Advertisement

- United States

- /

- Biotech

- /

- NasdaqCM:WHWK

Improved Revenues Required Before Aadi Bioscience, Inc. (NASDAQ:AADI) Stock's 28% Jump Looks Justified

Aadi Bioscience, Inc. (NASDAQ:AADI) shareholders are no doubt pleased to see that the share price has bounced 28% in the last month, although it is still struggling to make up recently lost ground. But the last month did very little to improve the 75% share price decline over the last year.

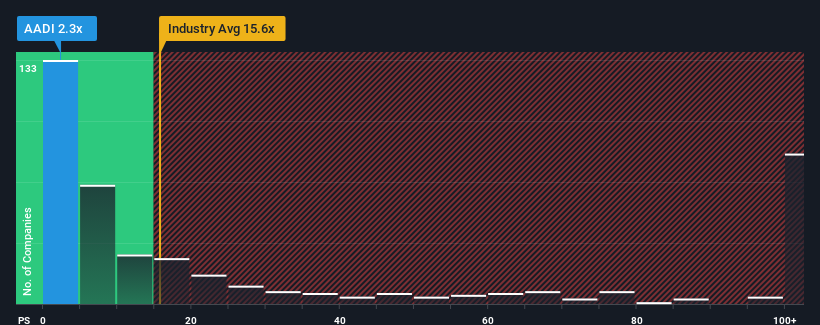

In spite of the firm bounce in price, Aadi Bioscience may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 2.3x, since almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 15.6x and even P/S higher than 80x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Aadi Bioscience

What Does Aadi Bioscience's Recent Performance Look Like?

Aadi Bioscience could be doing better as it's been growing revenue less than most other companies lately. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Keen to find out how analysts think Aadi Bioscience's future stacks up against the industry? In that case, our free report is a great place to start.Do Revenue Forecasts Match The Low P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as depressed as Aadi Bioscience's is when the company's growth is on track to lag the industry decidedly.

Taking a look back first, we see that the company grew revenue by an impressive 112% last year. Pleasingly, revenue has also lifted 59% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 48% per annum during the coming three years according to the four analysts following the company. That's shaping up to be materially lower than the 273% per annum growth forecast for the broader industry.

With this in consideration, its clear as to why Aadi Bioscience's P/S is falling short industry peers. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Aadi Bioscience's recent share price jump still sees fails to bring its P/S alongside the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Aadi Bioscience's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

Plus, you should also learn about these 3 warning signs we've spotted with Aadi Bioscience (including 1 which is a bit concerning).

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Whitehawk Therapeutics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:WHWK

Whitehawk Therapeutics

A clinical-stage oncology therapeutics company that develops technologies to establish tumor biology for cancer treatments.

Flawless balance sheet with moderate risk.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative