Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:PRTA

New Forecasts: Here's What Analysts Think The Future Holds For Prothena Corporation plc (NASDAQ:PRTA)

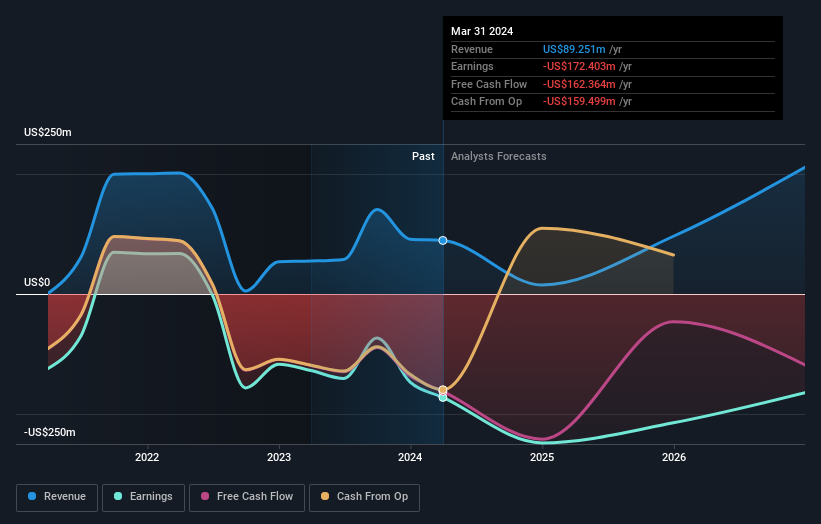

Prothena Corporation plc (NASDAQ:PRTA) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the latest upgrade, the current consensus, from the ten analysts covering Prothena, is for revenues of US$15m in 2024, which would reflect a substantial 83% reduction in Prothena's sales over the past 12 months. Losses are supposed to balloon 45% to US$4.66 per share. However, before this estimates update, the consensus had been expecting revenues of US$13m and US$4.81 per share in losses. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

See our latest analysis for Prothena

There was no major change to the consensus price target of US$63.43, perhaps suggesting that the analysts remain concerned about ongoing losses despite the improved earnings and revenue outlook.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Prothena's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with a forecast 91% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 40% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 18% per year. It's pretty clear that Prothena's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting Prothena is moving incrementally towards profitability. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Prothena.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Prothena going out to 2026, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PRTA

Prothena

A late-stage clinical biotechnology company, focuses on discovery and development of novel therapies to treat diseases caused by protein dysregulation in the United States.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor