Advertisement

- United States

- /

- Real Estate

- /

- NYSE:BEKE

Time To Worry? Analysts Just Downgraded Their KE Holdings Inc. (NYSE:BEKE) Outlook

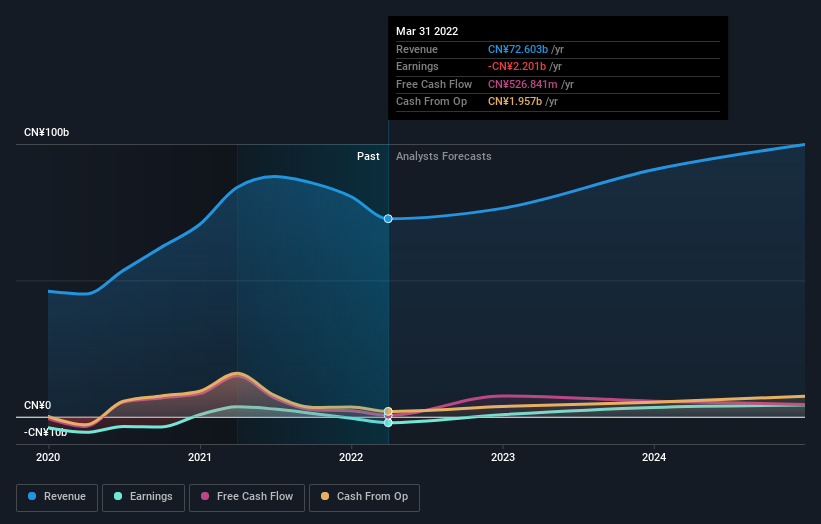

Market forces rained on the parade of KE Holdings Inc. (NYSE:BEKE) shareholders today, when the analysts downgraded their forecasts for this year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic. Surprisingly the share price has been buoyant, rising 13% to US$12.67 in the past 7 days. With such a sharp increase, it seems brokers may have seen something that is not yet being priced in by the wider market.

Following the latest downgrade, the current consensus, from the 13 analysts covering KE Holdings, is for revenues of CN¥64b in 2022, which would reflect a not inconsiderable 12% reduction in KE Holdings' sales over the past 12 months. Losses are predicted to fall substantially, shrinking 77% to CN¥0.41. Previously, the analysts had been modelling revenues of CN¥79b and earnings per share (EPS) of CN¥0.89 in 2022. So we can see that the consensus has become notably more bearish on KE Holdings' outlook with these numbers, making a measurable cut to this year's revenue estimates. Furthermore, they expect the business to be loss-making this year, compared to their previous forecasts of a profit.

See our latest analysis for KE Holdings

The consensus price target was broadly unchanged at CN¥127, perhaps implicitly signalling that the weaker earnings outlook is not expected to have a long-term impact on the valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic KE Holdings analyst has a price target of CN¥24.39 per share, while the most pessimistic values it at CN¥13.70. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that the analysts have a clear view on its prospects.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would also point out that the forecast 16% annualised revenue decline to the end of 2022 is roughly in line with the historical trend, which saw revenues shrink 14% annually over the past year By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 5.1% per year. So it's pretty clear that, while it does have declining revenues, the analysts also expect KE Holdings to suffer worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts are expecting KE Holdings to become unprofitable this year. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of KE Holdings going forwards.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple KE Holdings analysts - going out to 2024, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if KE Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:BEKE

KE Holdings

Through its subsidiaries, engages in operating an integrated online and offline platform for housing transactions and services in the People's Republic of China.

Flawless balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor