- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Amazon.com (AMZN) Partners With Sendbird To Enhance AI Capabilities And Market Reach

Reviewed by Simply Wall St

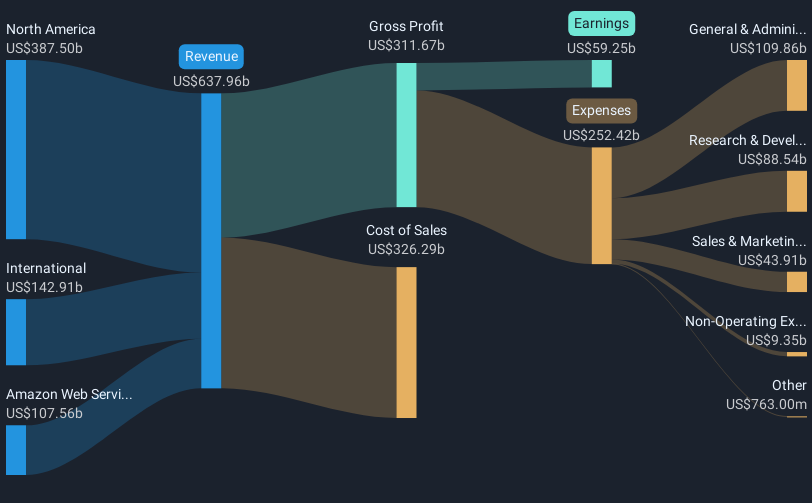

Sendbird Inc.'s recent collaboration with AWS marks a significant development in the AI agent space, likely aligning positively with market expectations for growth in agentic AI. During the last quarter, Amazon.com (AMZN) saw its stock price move 5%, a change that can be attributed to a combination of factors, including its robust Q2 earnings report and the completion of a substantial share repurchase program. The company's strategic partnerships and expansion initiatives, such as the $10 billion investment in North Carolina for infrastructure, complemented broader market trends, which have been buoyant with the S&P 500 and Nasdaq hitting all-time highs.

The collaboration between Sendbird Inc. and AWS could enhance Amazon's role in AI-driven solutions, particularly in the AI agent space. This complements the narrative that cloud transition and AI adoption will propel Amazon’s growth. The ongoing development in AI, coupled with AWS's leadership, might positively influence future revenue and earnings forecasts, as AWS leverages its infrastructure to meet increasing AI demands. However, competitive and regulatory pressures remain, potentially affecting the ability to maintain margins.

Over a three-year period, Amazon's total shareholder return reached 54.56%, underscoring strong performance. This return outpaced the US Multiline Retail industry’s one-year performance, where Amazon exceeded the 28.3% industry gain. In comparison to the broader market, Amazon also surpassed the US Market's 19.4% increase over the past year.

Considering the current share price of US$221.30 against the consensus price target of US$262.14, there is an 18.46% discount to the target, suggesting room for growth if forecasts align with reality. This potential upside reflects analyst expectations, hinging on whether Amazon can achieve anticipated revenue and earnings milestones. The recent news and strategic developments might aid in closing the gap towards the price target, as market confidence in the company's growth initiatives strengthens.

Examine Amazon.com's earnings growth report to understand how analysts expect it to perform.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fiducian: Compliance Clouds or Value Opportunity?

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Recently Updated Narratives

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Significantly undervalued gold explorer in Timmins, finally getting traction

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026