Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:AKA

a.k.a. Brands Holding (NYSE:AKA) May Have Issues Allocating Its Capital

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. In light of that, when we looked at a.k.a. Brands Holding (NYSE:AKA) and its ROCE trend, we weren't exactly thrilled.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for a.k.a. Brands Holding, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0089 = US$3.8m ÷ (US$510m - US$88m) (Based on the trailing twelve months to December 2022).

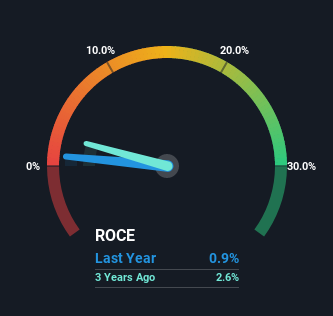

Therefore, a.k.a. Brands Holding has an ROCE of 0.9%. In absolute terms, that's a low return and it also under-performs the Specialty Retail industry average of 13%.

View our latest analysis for a.k.a. Brands Holding

In the above chart we have measured a.k.a. Brands Holding's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for a.k.a. Brands Holding.

SWOT Analysis for a.k.a. Brands Holding

Strength

- Debt is well covered by .

Weakness

- Interest payments on debt are not well covered.

Opportunity

- Forecast to reduce losses next year.

- Good value based on P/S ratio and estimated fair value.

- Significant insider buying over the past 3 months.

Threat

- Debt is not well covered by operating cash flow.

- Has less than 3 years of cash runway based on current free cash flow.

How Are Returns Trending?

In terms of a.k.a. Brands Holding's historical ROCE movements, the trend isn't fantastic. Over the last three years, returns on capital have decreased to 0.9% from 2.6% three years ago. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

In Conclusion...

In summary, a.k.a. Brands Holding is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. Moreover, since the stock has crumbled 88% over the last year, it appears investors are expecting the worst. All in all, the inherent trends aren't typical of multi-baggers, so if that's what you're after, we think you might have more luck elsewhere.

If you want to know some of the risks facing a.k.a. Brands Holding we've found 2 warning signs (1 is a bit concerning!) that you should be aware of before investing here.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:AKA

a.k.a. Brands Holding

Operates a portfolio of online fashion brands in the United States, Australia, New Zealand, and internationally.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor