- United States

- /

- Specialized REITs

- /

- NYSE:WY

Reassessing Weyerhaeuser After a 7.8% Weekly Jump and Mixed Valuation Signals

Reviewed by Bailey Pemberton

- Wondering if Weyerhaeuser is quietly turning into a value opportunity in the beaten up real estate space, or if it is cheap for a reason? This breakdown is designed to give you a clear, no jargon answer.

- After a tough stretch where the stock is still down 16.4% year to date and 19.6% over the last year, a sharp 7.8% jump in the past week and 5.7% over the last month suggests investors are starting to reassess the risk reward balance.

- Recent moves have come as investors refocus on long term demand for timber and wood products and how Weyerhaeuser's vast timberland portfolio might benefit from any recovery in construction and housing markets. At the same time, shifting expectations for interest rates and real estate valuations have put the entire REIT and property complex back under the microscope, which helps explain the renewed volatility.

- On our framework, Weyerhaeuser only scores a 2/6 valuation score, with just two checks suggesting the shares look undervalued, so the headline numbers are not screaming bargain yet. In the sections that follow we will walk through the main valuation approaches behind that score, and then finish with a more holistic way to think about what this stock is really worth.

Weyerhaeuser scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Weyerhaeuser Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a business is worth by projecting the cash it can return to shareholders in future years and then discounting those cash flows back into today’s dollars.

For Weyerhaeuser, the latest twelve-month Free Cash Flow is about $533.7 million. Analysts and internal forecasts used in this model assume that figure rises over time, with projected Free Cash Flow of roughly $1.34 billion in 2035. The first few years are based on analyst estimates, while later years are extrapolated using Simply Wall St growth assumptions to extend the trend over a full decade.

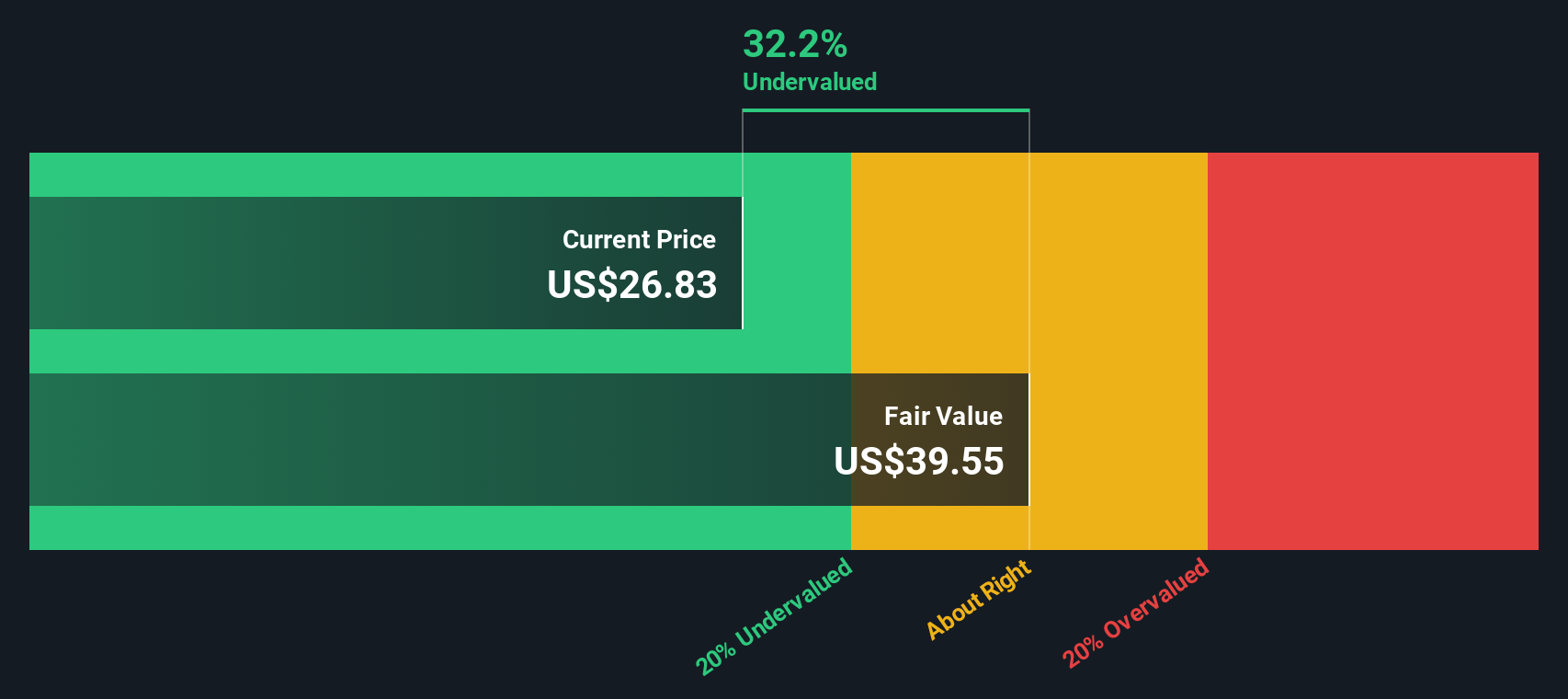

When all those future cash flows are discounted back using a two-stage Free Cash Flow to Equity model, the intrinsic value in this analysis is about $28.86 per share. At that price, the stock would be trading at roughly an 18.9% discount to the DCF fair value used in the model, which indicates the longer-term cash generation of the timberland portfolio may not be fully reflected in the current share price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Weyerhaeuser is undervalued by 18.9%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Weyerhaeuser Price vs Earnings

