Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:CVAC

Analysts Are Betting On CureVac N.V. (NASDAQ:CVAC) With A Big Upgrade This Week

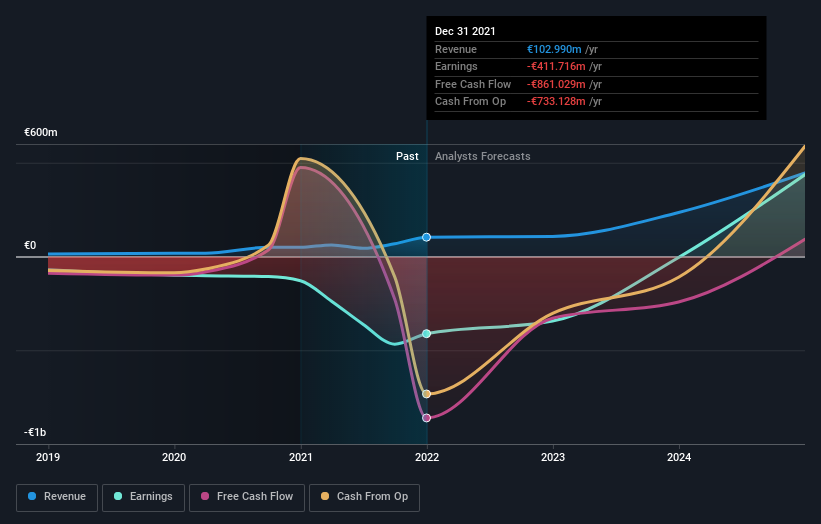

Celebrations may be in order for CureVac N.V. (NASDAQ:CVAC) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. Investor sentiment seems to be improving too, with the share price up 5.6% to US$17.09 over the past 7 days. It will be interesting to see if this latest upgrade is enough to kickstart further buying interest in the stock.

Following the upgrade, the latest consensus from CureVac's six analysts is for revenues of €107m in 2022, which would reflect an okay 3.8% improvement in sales compared to the last 12 months. The loss per share is expected to ameliorate slightly, reducing to €2.11. Yet before this consensus update, the analysts had been forecasting revenues of €79m and losses of €2.22 per share in 2022. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

View our latest analysis for CureVac

Yet despite these upgrades, the analysts cut their price target 16% to €26.88, implicitly signalling that the ongoing losses are likely to weigh negatively on CureVac's valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on CureVac, with the most bullish analyst valuing it at €49.07 and the most bearish at €14.77 per share. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the CureVac's past performance and to peers in the same industry. We would highlight that CureVac's revenue growth is expected to slow, with the forecast 3.8% annualised growth rate until the end of 2022 being well below the historical 57% p.a. growth over the last three years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 11% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than CureVac.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting CureVac is moving incrementally towards profitability. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of CureVac's future valuation. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at CureVac.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect CureVac to be able to reach break-even within the next few years. You can learn more about these forecasts, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:CVAC

CureVac

A biopharmaceutical company, focuses on developing various transformative medicines based on messenger ribonucleic acid (mRNA).

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor