Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:CCCC

C4 Therapeutics, Inc.'s (NASDAQ:CCCC) 33% Share Price Plunge Could Signal Some Risk

C4 Therapeutics, Inc. (NASDAQ:CCCC) shareholders won't be pleased to see that the share price has had a very rough month, dropping 33% and undoing the prior period's positive performance. The good news is that in the last year, the stock has shone bright like a diamond, gaining 161%.

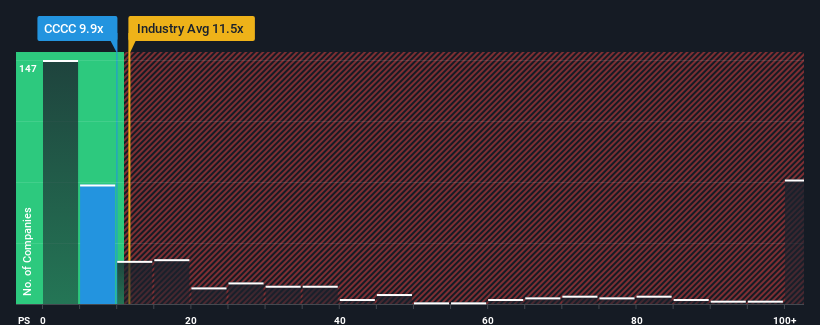

Although its price has dipped substantially, there still wouldn't be many who think C4 Therapeutics' price-to-sales (or "P/S") ratio of 9.9x is worth a mention when the median P/S in the United States' Biotechs industry is similar at about 11.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Check out our latest analysis for C4 Therapeutics

What Does C4 Therapeutics' P/S Mean For Shareholders?

Recent times haven't been great for C4 Therapeutics as its revenue has been rising slower than most other companies. Perhaps the market is expecting future revenue performance to lift, which has kept the P/S from declining. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think C4 Therapeutics' future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The P/S Ratio?

C4 Therapeutics' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, we see that the company grew revenue by an impressive 65% last year. Although, its longer-term performance hasn't been as strong with three-year revenue growth being relatively non-existent overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Looking ahead now, revenue is anticipated to slump, contracting by 17% per annum during the coming three years according to the six analysts following the company. With the industry predicted to deliver 120% growth per annum, that's a disappointing outcome.

With this information, we find it concerning that C4 Therapeutics is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

The Bottom Line On C4 Therapeutics' P/S

C4 Therapeutics' plummeting stock price has brought its P/S back to a similar region as the rest of the industry. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It appears that C4 Therapeutics currently trades on a higher than expected P/S for a company whose revenues are forecast to decline. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the poor revenue outlook tells us one thing, it's that these current price levels could be unsustainable.

There are also other vital risk factors to consider and we've discovered 4 warning signs for C4 Therapeutics (1 is a bit concerning!) that you should be aware of before investing here.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CCCC

C4 Therapeutics

A clinical-stage biopharmaceutical company, develops novel therapeutic candidates to degrade disease-causing proteins for the treatment of cancer, neurodegenerative conditions, and other diseases.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|9.5% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|27.6% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|36.6% undervalued

DZ

Community Contributor