- United States

- /

- Pharma

- /

- NYSE:BHC

Discover 3 Top Growth Companies With Significant Insider Ownership

Reviewed by Simply Wall St

As the United States market experiences a rally with major indices like the S&P 500 and Nasdaq posting gains, investor sentiment is buoyed by reports of potential tariff reductions. In this environment, growth companies with significant insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the company's operations and prospects.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 25.5% | 25.7% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.2% | 30.4% |

| Duolingo (NasdaqGS:DUOL) | 14.4% | 37.1% |

| Hims & Hers Health (NYSE:HIMS) | 13.2% | 21.8% |

| Corcept Therapeutics (NasdaqCM:CORT) | 11.7% | 36.7% |

| Coastal Financial (NasdaqGS:CCB) | 14.5% | 46.3% |

| Astera Labs (NasdaqGS:ALAB) | 15.9% | 61.3% |

| BBB Foods (NYSE:TBBB) | 16.2% | 41.1% |

| Upstart Holdings (NasdaqGS:UPST) | 12.7% | 100.1% |

| Credit Acceptance (NasdaqGS:CACC) | 14.4% | 33.6% |

Let's take a closer look at a couple of our picks from the screened companies.

AlTi Global (NasdaqCM:ALTI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AlTi Global, Inc. is a company that offers wealth and asset management services across the United States, the United Kingdom, and internationally with a market cap of $405.38 million.

Operations: The company's revenue is primarily derived from its Wealth & Capital Solutions segment at $198.26 million, followed by International Real Estate at $8.54 million, and Corporate activities contributing $0.14 million.

Insider Ownership: 37.7%

Earnings Growth Forecast: 119.3% p.a.

AlTi Global is projected to achieve profitability in the next three years, with earnings expected to grow at 119.26% annually, surpassing market averages. Despite this growth potential, recent financials show a decline in revenue and continued net losses. The company has undergone executive changes with the appointment of Mike Harrington as CFO, bringing extensive financial services experience. While insider trading data is unavailable for recent months, past shareholder dilution remains a concern.

- Click here and access our complete growth analysis report to understand the dynamics of AlTi Global.

- Insights from our recent valuation report point to the potential overvaluation of AlTi Global shares in the market.

Liquidia (NasdaqCM:LQDA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Liquidia Corporation is a biopharmaceutical company focused on developing, manufacturing, and commercializing products for unmet patient needs in the United States with a market cap of $1.29 billion.

Operations: The company generates revenue primarily from its pharmaceuticals segment, which amounted to $14 million.

Insider Ownership: 10.7%

Earnings Growth Forecast: 64.7% p.a.

Liquidia is forecast to achieve profitability within three years, with revenue growth projected at 44.3% annually, surpassing market expectations. Despite trading significantly below estimated fair value, recent earnings revealed a decrease in sales to US$14 million and increased net losses of US$130.39 million. The company filed multiple shelf registrations totaling over US$68 million for common stock offerings, indicating potential shareholder dilution concerns amidst its growth trajectory.

- Delve into the full analysis future growth report here for a deeper understanding of Liquidia.

- Our valuation report here indicates Liquidia may be overvalued.

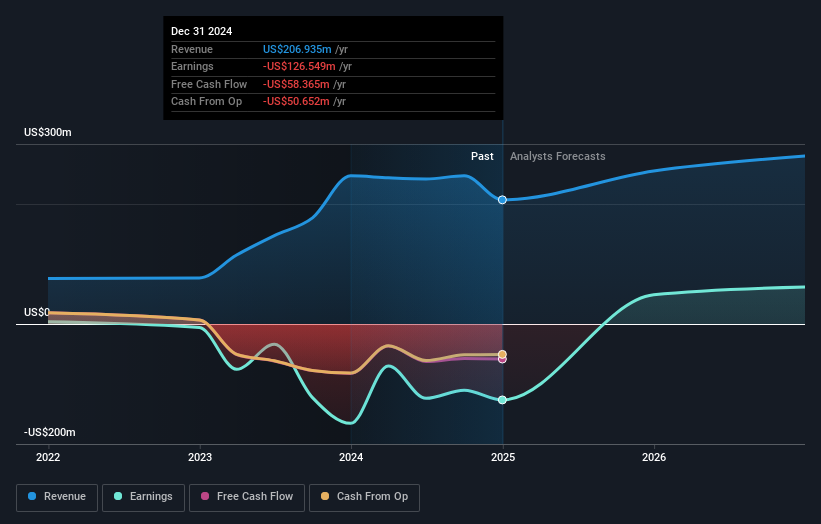

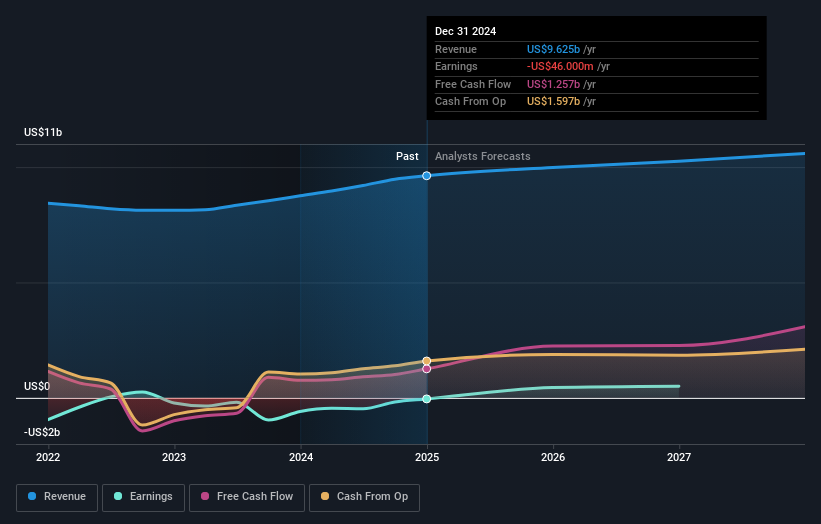

Bausch Health Companies (NYSE:BHC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bausch Health Companies Inc. is a diversified specialty pharmaceutical and medical device company that develops, manufactures, and markets products across various fields including gastroenterology, neurology, dermatology, and eye health both in the United States and internationally, with a market cap of approximately $2.63 billion.

Operations: The company's revenue segments include Salix at $2.33 billion, Diversified Products at $950 million, Bausch + Lomb at $4.79 billion, International operations contributing $1.11 billion, and Solta Medical generating $440 million.

Insider Ownership: 10.5%

Earnings Growth Forecast: 87.8% p.a.

Bausch Health Companies is forecast to become profitable within three years, with earnings expected to grow at 87.84% annually. Despite negative shareholders' equity, BHC trades significantly below its estimated fair value and offers good relative value compared to peers. Recent financial results show improved revenue and reduced losses, while the company has announced significant debt refinancing plans totaling US$7.4 billion, which may impact future financial flexibility and growth prospects.

- Navigate through the intricacies of Bausch Health Companies with our comprehensive analyst estimates report here.

- Our valuation report here indicates Bausch Health Companies may be undervalued.

Make It Happen

- Click this link to deep-dive into the 205 companies within our Fast Growing US Companies With High Insider Ownership screener.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Bausch Health Companies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BHC

Bausch Health Companies

Operates as a diversified specialty pharmaceutical and medical device company, develops, manufactures, and markets a range of products primarily in gastroenterology, hepatology, neurology, dermatology, generic pharmaceuticals, over-the-counter (OTC) products, aesthetic medical devices, and eye health in the United States and internationally.

Undervalued with reasonable growth potential.