- United States

- /

- Office REITs

- /

- NYSE:HPP

Undervalued Small Caps With Insider Action To Watch In March 2025

Reviewed by Simply Wall St

Over the last 7 days, the United States market has experienced a 3.1% drop despite having risen by 13% over the past year, with earnings forecasted to grow by 14% annually. In this context, identifying stocks that are potentially undervalued and have insider activity can offer intriguing opportunities for investors looking to navigate current market conditions.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| First Mid Bancshares | 11.3x | 2.8x | 37.68% | ★★★★★★ |

| Shore Bancshares | 11.1x | 2.5x | 2.16% | ★★★★★☆ |

| First United | 10.8x | 2.9x | 42.34% | ★★★★★☆ |

| German American Bancorp | 13.9x | 4.6x | 47.96% | ★★★★☆☆ |

| Arrow Financial | 14.8x | 3.3x | 40.64% | ★★★★☆☆ |

| Quanex Building Products | 26.7x | 0.7x | 43.87% | ★★★★☆☆ |

| Eagle Financial Services | 7.4x | 1.6x | 38.79% | ★★★★☆☆ |

| S&T Bancorp | 11.4x | 3.9x | 39.29% | ★★★★☆☆ |

| Innovex International | 8.4x | 1.8x | 43.51% | ★★★★☆☆ |

| Citizens & Northern | 12.5x | 3.0x | 42.26% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

Citizens & Northern (NasdaqCM:CZNC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Citizens & Northern operates as a community banking institution, providing a range of financial services with a market capitalization of $0.32 billion.

Operations: The company generates revenue primarily through community banking, with recent quarterly revenue reaching $106.13 million. Operating expenses have consistently been a significant portion of costs, recently reported at $74.26 million. The net income margin has varied over time, most recently recorded at 24.28%.

PE: 12.5x

Citizens & Northern, a smaller U.S. company, recently declared a quarterly dividend of US$0.28 per share payable in February 2025, reflecting stable shareholder returns. Despite no recent share repurchases, the company completed an earlier buyback of 26,034 shares for US$0.44 million under its September 2023 plan. Earnings are projected to grow by 8% annually, and their allowance for bad loans stands at a low 84%, indicating prudent risk management. Insider confidence is evident with recent share purchases by executives suggesting potential growth ahead.

- Take a closer look at Citizens & Northern's potential here in our valuation report.

Explore historical data to track Citizens & Northern's performance over time in our Past section.

Shore Bancshares (NasdaqGS:SHBI)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shore Bancshares operates as a community banking organization, with a focus on providing financial services and products, and has a market capitalization of $0.19 billion.

Operations: Shore Bancshares generates revenue primarily from its community banking operations, with recent revenues reaching $196.96 million. The company has consistently achieved a gross profit margin of 100%, indicating that all reported revenue translates directly into gross profit. Operating expenses, including general and administrative costs, significantly impact net income margins, which have shown variability over time but reached 22.28% in the latest period.

PE: 11.1x

Shore Bancshares stands out in the small-cap sector with a promising earnings growth forecast of 15.32% annually. Recent financials show a rise in net interest income to US$44 million for Q4 2024, up from US$41.53 million the previous year, and net income at US$13.28 million compared to US$10.49 million last year, highlighting its potential value. Insider confidence is evident as they continue acquiring shares, reflecting belief in future prospects despite upcoming CFO retirement changes effective August 2025.

- Get an in-depth perspective on Shore Bancshares' performance by reading our valuation report here.

Evaluate Shore Bancshares' historical performance by accessing our past performance report.

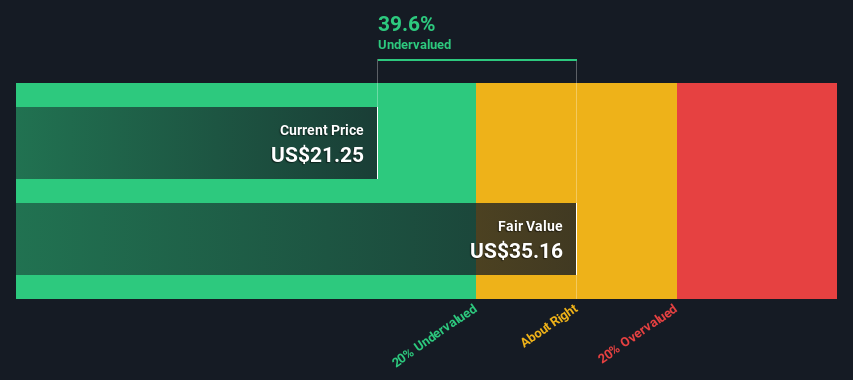

Hudson Pacific Properties (NYSE:HPP)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hudson Pacific Properties is a real estate investment trust focusing on owning and operating office and studio properties, with a market capitalization of approximately $1.92 billion.

Operations: Hudson Pacific Properties generates revenue primarily from its Office and Studio segments, with the Office segment contributing $692.28 million and the Studio segment adding $149.81 million. The company's gross profit margin has shown a declining trend, reaching 45.31% as of December 2024, reflecting changes in cost structures over time. Operating expenses include significant depreciation and amortization costs, which have impacted net income margins negatively in recent periods.

PE: -1.2x

Hudson Pacific Properties, a smaller player in the real estate sector, faces challenges with its unprofitable status and reliance on external borrowing. Despite reporting a net loss of US$342.93 million for 2024, insider confidence is evident as Chairman & CEO Victor Coleman purchased 50,000 shares worth US$176,500 recently. This move suggests belief in potential recovery or value within the company. The firm recently sold non-core assets to manage debt and anticipates GAAP non-cash revenue between US$10-15 million for 2025.

- Click here to discover the nuances of Hudson Pacific Properties with our detailed analytical valuation report.

Assess Hudson Pacific Properties' past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Get an in-depth perspective on all 61 Undervalued US Small Caps With Insider Buying by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hudson Pacific Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HPP

Hudson Pacific Properties

Hudson Pacific Properties (NYSE: HPP) is a real estate investment trust serving dynamic tech and media tenants in global epicenters for these synergistic, converging and secular growth industries.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives