Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:EDIT

Growth Investors: Industry Analysts Just Upgraded Their Editas Medicine, Inc. (NASDAQ:EDIT) Revenue Forecasts By 11%

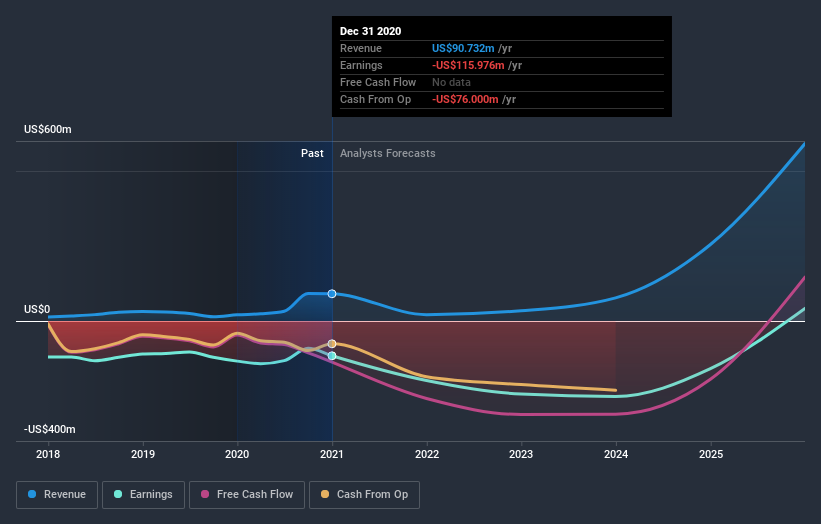

Shareholders in Editas Medicine, Inc. (NASDAQ:EDIT) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

After the upgrade, the consensus from Editas Medicine's eight analysts is for revenues of US$24m in 2021, which would reflect a sizeable 74% decline in sales compared to the last year of performance. Per-share losses are expected to explode, reaching US$3.46 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$22m and losses of US$3.52 per share in 2021. So there's definitely been a change in sentiment in this update, with the analysts upgrading this year's revenue estimates, while at the same time holding losses per share steady.

View our latest analysis for Editas Medicine

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that sales are expected to reverse, with a forecast 74% annualised revenue decline to the end of 2021. That is a notable change from historical growth of 53% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 19% annually for the foreseeable future. It's pretty clear that Editas Medicine's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around Editas Medicine's prospects. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Editas Medicine.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Editas Medicine analysts - going out to 2025, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading Editas Medicine or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Editas Medicine might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:EDIT

Editas Medicine

A clinical stage genome editing company, focuses on developing transformative genomic medicines to treat a range of serious diseases.

Flawless balance sheet very low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|24.5% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|45.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|33.9% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|57.0% undervalued

AX

Community Contributor