Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:ICPT

Intercept Pharmaceuticals (NASDAQ:ICPT) Has Debt But No Earnings; Should You Worry?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Intercept Pharmaceuticals, Inc. (NASDAQ:ICPT) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Intercept Pharmaceuticals

What Is Intercept Pharmaceuticals's Net Debt?

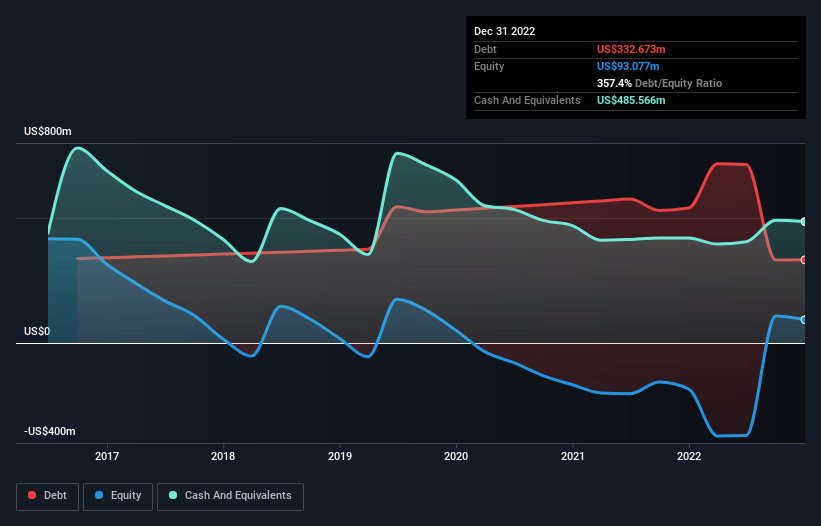

You can click the graphic below for the historical numbers, but it shows that Intercept Pharmaceuticals had US$332.7m of debt in December 2022, down from US$539.8m, one year before. But on the other hand it also has US$485.6m in cash, leading to a US$152.9m net cash position.

How Strong Is Intercept Pharmaceuticals' Balance Sheet?

We can see from the most recent balance sheet that Intercept Pharmaceuticals had liabilities of US$230.1m falling due within a year, and liabilities of US$230.6m due beyond that. Offsetting these obligations, it had cash of US$485.6m as well as receivables valued at US$29.3m due within 12 months. So it can boast US$54.2m more liquid assets than total liabilities.

This surplus suggests that Intercept Pharmaceuticals has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Intercept Pharmaceuticals boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Intercept Pharmaceuticals can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Intercept Pharmaceuticals wasn't profitable at an EBIT level, but managed to grow its revenue by 9.6%, to US$286m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is Intercept Pharmaceuticals?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Intercept Pharmaceuticals lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$27m and booked a US$175m accounting loss. However, it has net cash of US$152.9m, so it has a bit of time before it will need more capital. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 1 warning sign we've spotted with Intercept Pharmaceuticals .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:ICPT

Intercept Pharmaceuticals

Intercept Pharmaceuticals, Inc., a biopharmaceutical company, focuses on the development and commercialization of therapeutics to treat progressive non-viral liver diseases in the United States, Europe, and Canada.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor