- United States

- /

- Biotech

- /

- NasdaqCM:RCEL

Little Excitement Around AVITA Medical, Inc.'s (NASDAQ:RCEL) Revenues As Shares Take 39% Pounding

AVITA Medical, Inc. (NASDAQ:RCEL) shareholders won't be pleased to see that the share price has had a very rough month, dropping 39% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 34% share price drop.

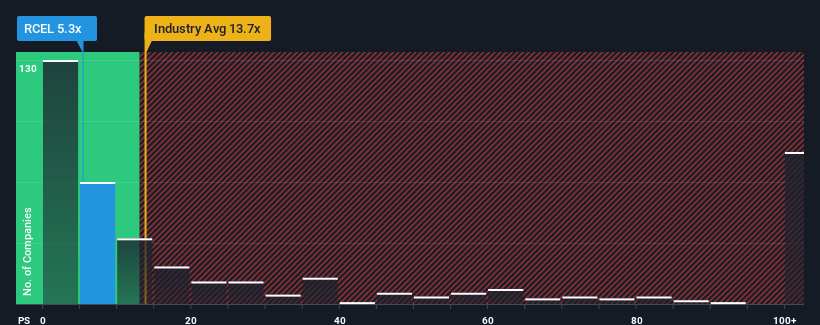

Since its price has dipped substantially, AVITA Medical may look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 5.3x, considering almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 13.7x and even P/S higher than 69x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

View our latest analysis for AVITA Medical

How AVITA Medical Has Been Performing

AVITA Medical could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on AVITA Medical.How Is AVITA Medical's Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like AVITA Medical's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 46% last year. The latest three year period has also seen an excellent 180% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 40% per year during the coming three years according to the ten analysts following the company. With the industry predicted to deliver 165% growth per year, the company is positioned for a weaker revenue result.

In light of this, it's understandable that AVITA Medical's P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

AVITA Medical's P/S looks about as weak as its stock price lately. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As expected, our analysis of AVITA Medical's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for AVITA Medical you should be aware of.

If you're unsure about the strength of AVITA Medical's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:RCEL

AVITA Medical

Operates as a regenerative medicine company in the United States and internationally.

Exceptional growth potential and undervalued.