- United States

- /

- Biotech

- /

- NasdaqGM:XOMA

Forecast: Analysts Think XOMA Corporation's (NASDAQ:XOMA) Business Prospects Have Improved Drastically

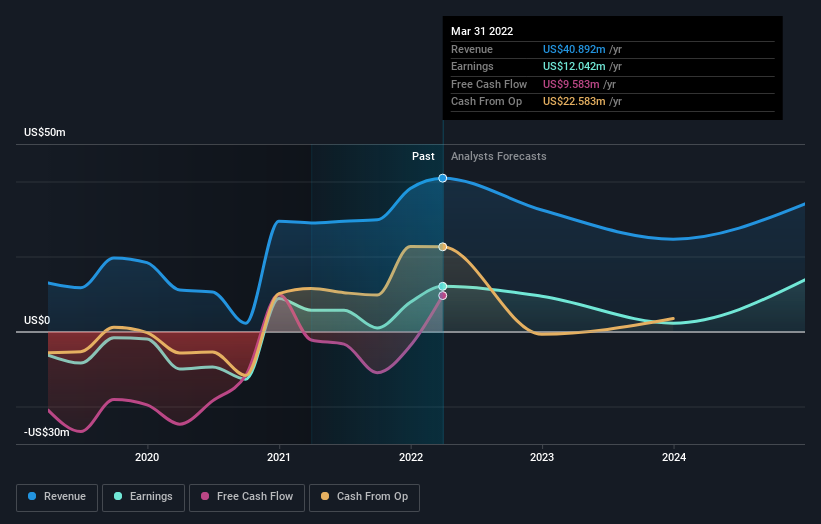

XOMA Corporation (NASDAQ:XOMA) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The analysts greatly increased their revenue estimates, suggesting a stark improvement in business fundamentals.

Following the upgrade, the consensus from three analysts covering XOMA is for revenues of US$32m in 2022, implying a substantial 21% decline in sales compared to the last 12 months. Statutory earnings per share are anticipated to nosedive 44% to US$0.59 in the same period. Yet before this consensus update, the analysts had been forecasting revenues of US$22m and losses of US$0.82 per share in 2022. So we can see that this has sparked a pretty clear upgrade to expectations, with higher revenues anticipated to lead to profit sooner than previously forecast.

Check out our latest analysis for XOMA

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 27% annualised revenue decline to the end of 2022. That is a notable change from historical growth of 1.9% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 12% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - XOMA is expected to lag the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that there is now an expectation for XOMA to become profitable this year, compared to previous expectations of a loss. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. With a serious upgrade to expectations, it might be time to take another look at XOMA.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple XOMA analysts - going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:XOMA

XOMA Royalty

Operates as a biotech royalty aggregator in the United States and the Asia Pacific.

High growth potential with adequate balance sheet.