- United States

- /

- Interactive Media and Services

- /

- NYSE:YELP

Has The Market Mispriced Yelp After Recent Share Price Rebound?

Reviewed by Bailey Pemberton

- If you have ever wondered whether Yelp is quietly turning into a value play while everyone chases flashier tech names, this is the moment to take a closer look.

- The stock has bounced 2.4% over the last week and 8.2% over the last month, even though it is still down 21.6% year to date and 22.8% over the past year. This hints that sentiment and risk perceptions may be starting to pivot.

- Recent headlines have focused on Yelp's ongoing push into higher value advertising tools and enhanced services for local businesses, a shift that could support more durable revenue per customer. At the same time, the market is reacting to competitive pressures in local search and reviews, which keeps expectations in check and creates an interesting setup for valuation.

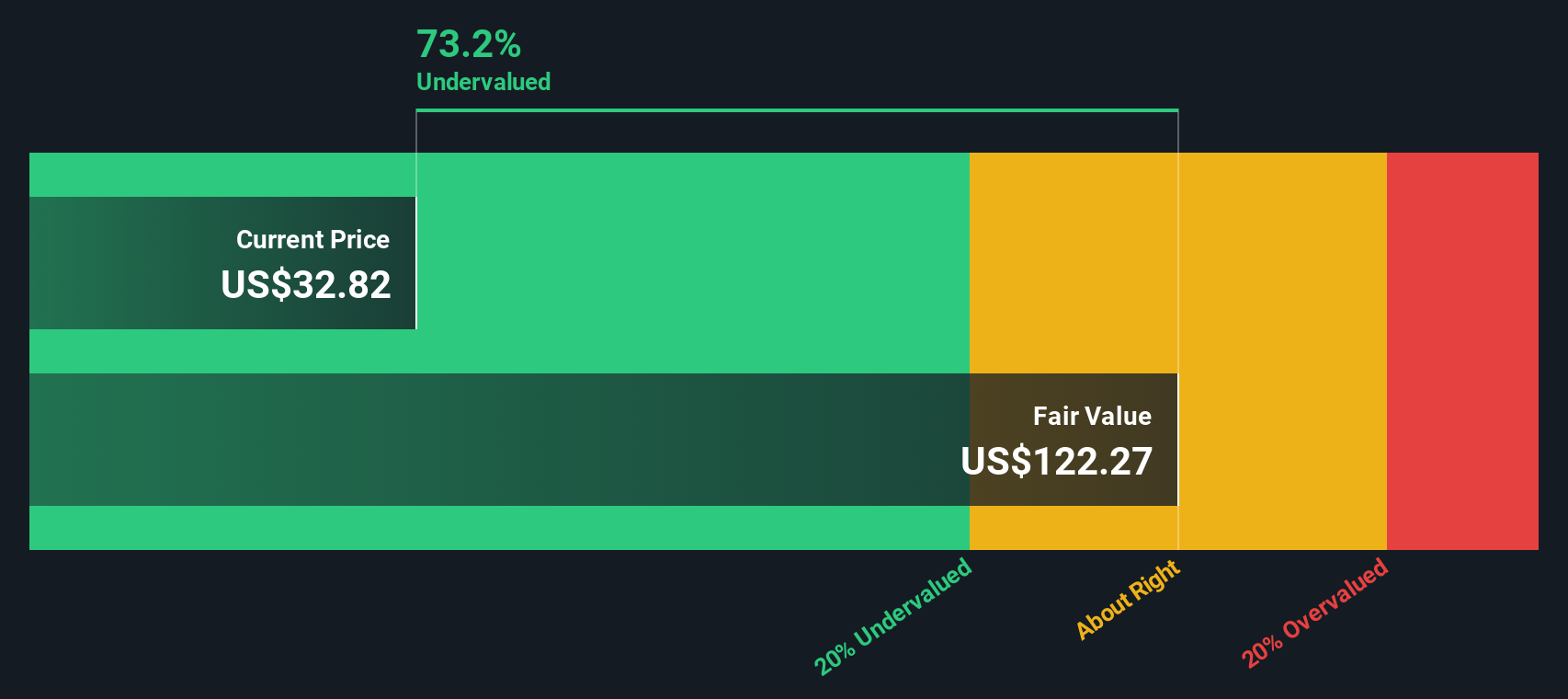

- Put that together and you get a valuation score of 5/6. This suggests Yelp screens as undervalued on most of the key metrics we track, and in the next sections we will break down those different valuation approaches while hinting at an even better way to judge fair value by the end of the article.

Find out why Yelp's -22.8% return over the last year is lagging behind its peers.

Approach 1: Yelp Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, values a business by estimating the cash it can generate in the future and then discounting those cash flows back to what they are worth in today’s dollars.

For Yelp, the model starts with last twelve month free cash flow of about $319 million. Analysts provide explicit forecasts for the next few years, and Simply Wall St then extends those estimates out over a 10 year period using a 2 Stage Free Cash Flow to Equity framework. By 2035, annual free cash flow is projected to be around $266 million, with growth moderating over time as the business matures.

