Advertisement

JD.com (NASDAQ:JD) Has A Rock Solid Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that JD.com, Inc. (NASDAQ:JD) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for JD.com

What Is JD.com's Debt?

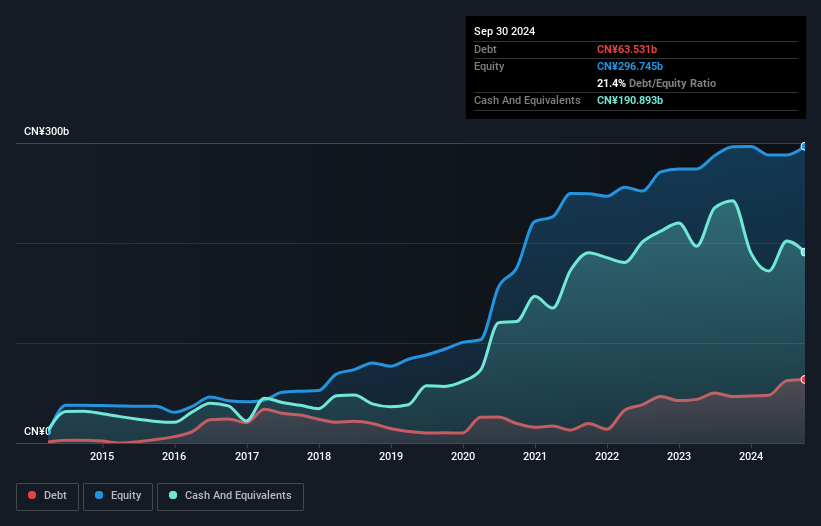

You can click the graphic below for the historical numbers, but it shows that as of September 2024 JD.com had CN¥63.5b of debt, an increase on CN¥46.5b, over one year. However, its balance sheet shows it holds CN¥190.9b in cash, so it actually has CN¥127.4b net cash.

A Look At JD.com's Liabilities

According to the last reported balance sheet, JD.com had liabilities of CN¥265.6b due within 12 months, and liabilities of CN¥81.3b due beyond 12 months. Offsetting this, it had CN¥190.9b in cash and CN¥22.9b in receivables that were due within 12 months. So it has liabilities totalling CN¥133.0b more than its cash and near-term receivables, combined.

This deficit isn't so bad because JD.com is worth a massive CN¥428.0b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. Despite its noteworthy liabilities, JD.com boasts net cash, so it's fair to say it does not have a heavy debt load!

On top of that, JD.com grew its EBIT by 35% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if JD.com can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While JD.com has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, JD.com actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing Up

While JD.com does have more liabilities than liquid assets, it also has net cash of CN¥127.4b. The cherry on top was that in converted 109% of that EBIT to free cash flow, bringing in CN¥28b. So is JD.com's debt a risk? It doesn't seem so to us. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of JD.com's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:JD

JD.com

Operates as a supply chain-based technology and service provider in the People’s Republic of China and Europe.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

275 followersusers have followed this narrative

1 commentusers have commented on this narrative

38 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.5% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4522.8% undervalued

3 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2802.3% undervalued

57 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on IREN ·

IREN to Transform into AI Cloud Giant with Mirantis Acquisition

Fair Value:US$44.323.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4050.1% undervalued

35 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

Coward_Nutlick on Elicio Therapeutics ·

Very Bullish

Fair Value:US$10089.4% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.8% undervalued

1394 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

32 likesusers have liked this narrative