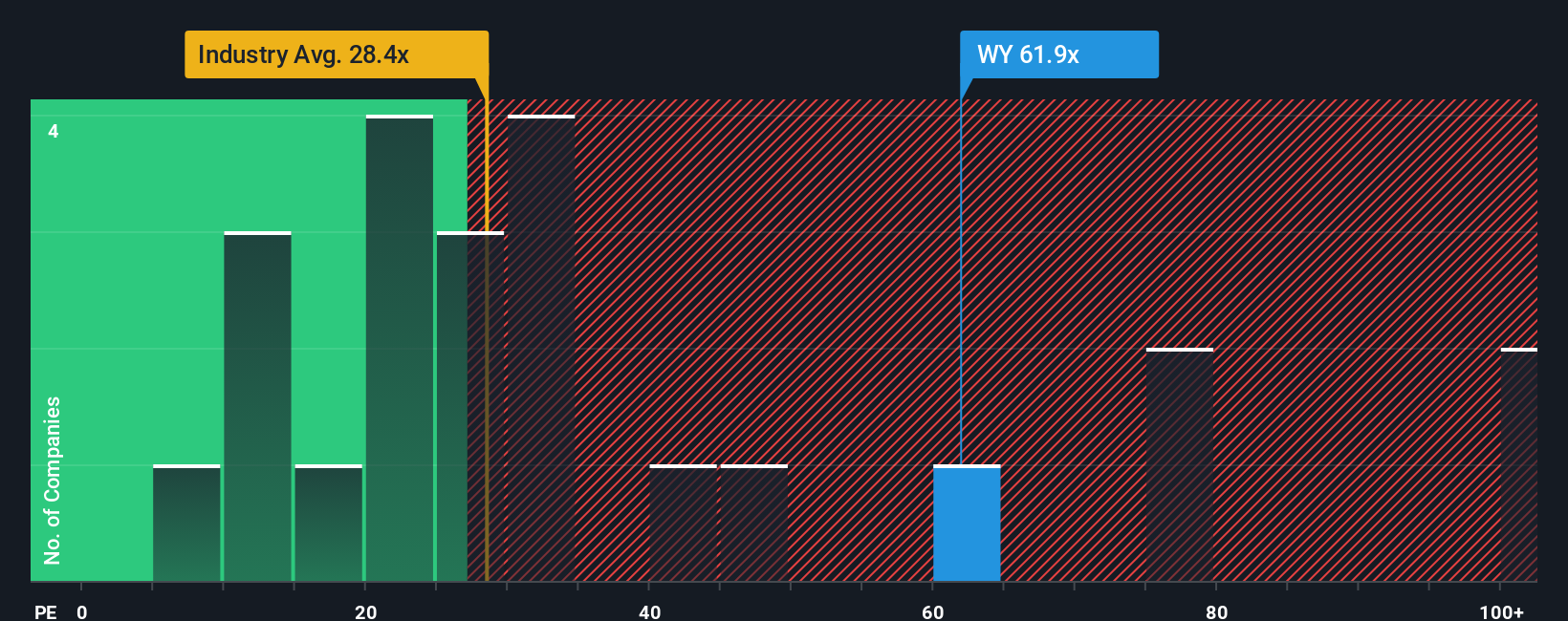

For profitable companies, the price to earnings ratio, or PE, is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. It is simple to understand and directly links the share price to the bottom line that ultimately supports dividends and reinvestment.

What counts as a reasonable PE depends largely on how fast earnings are expected to grow and how risky those earnings are. Higher growth and more predictable profits can justify a higher multiple, while slower or more volatile earnings usually deserve a lower one. Weyerhaeuser currently trades on a PE of about 50.9x, which is well above both the Specialized REITs industry average of roughly 16.6x and the peer group average of around 27.7x. This suggests the market is already pricing in strong prospects.

Simply Wall St’s Fair Ratio is a proprietary estimate of what Weyerhaeuser’s PE should be, given its earnings growth outlook, profit margins, industry, market value and risk profile. This richer framework is more useful than a simple peer or sector comparison because it adjusts for the company’s specific strengths and weaknesses. On that basis, Weyerhaeuser’s Fair Ratio is 36.5x, noticeably below the current 50.9x. This points to the shares looking expensive on an earnings basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Weyerhaeuser Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company, backed up by their own assumptions for future revenue, earnings, margins and fair value. A Narrative takes what you believe about Weyerhaeuser’s business, links it to a concrete financial forecast, and then converts that into a single fair value you can compare against today’s share price to decide whether to buy, hold or sell. On Simply Wall St’s Community page, millions of investors use Narratives as an easy, accessible tool, and each Narrative automatically updates when new information like earnings, news or guidance comes in, so your view never goes stale. For Weyerhaeuser, one Narrative might lean into share repurchases, long term demand for timber, and growth in Natural Climate Solutions to justify a higher fair value around 38 dollars. In contrast, a more cautious Narrative might focus on softer housing activity and margin pressure to support a lower fair value closer to 29 dollars. Where you sit between those views defines your personal Narrative.

Do you think there's more to the story for Weyerhaeuser? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Weyerhaeuser might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WY

Weyerhaeuser

Weyerhaeuser Company, one of the world's largest private owners of timberlands, began operations in 1900 and today owns or controls approximately 10.4 million acres of timberlands in the U.S., as well as additional public timberlands managed under long-term licenses in Canada.

Moderate growth potential with low risk.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)