When those future cash flows are discounted back, the DCF model arrives at an intrinsic value of roughly $66.50 per share in $. Compared to the current share price, this implies the stock is about 54.0% undervalued, which indicates that the market is pricing in a far weaker cash flow outlook than the model assumes.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Yelp is undervalued by 54.0%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

Approach 2: Yelp Price vs Earnings

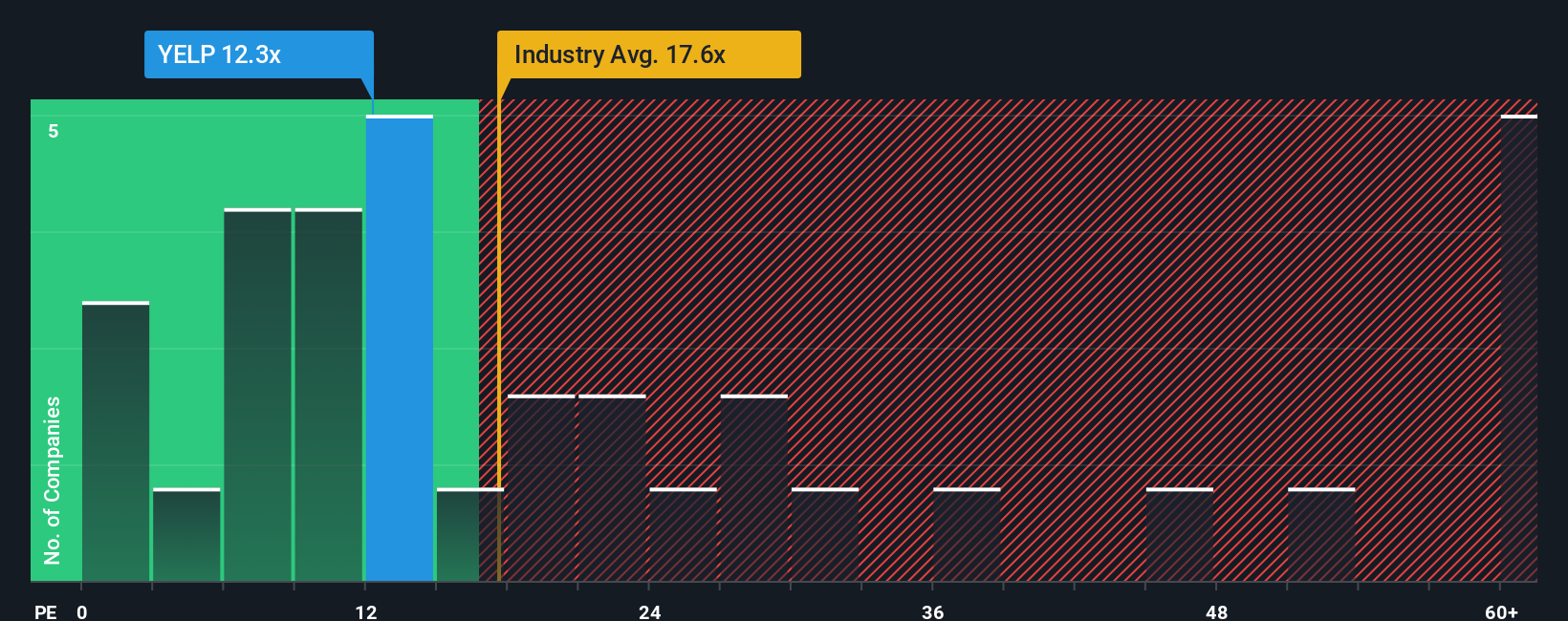

For a profitable company like Yelp, the price to earnings (PE) ratio is a useful way to see how much investors are paying for each dollar of current earnings. It captures not just today’s profitability, but also how optimistic the market is about future growth and how much risk investors are willing to tolerate.

In simple terms, faster growing and lower risk businesses usually justify a higher, or more expensive, PE multiple, while slower or riskier ones should trade on a lower multiple. Yelp currently trades on about 12.6x earnings. That is below both the broader Interactive Media and Services industry average of roughly 16.9x and the peer group average of about 21.3x, suggesting the market is taking a cautious stance.

Simply Wall St’s Fair Ratio framework refines this comparison by estimating what PE multiple a company should trade on, given its earnings growth profile, margins, industry, market cap and specific risk factors. For Yelp, that Fair Ratio is around 15.9x, above the current 12.6x. On this basis, the stock appears undervalued relative to what a balanced view of its fundamentals would imply.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1456 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Yelp Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Yelp’s story to a set of financial forecasts and a fair value that updates as reality changes. A Narrative lets you spell out why you think AI features, advertiser tools and cost control will shape Yelp’s future, then ties that story to explicit assumptions for revenue, earnings and margins, producing a Fair Value you can compare directly to today’s share price to assess whether it looks like a buy, hold or sell. Narratives on Simply Wall St, available on the Community page used by millions of investors, recalculate automatically when new information comes in, such as earnings results, guidance changes or major product news. This helps your thesis stay current rather than static. For Yelp, one investor might build a bullish Narrative that leans on accelerating AI adoption and assign a fair value closer to $40. A more cautious investor could focus on competition and segment weakness and land nearer $30, and seeing those side by side helps you judge where your own view fits on the spectrum.

Do you think there's more to the story for Yelp? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:YELP

Yelp

Operates a platform that connects consumers with local businesses in the United States and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)