- United States

- /

- Specialty Stores

- /

- NasdaqGS:ULTA

Ulta Beauty (NASDAQ:ULTA) stock performs better than its underlying earnings growth over last five years

When we invest, we're generally looking for stocks that outperform the market average. And the truth is, you can make significant gains if you buy good quality businesses at the right price. For example, long term Ulta Beauty, Inc. (NASDAQ:ULTA) shareholders have enjoyed a 97% share price rise over the last half decade, well in excess of the market return of around 56% (not including dividends). However, more recent returns haven't been as impressive as that, with the stock returning just 18% in the last year.

Since the stock has added US$1.0b to its market cap in the past week alone, let's see if underlying performance has been driving long-term returns.

Though if you're not interested in researching what drove ULTA's performance, we have a free list of interesting investing ideas to potentially inspire your next investment!

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

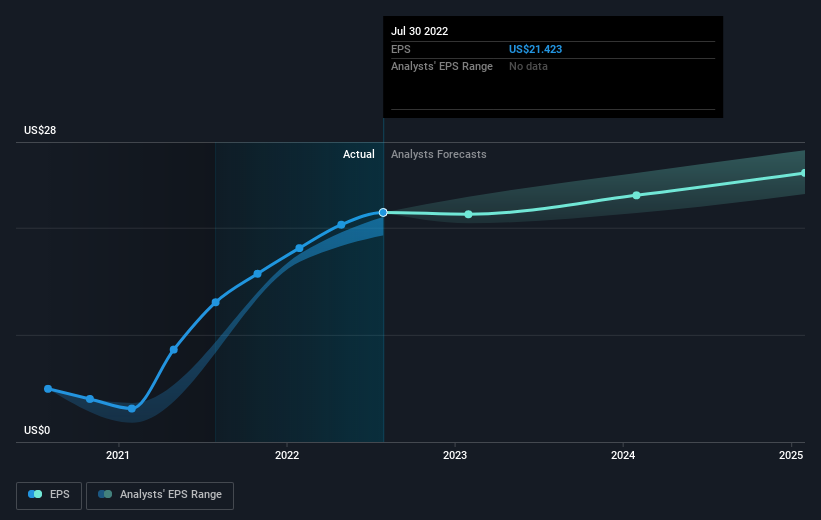

During five years of share price growth, Ulta Beauty achieved compound earnings per share (EPS) growth of 24% per year. This EPS growth is higher than the 15% average annual increase in the share price. Therefore, it seems the market has become relatively pessimistic about the company.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

We know that Ulta Beauty has improved its bottom line lately, but is it going to grow revenue? If you're interested, you could check this free report showing consensus revenue forecasts.

A Different Perspective

It's good to see that Ulta Beauty has rewarded shareholders with a total shareholder return of 18% in the last twelve months. Since the one-year TSR is better than the five-year TSR (the latter coming in at 15% per year), it would seem that the stock's performance has improved in recent times. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 1 warning sign we've spotted with Ulta Beauty .

But note: Ulta Beauty may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ULTA

Ulta Beauty

Operates as a specialty beauty retailer in the United States.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives