regulatory and Growth Outlook?

Simply Wall St

Reviewed by Sasha Jovanovic

- Recently, JPMorgan highlighted Canadian Solar as a short opportunity in the energy sector, citing increased input costs and regulatory headwinds, while Goldman Sachs reiterated a cautious outlook.

- This convergence of analyst concerns underscores the mounting challenges Canadian Solar faces in maintaining profitability and meeting compliance standards amid rising polysilicon prices and evolving U.S. regulations.

- We'll explore how mounting regulatory and margin pressures highlighted by analysts may reshape Canadian Solar's investment case and growth prospects.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Canadian Solar Investment Narrative Recap

At its core, holding Canadian Solar stock is about believing in the long-term rise of global solar and battery storage demand, aided by product innovation and geographic reach. The recent analyst warnings, prompted by rising input costs (like polysilicon) and regulatory threats in the U.S., directly challenge the near-term margin recovery that many investors see as the most important catalyst, while also sharpening focus on profitability risk, the company’s biggest near-term hurdle.

One recent announcement that stands out in this context is the launch of Canadian Solar’s next-generation Low Carbon modules, starting deliveries in August 2025. This product emphasizes improved efficiency and reduced carbon footprint, which could bolster competitiveness if the company can contain cost pressures, highlighting the push-pull between margin risks and technical advancement.

However, despite this technological progress, investors should not overlook the risk that recent regulatory changes in the U.S. could quickly ...

Read the full narrative on Canadian Solar (it's free!)

Canadian Solar's outlook anticipates $8.0 billion in revenue and $201.9 million in earnings by 2028. This forecast relies on 10.4% annual revenue growth and a $208.8 million earnings increase from the current -$6.9 million.

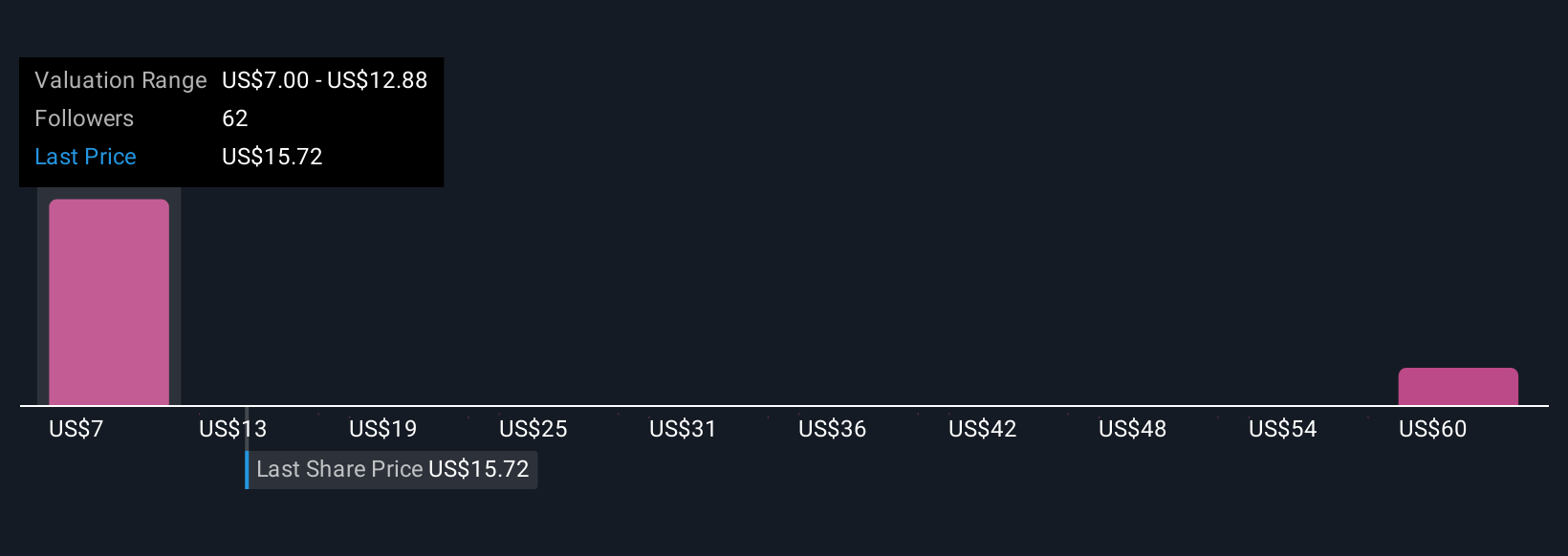

Uncover how Canadian Solar's forecasts yield a $12.37 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Six estimates from the Simply Wall St Community place Canadian Solar's fair value between US$12.37 and US$65.81. With such a wide spread and margin headwinds in focus, consider how much analyst and community sentiment can swing based on shifting supply chain or policy risks.

Explore 6 other fair value estimates on Canadian Solar - why the stock might be worth 8% less than the current price!

Build Your Own Canadian Solar Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Canadian Solar research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Canadian Solar research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Canadian Solar's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSIQ

Canadian Solar

Provides solar energy and battery energy storage products and solutions in Asia, the Americas, Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|10.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|12.0% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor