- United States

- /

- Retail REITs

- /

- NYSE:MAC

Macerich (MAC): Exploring Whether Recent Multi‑Year Rebound Still Leaves the REIT Undervalued

Reviewed by Simply Wall St

Market backdrop and recent performance

Macerich (MAC) has been drifting quietly under the radar, even as the stock has climbed about 6% over the past month and roughly 4% in the past 3 months.

See our latest analysis for Macerich.

Despite a softer 1 day share price return of minus 1.56 percent leaving the stock at about 18.30 dollars, Macerich’s recent 30 day share price return of 6.33 percent sits against a weaker year to date share price return, while its three and five year total shareholder returns above 80 percent hint that sentiment has been rebuilding over the longer run.

If Macerich’s rebound has you thinking about what else could surprise on the upside, this is a good moment to explore fast growing stocks with high insider ownership.

So with the share price still below analyst targets but trading on a strong multi year rebound, is Macerich quietly undervalued and mispriced, or are investors already paying up for the next leg of growth?

Most Popular Narrative Narrative: 6.3% Undervalued

With the narrative placing fair value slightly above Macerich’s 18.30 dollars close, the spotlight shifts to what is driving that modest upside case.

The focus on experiential and destination-oriented retail (for example, DICK'S House of Sport, Cheesecake Factory, entertainment concepts) is revitalizing consumer engagement and increasing traffic, positioning the portfolio to benefit from experience-driven spending and capturing higher net margins over time.

Curious how a business with flat revenues is still modeled for rising margins and a premium future earnings multiple usually reserved for market darlings? Discover the specific profit path and capital allocation bets that underpin this fair value call.

Result: Fair Value of $19.53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy leverage and ongoing exposure to structurally challenged mall markets could quickly cap valuation upside if refinancing or asset sales are disappointing.

Find out about the key risks to this Macerich narrative.

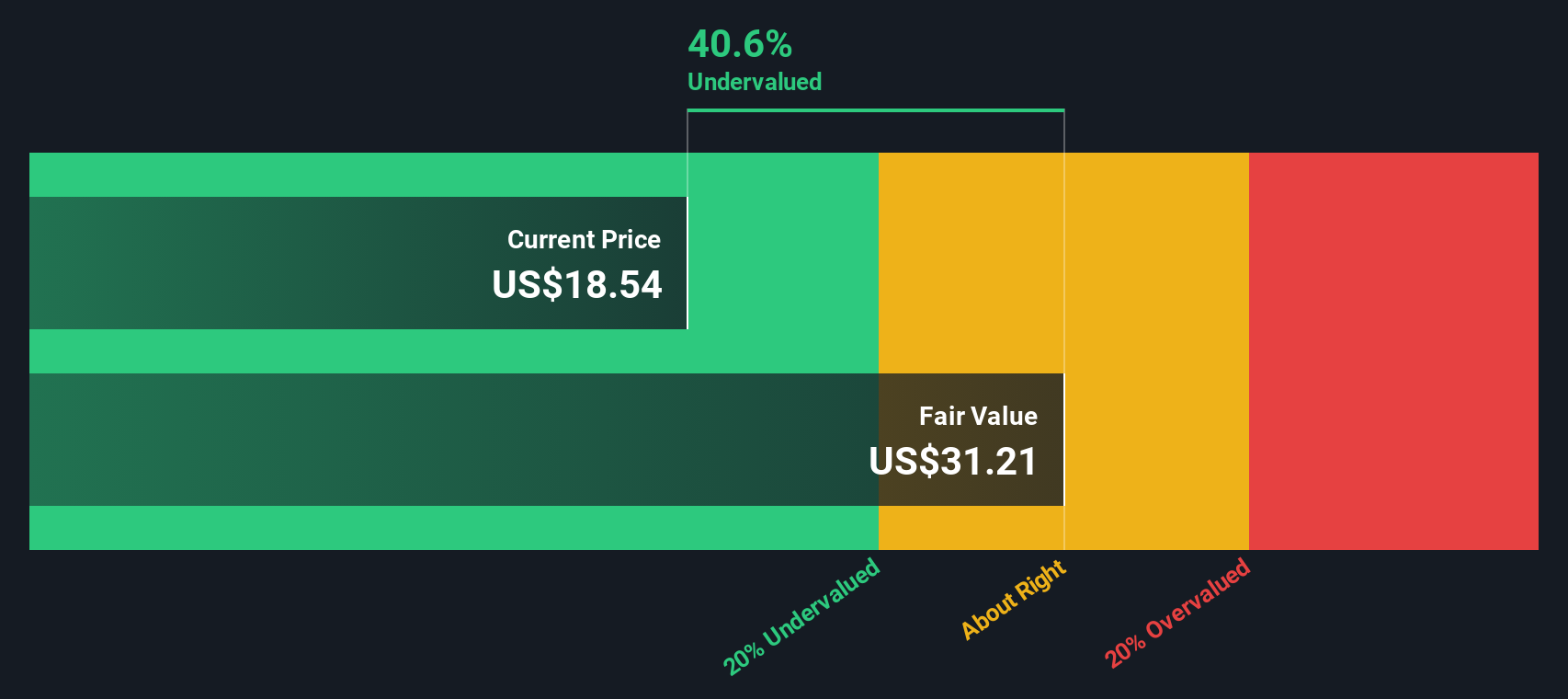

Another way to look at value

Our DCF model paints a much stronger upside than the narrative does, suggesting Macerich is trading roughly 41 percent below an estimated fair value of about 31 dollars. If cash flows really deserve that premium, are investors underestimating how much earnings power this portfolio can recover?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Macerich Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your Macerich research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

Before you stop at Macerich, lock in your next smart idea on Simply Wall St’s screener and stay a step ahead of less prepared investors.

- Capture potential mispricing by scanning these 915 undervalued stocks based on cash flows and target companies the market has not fully rewarded yet.

- Ride structural growth by reviewing these 30 healthcare AI stocks and uncovering businesses at the intersection of medicine and intelligent technology.

- Tap into high yield opportunities with these 13 dividend stocks with yields > 3% and focus on companies rewarding shareholders with robust income streams.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MAC

Macerich

Macerich is a fully integrated, self-managed, self-administered real estate investment trust (REIT).

Good value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)