Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:HD

Why Home Depot's (NYSE:HD) Fundamentals are Better than Expected

We saw the price of Home Depot, Inc. (NYSE:HD) drop some 25% from its January highs to around US$310 on the last close. In this analysis, we will review if the fundamentals justify the price on a relative and intrinsic basis.

If you just want a glance, here is what we found.

Analysis Key Takeaways:

- HD is trading around intrinsic value

- Relative analysis also shows that earnings justify the current market cap

- HD has a large 54% return on capital and a good amount of moat with its 10% profit margin

- Future consumer spending capacity may be a significant risk

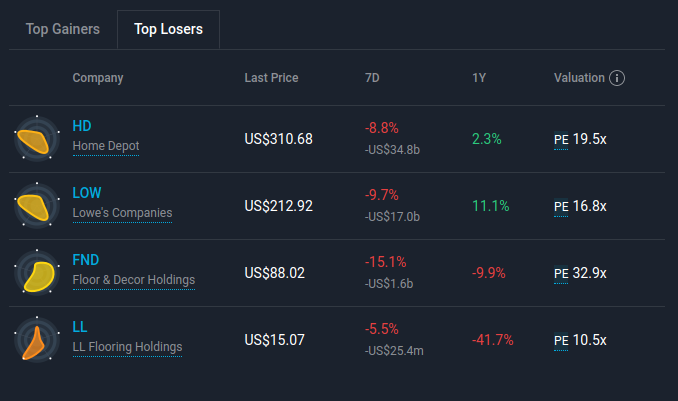

We were drawn to the Home Depot stock while screening for home improvement retail stores (top losers). You can view their competitors and possibly find something more interesting on our Markets tab:

Fundamental Snapshot

The company has a steady growth line, which jumped in 2020. Current revenues are US$151b for the last 12 months, which grew about 37% from FY 2020.

Home Depot has a market cap of US$321b with US$16.4b of net income - a margin of 10.8%, and free cash flows of US$14b.

This gives the company an attractive price to earnings ratio of 19.5x and an enterprise value to free cash flow ratio of 25.4x. We use EV instead of price because free cash flows are before debt payments. This way, we can say that investors pay $25 for every $1 of free cash flows. In other words, it should take 25 years for investors to double their money. This may look like a good or bad investment depending on your time horizon, and whether you prioritize stability or growth.

Home Depot also has some amazing returns!

For example, return on assets is 24.7%, stemming from the fact that they can operate their stores with 490k employees. As well as a return on capital employed of 54%! This comes from the relatively high profit margin.

Additionally, HD has a current dividend yield of 2.45%, and has been consistently increasing their dividend per share in the last 10 years.

Finally, we turn to the future, and see that analysts are expecting the Home Depot to grow revenues by 3% and earnings by 3.8% annually. This is a stable growth rate suitable for mature companies, which in turn, allows us to make a good valuation model.

Home Depot Valuation

We would caution that there are many ways of valuing a company and, like the DCF, each technique has advantages and disadvantages in certain scenarios. If you still have some burning questions about this type of valuation, take a look at the Simply Wall St analysis model.

See our latest analysis for Home Depot

We use what is known as a 2-stage model, which simply means we have two different periods of growth rates for the company's cash flows. Generally, we assume that a dollar today is more valuable than a dollar in the future, so we need to discount the sum of these future cash flows to arrive at a present value estimate:

10-year free cash flow (FCF) forecast

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF ($, Millions) | US$15.9b | US$17.1b | US$17.8b | US$18.0b | US$18.5b | US$19.2b | US$19.6b | US$20.0b | US$20.4b | US$20.9b |

| Growth Rate Estimate Source | Analyst x11 | Analyst x11 | Analyst x10 | Analyst x4 | Analyst x2 | Analyst x2 | Est @ 2.3% | Est @ 2.19% | Est @ 2.11% | Est @ 2.05% |

| Present Value ($, Millions) Discounted @ 6.9% | US$14.9k | US$14.9k | US$14.6k | US$13.7k | US$13.2k | US$12.8k | US$12.3k | US$11.7k | US$11.2k | US$10.7k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$130b

The second stage is also known as Terminal Value. We discount the terminal cash flows to today's value at a cost of equity of 6.9%.

Terminal Value (TV)= FCF2031 × (1 + g) ÷ (r – g) = US$21b× (1 + 1.9%) ÷ (6.9%– 1.9%) = US$426b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$426b÷ ( 1 + 6.9%)10= US$218b

The total value, or equity value, is then the sum of the present value of the future cash flows, which in this case is US$348b.

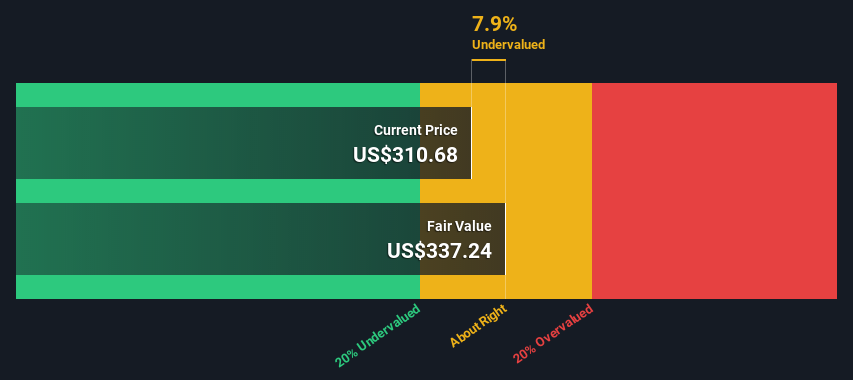

Relative to the current share price of US$311, the company appears about fair value at a 7.9% discount to where the stock price trades currently.

Our valuation model indicates that the company is trading around intrinsic value, which makes sense given the earnings and free cash flows it is making. Investors might have expected more growth in the beginning of 2022, but given the current situation, a retention of current revenue levels is required in order to justify the current value for Home Depot.

Investors that think that the company will have issues with consumer demand and pricing power, might expect a decline in growth, which would make them bearish on the stock.

Looking Ahead:

For Home Depot, we've put together three fundamental factors you should assess:

- Risks: For example, we've discovered 2 warning signs for Home Depot that you should be aware of before investing here.

- Future Earnings: How does HD's growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other High Quality Alternatives: Do you like a good all-rounder? Explore our interactive list of high quality stocks to get an idea of what else is out there you may be missing!

PS. Simply Wall St updates its DCF calculation for every American stock every day, so if you want to find the intrinsic value of any other stock just search here.

Valuation is complex, but we're here to simplify it.

Discover if Home Depot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:HD

Home Depot

Operates as a home improvement retailer in the United States and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor