- United States

- /

- Specialty Stores

- /

- NasdaqGS:EYE

Revenues Tell The Story For National Vision Holdings, Inc. (NASDAQ:EYE) As Its Stock Soars 38%

National Vision Holdings, Inc. (NASDAQ:EYE) shareholders have had their patience rewarded with a 38% share price jump in the last month. Notwithstanding the latest gain, the annual share price return of 4.8% isn't as impressive.

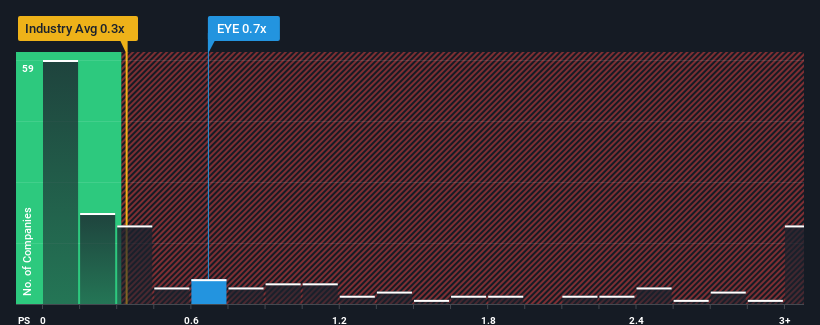

Even after such a large jump in price, there still wouldn't be many who think National Vision Holdings' price-to-sales (or "P/S") ratio of 0.7x is worth a mention when the median P/S in the United States' Specialty Retail industry is similar at about 0.3x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for National Vision Holdings

What Does National Vision Holdings' P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, National Vision Holdings' revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think National Vision Holdings' future stacks up against the industry? In that case, our free report is a great place to start.How Is National Vision Holdings' Revenue Growth Trending?

In order to justify its P/S ratio, National Vision Holdings would need to produce growth that's similar to the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 14%. This means it has also seen a slide in revenue over the longer-term as revenue is down 11% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Shifting to the future, estimates from the ten analysts covering the company suggest revenue should grow by 4.8% over the next year. That's shaping up to be similar to the 4.9% growth forecast for the broader industry.

With this in mind, it makes sense that National Vision Holdings' P/S is closely matching its industry peers. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

What Does National Vision Holdings' P/S Mean For Investors?

Its shares have lifted substantially and now National Vision Holdings' P/S is back within range of the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

A National Vision Holdings' P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Specialty Retail industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. All things considered, if the P/S and revenue estimates contain no major shocks, then it's hard to see the share price moving strongly in either direction in the near future.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for National Vision Holdings with six simple checks on some of these key factors.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if National Vision Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:EYE

National Vision Holdings

Through its subsidiaries, operates as an optical retailer in the United States.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives