Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:LNAI

Enochian Biosciences (NASDAQ:ENOB) Has Debt But No Earnings; Should You Worry?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Enochian Biosciences, Inc. (NASDAQ:ENOB) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Enochian Biosciences

What Is Enochian Biosciences's Net Debt?

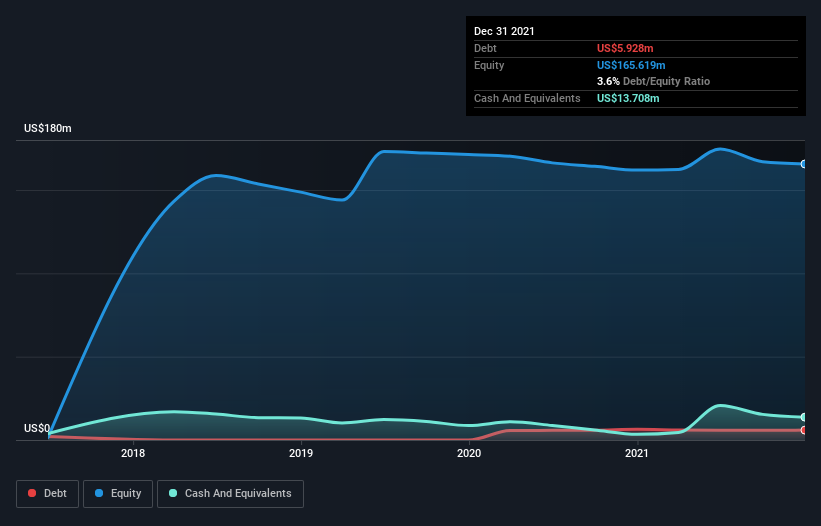

You can click the graphic below for the historical numbers, but it shows that Enochian Biosciences had US$5.93m of debt in December 2021, down from US$6.41m, one year before. However, its balance sheet shows it holds US$13.7m in cash, so it actually has US$7.78m net cash.

How Strong Is Enochian Biosciences' Balance Sheet?

According to the last reported balance sheet, Enochian Biosciences had liabilities of US$6.20m due within 12 months, and liabilities of US$11.3m due beyond 12 months. Offsetting these obligations, it had cash of US$13.7m as well as receivables valued at US$1.6k due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$3.81m.

Having regard to Enochian Biosciences' size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the US$473.7m company is short on cash, but still worth keeping an eye on the balance sheet. While it does have liabilities worth noting, Enochian Biosciences also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Enochian Biosciences's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Since Enochian Biosciences doesn't have significant operating revenue, shareholders may be hoping it comes up with a great new product, before it runs out of money.

So How Risky Is Enochian Biosciences?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And in the last year Enochian Biosciences had an earnings before interest and tax (EBIT) loss, truth be told. Indeed, in that time it burnt through US$25m of cash and made a loss of US$38m. However, it has net cash of US$7.78m, so it has a bit of time before it will need more capital. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 5 warning signs for Enochian Biosciences you should be aware of, and 3 of them are potentially serious.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LNAI

Lunai Bioworks

A pre-clinical stage biotechnology company, provides medicine, diagnostics, and biodefense products the United States and the Netherlands.

Medium-low risk with weak fundamentals.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor